“The whole is more than the sum of its parts.”

Aristotle

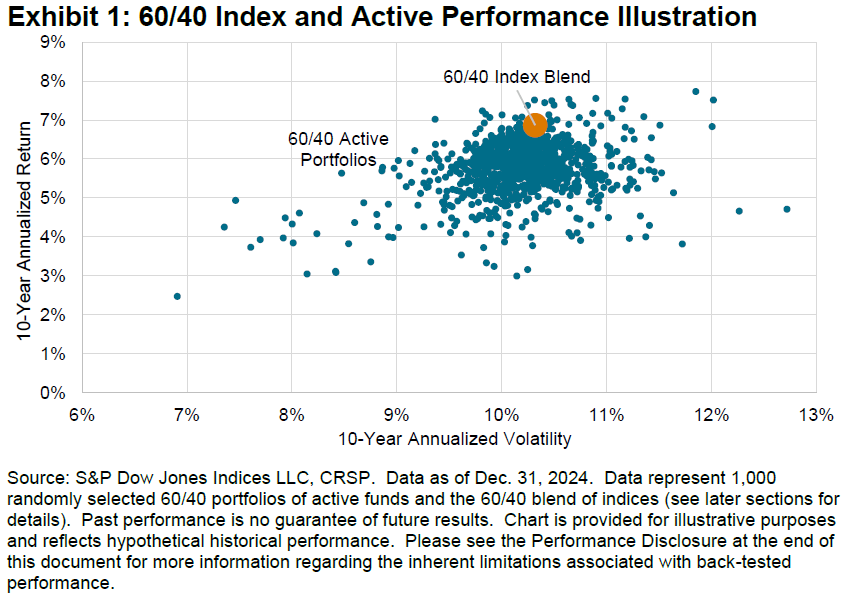

Since 2002, S&P Dow Jones Indices (S&P DJI) has evaluated individual active fund performance through our SPIVA® Scorecards. In this special report, we compare theoretical multi-asset portfolios of active funds to weighted blends of indices, finding that 96.9% of 60/40 portfolios of active funds would have underperformed equivalent blends of indices over 10 years. In many cases, portfolios of active funds not only produced lower performance, but also generated higher volatility (see Exhibit 1).

1. Introduction: The Whole and Its Parts

For more than two decades, S&P DJI’s regular SPIVA Scorecards have reported rates of success (or failure) among active managers striving to beat category benchmarks. There has been less focus on the resulting challenges for managers or advisors who select and allocate across multiple funds to build portfolios.

Natural questions arise when extrapolating SPIVA results into this real-world context; if individual fund categories have different rates of active underperformance, what is the appropriate way to measure success or failure of a hypothetical portfolio of active funds? Does the combination of active funds across asset classes offer diversification, reducing the influence of underperformers? Finally, if one could identify the set of outperforming funds in advance, in which fund categories would this ability be most amply rewarded? Ultimately, we seek to answer these questions and more by starting with one simple query: How do portfolios of active funds compare to similarly weighted blends of indices?

Individual active funds are rarely chosen in isolation; instead, they are more often selected as a component within a broader portfolio of funds representing different styles and asset classes. Some of these may be active funds, others may be passive. Our SPIVA and Persistence Scorecards have collectively shed light upon the prospects for achieving consistent outperformance within specific fund categories such as Government Bonds or Large-Cap U.S. Equities, but they say little about their potential combinations. This special report extends those results upstream to the arena of the fund selector or portfolio constructor tasked with blending multiple managers into a cohesive and high-performing allocation.