BLOG — Feb 24, 2021

Canadian inflation jumps in January despite lockdown restrictions

By Arlene Kish

- Consumer prices were higher from the previous month with a 0.4% month-on-month (m/m) rise on a seasonally adjusted basis (SA) and a stronger 0.6% m/m jump on a non-seasonally adjusted basis (NSA).

- Annual inflation quickened to 1.1% year on year (y/y) SA and 1.0% y/y NSA.

- Two of the three Bank of Canada core consumer price inflation rates were higher, averaging 1.5% y/y.

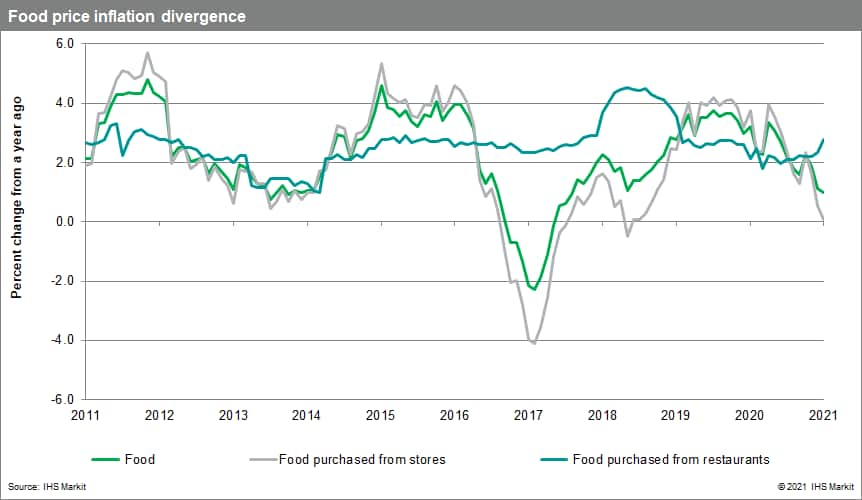

- Food price inflation came in stronger than expectations and higher gasoline prices contributed to higher inflation pressures.

- The January blahs were made all the worse for consumers by stronger inflation pressures, albeit at a relatively modest rate. Looks for this trend to persist in the near term.

Although food price inflation has decelerated for the past three months, the slowdown was weaker than expected. This was in part due to a boost in food prices purchased at restaurants, hitting a 22-month high of 2.8% y/y. The price increase in the food purchased from stores was significantly slower at 0.1% y/y.

Inflation was driven higher by the 1.9% y/y lift in services. The 31.1% y/y leap in travel tours contributed to the overall annual price increase despite recommendations against non-essential travel. This boosted the recreation, education, and reading price index. Elsewhere, the upward swings in home prices are putting more upward strain on homeowners' replacement costs, advancing 5.8% y/y. Plus, purchases of passenger vehicle prices climbed 2.9% y/y with the release of new motor vehicle models. The low 3.3% y/y decline in gasoline prices and higher costs for vehicle parts and repairs lifted the cost of operating passenger vehicles for the first time since February 2020. While demand remains soft, consumers are getting a break on spending with a 4.1% y/y decline for clothing and footwear.

With the economy reopening, there is a greater chance that businesses will pass on higher prices to consumers, as many business operators face challenges with slow business activity and higher input costs, thanks to rising producer price inflation. However, as of now, total and core inflation remain low, which means the Bank will focus mostly on the economic recovery and on lagging industries and sectors. The anticipated quick rise in annual gasoline price inflation will pull total prices higher, but as usual, the Bank will view this as a temporary price pressure. There is still plenty of economic slack that needs to be absorbed. The stronger-than-expected takeoff in January inflation will lift the 2021 inflation outlook, closer to the 1.5% y/y range. The Bank of Canada is expected to remain on the sidelines for a while longer until the first rate hike in mid-2023.