31 Mar 2017 | 19:34 UTC — Insight Blog

Warm winter keeps natural gas prices subdued, production growth in question

The natural gas market has worked itself into an interesting situation recently. The combination of a warm winter in 2015-16, declining associated production, lack of new infrastructure and coal retirements have created a perfect storm for a very challenging year to evolve in 2017. Although many of the potential issues were alleviated by yet another warm winter, attention is now starting to turn toward the supply side of the equation, and it’s having an impact on the shape of the natural gas forward curve.

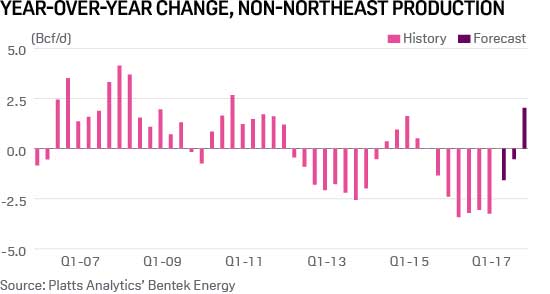

The problem is simple: production needs to grow in 2017, and the growth needs to come from somewhere other than the Northeast, something that has not happened on an annual basis since 2011. Production will be called upon in a major way this year, but associated gas may be largely left out of the mix as oil prices have stagnated around $50/barrel.

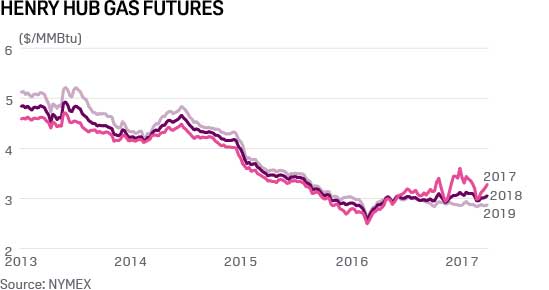

However, the market is asking for dry gas production to grow in the face of a backwardated curve, as natural gas prices beyond 2017 have stubbornly hung below break-even drilling costs for the majority of basins in the US. The specter of new infrastructure and inexpensive Northeast production hitting the market has pulled the back end of the curve lower, creating a paradox for producers. Why ramp up production throughout 2017 when the prospects over the next three to four years seem to challenge returns? Or rather, could the recent momentum we’ve seen in dry gas basins be short-lived as producers try to capture as much of the short-term rally as possible before pulling back over the next few years?

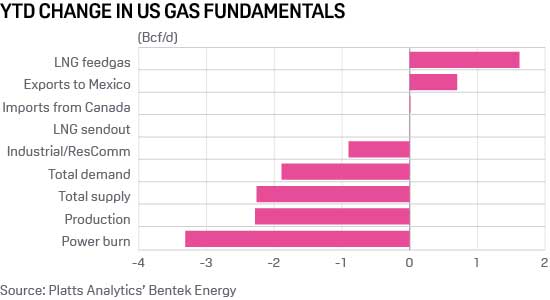

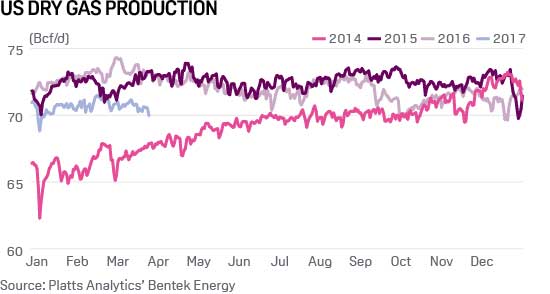

The recent rally and subsequent pullback have been driven by several factors. After reaching all-time highs in November, storage inventories quickly normalized due to a colder-than- normal December. However, a warm second half of January and an extremely warm February has helped quell any concern about inventories, but arguably it is doing more harm than good. Market fundamentals are decidedly tighter this year despite a significant reduction in power burn demand, driven by higher natural gas prices and higher hydro output along the Pacific Coast. Most notably, production has been lagging significantly behind year-ago levels, and export demand is trending more than 2.3 Bcf/d higher than a year ago.

The issue is that with this higher demand and lower production, the market seems poised to inject less into storage than last summer, and because inventories are trending roughly 400 Bcf below last year’s levels already, this means inventories could end up at their lowest summer-ending carryout in almost a decade.

The real problem here is that the price incentive to resume drilling operations in these dry gas plays has already played out, but we haven’t seen the production response expected. If the marginal basin for dry gas production outside of the Northeast is the Haynesville, it will need to be the area that provides the marginal molecule. The 2017 Henry Hub strip pushed above the break-even for the average Haynesville well toward the end of 2016. And sure enough, producer activity ramping up during this time seems to be a direct response to try to capture the returns on higher natural gas prices in 2017. In fact, we’ve already started to see some production in light of this increased activity, as Haynesville production is up nearly 0.4 Bcf/d since December.

Logically, this makes sense; the environment is ripe for a dry gas producer in the Southeast to ramp up production. The next 12 month’s strip is above break-even costs, but after that, the next four years are below break-evens, meaning it’s better to produce this year than wait to ramp up activity. With this in mind, it’s possible that the increase in rigs from the low in Q3 2016 into Q1 2017 likely represents the majority of the production response we can expect at these price levels. As mentioned, the increase drilling activity has helped push Haynesville production higher, but it hasn’t been enough to offset declines elsewhere, which has caused total US dry gas production to decline by nearly 0.3 Bcf/d from December.

This is a conundrum for the 2017 gas market. It is now unclear how the market will respond to provide enough incentive for dry gas production in the Haynesville to grow. It will be challenging to move the 2018 Henry Hub futures strip much higher, because new infrastructure projects such as Rover Pipeline, Columbia’s Leach Xpress and the Northern Access 2016 Expansion project are poised to bring significant production from the Marcellus and Utica onto the market in 2018. It is clear that something has to give this year.