27 Mar 2020 | 16:04 UTC — Insight Blog

Insight from Moscow: Are Russia’s war chest and fiscal setup enough to combat OPEC+, coronavirus fallout?

The first few months of 2020 saw major changes to Russia’s political and energy landscape, as President Vladimir Putin proposed amendments to the constitution, the country’s crude production agreement with OPEC dramatically collapsed, and the coronavirus pandemic caused chaos on global markets.

Of these factors, the latter two are having a more immediate impact on the Russian energy sector, most evidently in the recent oil price crash.

Although the Russian energy ministry has released details on how much producers can increase crude output in April, the economic impact of the spread of the coronavirus could now derail these plans.

OPEC+ collapse

The collapse of the OPEC+ deal came as a surprise to many, with Russian officials indicating that they wanted to continue cooperation with OPEC right up to the eve of crucial meetings in March. Ultimately, significant differences of opinion proved too difficult to bridge.

Russia suggested extending the current agreement for the second quarter, and continuing to monitor the impact of the coronavirus outbreak on the market. Meanwhile many OPEC member states wanted deeper cuts, and proposed cutting an additional 1.5 million b/d. This would have likely doubled Russia’s cut from 300,000 b/d to 600,000 b/d, and it rejected the proposal.

In the background, changes to Russian domestic policy also influenced its position. Russian oil companies and the state budget alike are more resilient to oil price volatility following introduction of the fiscal rule in 2017.

This rule has led to a decoupling of the ruble-dollar exchange rate from the oil price, significantly reducing revenue uncertainty, and resulting in a boost to oil exporters from the weaker ruble. Furthermore, it incentivizes maximizing crude production and has allowed Russia to build up its National Welfare Fund.

On the eve of the OPEC+ meeting, Putin said that Russia's international reserves stood at $563 billion, and there is a further $124 billion in the National Welfare Fund. He said that this is sufficient to ensure stability and meet all budget obligations, even with a possible deterioration in the global economy.

Since then much has changed, with the collapse of the OPEC+ deal and the impact of the coronavirus pandemic continuing to rattle the oil market.

Go deeper: Visit Platts Live for latest commodities and energy news, insights and webinars

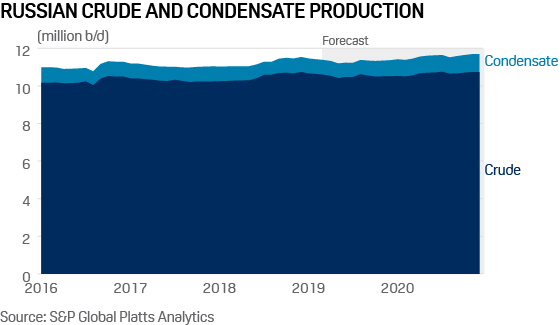

Immediately after the agreement collapsed, Russian Energy Minister Alexander Novak said that Russia could bring back 200,000 b/d to market in April, and this may increase to 500,000 b/d in the longer term. Russia’s crude and condensate output was around 11.289 mil b/d in February.

By mid-March the situation had already changed dramatically amid increasingly negative forecasts of the impact of the coronavirus on the global economy, and many countries shutting down. So far Russian oil and gas producers and suppliers say that they can comply with government measures to combat spread of the virus and run operations as normal, but the situation could change significantly in the next few weeks.

Markedly lower oil prices also raise the prospect of changes to tax breaks on crude production in Russia, which have become more prevalent in recent years. Analysts estimate that oil production from fields with tax relief increased from around 30% in the mid-2010s to over 50% in 2019. State giant Rosneft has been the main beneficiary of these discounts.

Sustained low oil prices threaten these tax breaks as they put pressure on the state budget, and the commercial viability of such projects.

Not all recipients of these discounts are likely to be affected in the same way. Analysts expect the government to continue to subsidize long-term strategic investments, including in the Arctic, even if prices remain low for a long period of time. Others are contingent on oil prices remaining above the budget threshold, however, which is set at $42.45/b for 2020. This includes Rosneft’s Vankor project and its joint venture with Gazprom Neft developing the Priobskoye oilfield.

Constitutional changes

So far Putin’s proposed changes to the constitution have had little tangible impact on the energy sector, with market conditions continuing to drive policy. Politics plays a big role in energy in Russia however, with oil and gas accounting for over 40% of Russia’s budget revenues in 2019, making the sector sensitive to political changes.

Analysts see the constitutional changes, which still have to pass a public referendum, as likely to result in Putin retaining power long after his current presidential term of office expires in 2024. This indicates that there may be a degree of continuity to leadership of the sector. Furthermore many longstanding ministers including Novak and Finance Minister Anton Siluanov remain in position.

Over the next few months much will depend on the impact of the coronavirus outbreak, how OPEC+ participants deal with an unpredictable market, and whether the state budget and oil producers are as resilient to volatile oil prices as they claim.