26 Jun 2019 | 18:05 UTC — Insight Blog

As Texas temperatures rise, will ERCOT electricity prices boil over?

By Travis Whalen and Manan Ahuja

When record-setting heat swept across Texas in mid-July 2018, ERCOT only narrowly avoided a blowout in power prices with the help of unusually low outages and the fortuitous arrival of a weekend.

This summer may be unlikely to get as hot as last year, but shrinking reserve margins continue to emphasize the possibility of surging summer prices. Taking into account increasingly tight reserve margins, upside under ERCOT’s recently revised shortage pricing formula, and higher dependence on wind generation, markets currently appear to understate that risk, S&P Global Platts Analytics forecast shows.

Capacity and price signals

ERCOT is a unique market that reflects Texas’ love of self-sufficiency. The bulk of the region is deregulated, meaning that power generation is owned separately from transmission assets. End-users are mostly limited to buying electricity from the utility in their region, but that electricity can come from any number of providers.

But ERCOT is also one of only two energy-only markets in the US, so these power producers earn revenue only from energy sales, rather than supplementing that with payments for available capacity, a practice common to other regional US markets.

As a result, companies are incentivized to retire or build generation via energy prices and their reflection in the forward markets.

This dynamic contributed to the current summer’s tight reserve margins of 8.6%. In comparison, the next lowest reserve margin this year is NYISO at 19.3%, and even ERCOT’s target was set at 13.75% reserves. These tight conditions could lead to wholesale price spikes during peak demand and/or high supply outage periods.

In order to properly value generation during these shortage hours, ERCOT relies on an Operating Reserve Demand Curve (ORDC) that imposes an additional price based on the level of available reserves at any given time. Between the two components, base power prices and shortage adders, ERCOT sets a price cap of $9000/MWh. That figure stands far above FERC-regulated markets in the US. FERC has a standard cap of $1000, although bids above that are allowed when costs are shown to be greater. The FERC shortage cap stands at $2000.

In addition, ERCOT revised the ORDC rules starting this past March, to trigger more regularly – at a higher reserve level – based on guidance from the Texas Public Utilities Commission, with a similar adjustment scheduled to go into effect next year.

ERCOT bucks demand trend

While tight supply and demand occurs largely by design in ERCOT, the region also boasts the strongest load growth anywhere in the country. Driven by oil- and gas-related activity along with general population growth, ERCOT weather-adjusted load – which attempts to estimate load under seasonally normal weather conditions – has consistently grown by at least 2% per year at a time many other regions are flat or in decline.

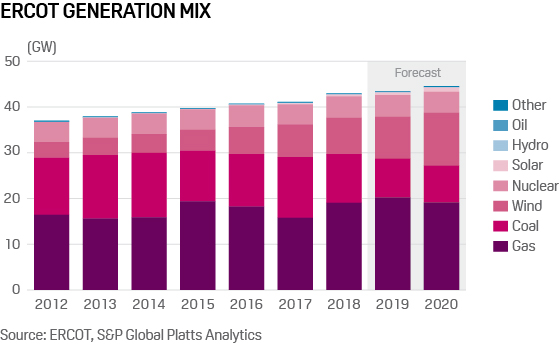

It’s not only the demand side of the equation that’s seeing major changes. Despite its reputation as a global oil and gas hub, Texas also continues to rely more heavily on wind generation each passing year. While that means lower emissions and generally lower prices, it also means managing increased variability during periods of shortage that could lead to price spikes.

Some critics have argued that such high price spikes could be avoided through mandated capacity margins and markets, as is common in other regions. However, these capacity prices are ultimately passed on to end-users. Proponents of the current energy-only market structure often point to the success in keeping retail power prices low in Texas, despite it being one of the only US markets to see consistent growth in demand.

Generators look to capitalize

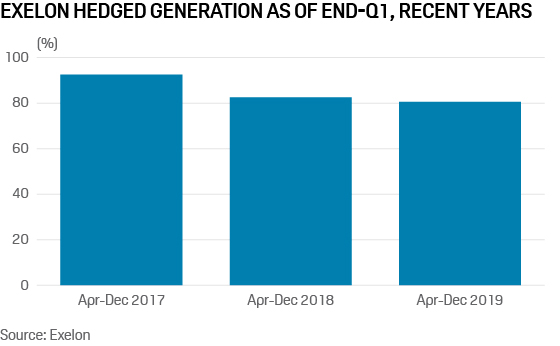

The hedged positions of large generation owners in ERCOT this summer also supports Platts Analytics’ view of potential for higher prices. As of end-March 2019,

Exelon’s ERCOT generationwas 79-82% hedged for Apr-Dec 2019. That comes in below hedging for the

same period last year(81-84%) and well below the

level seen in 2017.

NRG, which owns generation and serves retail load in ERCOT, also seems to have a similar positioning. According to the company’s recent 1Q19 earnings call, its retail exposure is completely hedged for the summer months, while on the generation side it is carrying unhedged generation into the summer. If prices go higher, NRG is positioned to benefit.

Details of NRG’s hedged positions in 2019 were unavailable. However, at end-March 2018 it had hedged 74% of generation and 102% of retail load for Apr-Dec 2018, in contrast to the end of March 2017 when it was over 90% hedged for its coal and nuclear generation portfolio in ERCOT for Apr-Dec 2017.

Vistra, which also owns generation and serves retail load in ERCOT, is carrying unhedged generation length into the important summer months as per its 1Q19 earnings call. The company also stated that the extent of backwardation in the ERCOT forward curves is dislocated from market fundamentals and likely a result of lack of liquidity in the forward years.

Such forward curves could hamper new fossil-fired generation projects, as well as renewables to some extent. The result could be continued low reserve margins in the coming years if load growth in Texas continues, as well as the sustained price risk that entails.