4 Aug, 2016 | 09:00

Chinese Firms Look To Challenged South Korean Insurers For New Profit Sources

Highlights

We have strong faith in the growth potential of the Korean market. Anbang has a long-term commitment to playing a meaningful role in the development of the Korean financial [and] insurance industry, as evidenced by its progress to date with [TONGYANG].

IFRS 4 in 2020 will be a big headache to Chinese companies, said Eunice Tan, a director of Greater China insurance coverage at S&P Global Ratings.

South Korean insurers facing tough times could well serve as new money-making platforms for Chinese companies.

Amid persistently low interest rates, and with tougher capital requirements looming, it is becoming increasingly difficult to run insurers in South Korea. For that reason, small and medium-sized companies in the sector, one after another, have been put up for sale.

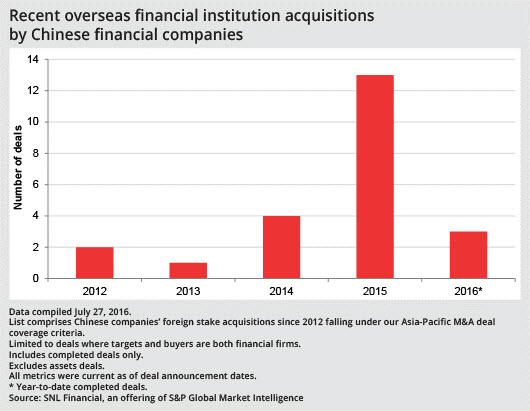

Bidding for them has been dominated by Chinese companies, which have been aggressively pursuing overseas acquisitions in recent years. Although any insurance business operators in South Korea would face the same challenges, one way Chinese companies can make profit from the industry in the country is to gain market share by pushing high-return products financed with investments in China and repatriate earnings in dividends, said Jo Young-wun, a research fellow covering international insurance at the Korea Insurance Research Institute.

That may be what China Taiping Insurance Group Ltd.'s Taiping Life Insurance Co. Ltd. wants to do if it succeeds in buying ING Life Insurance Korea Ltd. The Chinese company is among bidders for the whole of the fifth-largest South Korean insurer by assets.

During a meeting with ING Life executives as part of due diligence in early July, China Taiping and Taiping Life officials asked whether the South Korean company can increase investments in China without running into regulatory problems, a person with direct knowledge of the matter told S&P Global Market Intelligence.

Changes at TONGYANG Life Insurance Co. Ltd. after Anbang Insurance Group Co. bought it in September 2015 suggest a similar strategy in play.

Since the acquisition, TONGYANG has focused on savings-type products paying higher yields than its competitors' offerings. Sales of such policies more than tripled to 1.444 trillion won in the first quarter from a year earlier, to make up 73.4% of total premiums earned during the three months, compared to 47.6% in the January-March period in 2015.

By comparison, savings products accounted for a combined 42.6% of first-quarter total premiums at all South Korean life insurers, according to data from the Financial Supervisory Service. At industry leader Samsung Life Insurance Co. Ltd., the proportion was just 9.3%.

A case in point: TONGYANG under Anbang

After coming under the control of Anbang, TONGYANG began investing in Chinese assets, buying U.S. dollar-denominated bonds issued by the country's government-owned companies. At the end of 2015, TONGYANG's purchases of Chinese assets grew to 13.2% of total overseas assets from none before the ownership change, according to the South Korean insurer's annual reports.

Investments in China tend to yield better returns than those in South Korea, a TONGYANG investor relations official said in an interview. Hence, income from Chinese assets allows TONGYANG to offer higher yields for customers than its rivals can.

The strategy helped TONGYANG increase first-quarter net profit by 8.8% year over year to 81 billion won, compared to 3.6% growth in industrywide earnings. TONGYANG is also giving more of its profit back to shareholders than it did before Anbang acquired a 63% stake. The South Korean company raised its dividend payout ratio to 40.1% for 2015 from 34.1% for the prior year.

"How Anbang is managing TONGYANG is a window into Chinese companies' strategy in South Korea," said Won Jae-woong, an insurance analyst at Mirae Asset Securities.

Anbang, currently the only Chinese company in the South Korean insurance sector, touts opportunities in the market.

"We have strong faith in the growth potential of the Korean market. Anbang has a long-term commitment to playing a meaningful role in the development of the Korean financial [and] insurance industry, as evidenced by its progress to date with [TONGYANG]," a representative for the Chinese company said in an emailed response to queries.

In April, Anbang clinched its second insurance deal in South Korea, agreeing to buy Allianz Group's South Korean life operations. The transaction is pending local regulatory approval.

Chinese bidders

The Chinese presence in South Korea's insurance industry may expand further. In the ING Life auction, the main contenders are Chinese firms including Taiping Life. They remain in the running, even as the private equity firm that currently owns the South Korean insurer, MBK Partners Ltd., is seeking to sell the business for double the price it paid ING Groep NV in 2013.

There will be more opportunities for Chinese insurers to expand into South Korea through deals. Korea Development Bank's KDB Life Insurance Co. Ltd.and Prudential Plc's PCA Life Insurance Co. Ltd. will soon be put on the block, according to media reports.

Companies are shedding insurance assets in South Korea, as the industry faces low rates and the prospect of tougher capital rules.

Under International Financial Reporting Standard 4 Phase II, to be implemented in 2020, South Korean insurance companies will have to set aside significant more capital. Under the new requirements, the value of liabilities to customers will be discounted less when market rates decline, forcing companies that sold high-yield products in the past to increase reserves. The risk-based capital ratio of the South Korean life insurance industry is estimated to fall to 83% after the rules are applied from 311% as of the end of 2014, according to a Korea Insurance Research Institute research report.

The rule change is a burden for Chinese buyers of South Korean insurers as well.

"IFRS 4 in 2020 will be a big headache to Chinese companies," said Eunice Tan, a director of Greater China insurance coverage at S&P Global Ratings.

Yet, for Chinese insurers, South Korea can still be attractive, with fewer regulatory obstacles to outbound investments than in the domestic market, where there are strict foreign-exchange restrictions.

"From Chinese insurers' perspective, South Korean insurers have more freedom in terms of overseas investments, compared to stickier regulations at home," Tan said.

As of Aug. 1, US$1 was equivalent to 1,107.26 South Korean won.

S&P Global Ratings and S&P Global Market Intelligence are owned by S&P Global Inc.

Syed Salman Shah and Ranvir Vala contributed to this article.