BLOG — Dec 04, 2019

Cloud 2.0 – What to expect in financial services

Research from TABB Group earlier this year found that use of public cloud within financial services was poised to accelerate in 2019. These findings are reflected in our own recent survey[1] which found that 80% of European and North American asset managers will be using the cloud for data management by the end of 2020. It seems the cloud has well and truly taken off within financial services and is now the default option for firms looking to save operational costs and become more nimble in their operations. With cloud now mainstream within the industry, how is the next phase of adoption shaping up?

The benefits of the cloud are now well understood. Asset managers in our survey cited the ability to offload administrative burdens as the biggest benefit of moving to the cloud by 42%. Moving commoditised processes to the cloud where they can be managed by a third party is freeing up firms' resources to focus on activities that lend them a competitive edge. Cost reduction and scalability were also identified as significant drivers for the cloud in our survey.

However, our research also showed that the drivers for cloud migration are evolving. So, what does cloud 2.0 look like?

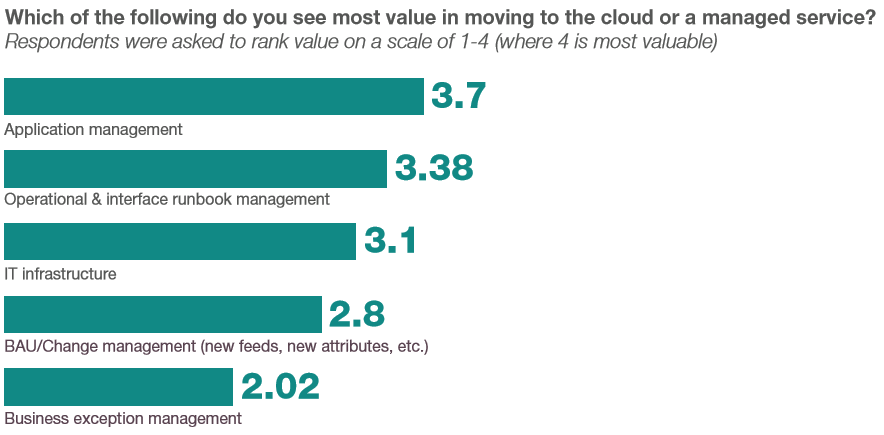

Firstly, buy-side firms are intent on maximising the benefits of the cloud by adopting a managed service model. As understanding of the cloud matures, firms are looking beyond infrastructure to outsourcing the management of their applications. When asked which functions promised the most value in being cloud-based, application management came in first place with IT infrastructure down in third place (see chart below for the full results). While discussions about the cloud have historically focused on infrastructure, there is now more interest in the benefits of a managed service which can support business efficiency by offloading commodity, low-value functions to a specialist. The role of the specialist is critical as managed service providers have built up years of experience of running data management in the cloud which firms can benefit greatly from.

A second driver for cloud is the explosion of alternative data. Financial firms are faced with managing a growing onslaught of data - particularly with the rise of alternative data sets that come from an array of new and diverse sources including ESG, satellite imagery, social media sentiment and shipping bill of lading data. The promise of new insights to support alpha generation is tantalising, but it also means managing a higher volume of data at a much higher frequency than traditional data sources. Quite often the data comes unstructured, requires work to gain the insights and is expensive to store. The cloud offers the opportunity to store huge volumes of data at low cost, while also providing the framework for the testing of innovative new ideas through an environment that can be quickly and easily scaled up or down. Cloud based data management technology also has a role to play in helping firms to structure, match and make sense of their alternative data alongside their traditional data sets.

Finally, the third and perhaps most significant emerging driver is the transformational techniques, such as artificial intelligence (AI) and advanced analytics, that are leveraging the cloud as an enabling technology. Data management in the cloud will be transformed over the coming years as AI makes onboarding of new data sets faster and easier and bots enable more data and operational activities to be served up proactively to the user. As these new models, that devour huge volumes of data, become increasingly mainstream, it is the cloud that will further propel their growth and support innovation.

As the buy-side industry grapples with these technology advances, combined with the challenging market conditions of new regulatory frameworks, macro-economic events and fee compression, firms are recognizing that deployed, in-house solutions are unsustainable. They are increasingly migrating many of their workflows to a cloud-based managed service model that is capable of managing alternative data sets and will harness the growing potential of AI. Cloud 2.0 is well and truly here.

For more information on this topic, download our white paper here.

[1] WBR Insights, Taking Data Management to the Next Level, October 2019: Survey of EMEA and North America asset managers with $10-100 billion AUM

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.