Summary

In this report, we add institutional accounts and separately managed accounts (SMA/wrap accounts) to the mutual funds analyzed in the S&P Indices versus Active (SPIVA) U.S. Scorecard. We aim to provide the institutional community with the ability to judge managers' true skill without the possible distortions that fees may create and to illustrate the similarities and differences between the performance of open-end funds, SMA/wrap accounts and segregated institutional accounts across categories.

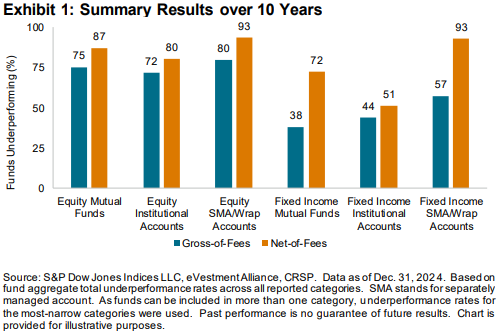

Exhibit 1 shows that among active institutional and SMA/wrap accounts, long-term equity underperformance rates were generally similar to those of mutual funds, with or without fees, while fees made a more significant difference in fixed income categories. After deducting fees, in all formats, at least 80% of equity funds and more than 50% of fixed income funds underperformed their respective benchmarks over the 10-year period ending Dec. 31, 2024.

Report Highlights

Within our most closely watched category of large-cap U.S. equity, 69% of institutional accounts and 67% of wrap accounts underperformed the S&P 500® in 2024 on a gross-of-fees basis, worse than the 65% reported for their mutual fund peers (see Sections II and III). Small-cap managers fared better, particularly within the SMA/wrap space, with only 19% of small-cap wrap accounts underperforming their respective benchmarks, even better than the 30% reported in mutual funds. These accounts were perhaps aided by their ability to opportunistically tilt toward outperforming large caps.

Over the long term, although underperformance rates were higher, mid- and small-cap underperformance rates for wrap accounts were significantly better relative to mutual funds, with only 57% of small-cap wrap accounts underperforming over a 10-year period, versus 62% and 82% reported for institutional accounts and mutual funds, respectively (see Exhibit 2).