28 Nov 2019 | 15:13 UTC — Insight Blog

Five global trends for the ferrous and steel sectors

S&P Global Platts hosted its Ferrous & Steel Outlook event in Singapore last week. Here are five key takeaways from the event.

1. China winter steel production cuts of less concern than property sector

Chinese mills have been less inclined to restock iron ore for fear they will be ordered to cut crude steel or sintering production over winter to reduce emissions, which would curb demand for iron ore and pull down prices.

S&P Global Platts China steel analyst Jing Zhang argued that winter output cuts are likely to be fairly mild this winter. Steel production rates will depend on margins that will largely be driven by property construction demand.

Citigroup head of iron ore trading Habib Esfahanian said China’s property sector should grow around 4%-5% next year, helping to support iron ore prices in the range of $70-$90/mt CFR.

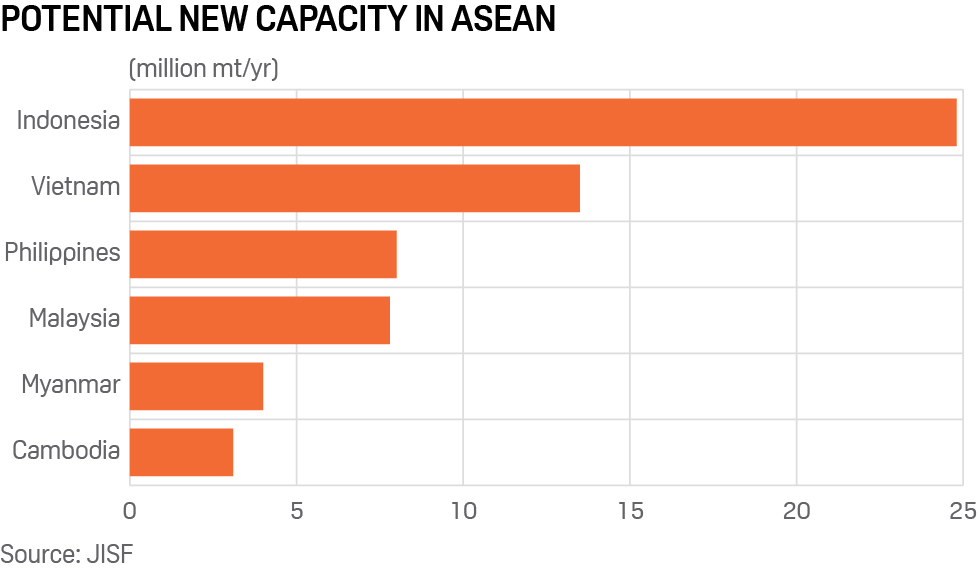

2. Southeast Asia could be the next steel overcapacity region

If all of the planned steelmaking projects come to fruition, Southeast Asia could add another 61 million mt/year of steel capacity in coming years, Mike Fujisawa, principal of JFE Steel’s overseas planning department, highlighted in his presentation.

Much of the new capacity will be Chinese-owned, with large projects planned for the Philippines and Malaysia. Fujisawa said new capacity slated for Malaysia was “comparable to its current steel use,” and steel market participants in the region were growing increasingly worried. If production outpaces demand, the new capacity will likely be exported, adding to supply pressure in Asian markets.

3. India unlikely to become a sizable coking coal producer

India is self-sufficient in iron ore but needs to import metallurgical coal. This truism seems unlikely to change in light of activity around India’s mine lease auction program. Private companies in India can only gain access to mining leases via the e-auction process.

To date, 24 of the 68 mining blocks that have been auctioned are iron ore mines, of which four are operating, according to Tata Steel’s head of raw materials, Somesh Biswas. But there have been no takers for coking coal leases in the last few tranches auctioned off.

Coking coal blocks contain non-coking material but owners are prohibited from selling coal to power stations; high upfront payments for the leases are non-refundable; and many blocks have communities living on them who farm the land. As a result, India will remain a coking coal importer.

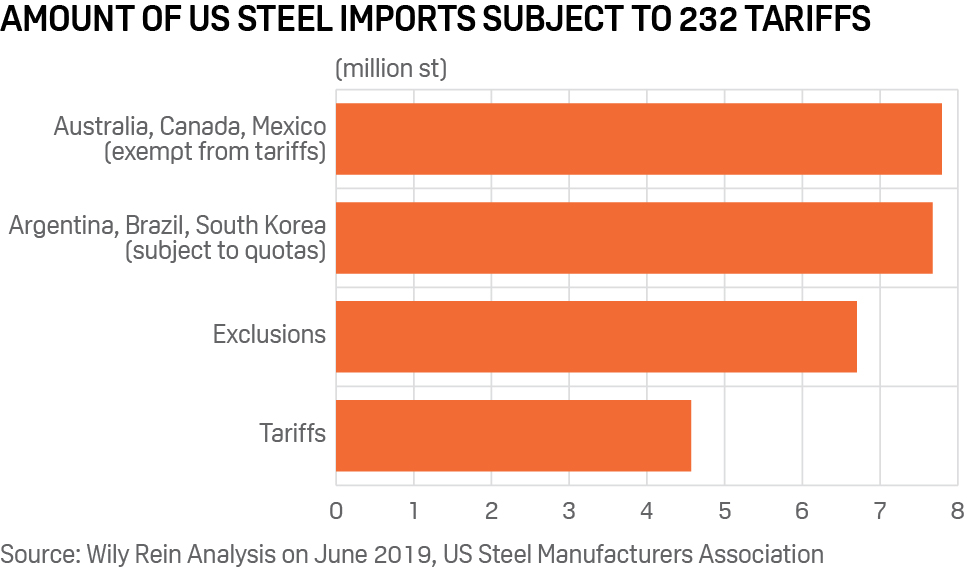

4. US steel import tariffs not as draconian as thought

The Trump administration’s imposition of import tariffs on steel following the Section 232 investigation last year was seen by many as the catalyst for the ongoing global trade tensions.

Trump was raising the drawbridge and protecting US business – in this case, the steel sector. But trade statistics presented by Philip Bell, president of the Steel Manufacturers Association (US), showed that only 17% of US steel imports were subject to the tariffs in June when the analysis was carried out.

Australia, Canada and Mexico (29% of imports) are exempt from the tariffs, Argentina, Brazil and South Korea (29%) were allowed a quota, and a further 25% of imports were subject to exclusions from the tariffs. Further, the US still imports more than 25% of its steel, down from 30.5% in the year to mid-2018.

5. Indian consolidation needs to move from flats to longs

India’s steel sector has undergone significant consolidation over the past 18 months with international heavyweights such as ArcelorMittal and Nippon Steel coming into the country via acquisitions.

Close to one-fifth of India’s steel capacity has changed hands as a result of the consolidation process, according to CRISIL Research director Rahul Prithiani. India’s flat steel sector will comprise four major players, shrinking from six previously. This will enable the producers to lift capacity utilization rates, better negotiate for raw materials, and improve margins.

India’s long steel production is more fragmented, with many smaller “secondary” producers. Prithiani expected weaker players to exit the market, with better quality assets snapped up by the large steel companies, giving them greater market share in India’s long steel sector.