The S&P 500 is widely regarded as the most well-known and most frequently used benchmark of U.S. large-cap equities. The index includes 500 leading companies and covers more than 80% of investable market capitalization in the U.S. equity market. At the end of 2024, more than USD 20 trillion around the world was indexed or benchmarked to the large-cap U.S. equity barometer. Exchange-traded products based on the S&P 500 have been listed in various markets across the globe, but what creates the international appetite for U.S. equities, especially The 500®?

In this paper, we will:

- Outline the global significance of large-cap U.S. equities;

- Demonstrate the S&P 500’s distinct characteristics compared to the leading large-cap equity benchmark in Australia;

- Examine how incorporating large-cap U.S. equities could have helped improve the performance of hypothetical domestic Australian compositions, historically; and

- Highlight the historical benefits of taking an indexed-based approach to large-cap U.S. equities.

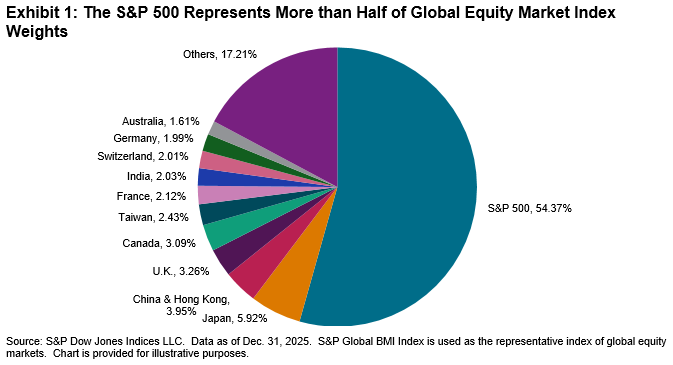

Significance of the S&P 500 in the Global Equity Market

The S&P 500 represents a significant part of global equity market capitalization, with index members representing more than 54% of the float-adjusted market cap of the S&P Global BMI as of Dec. 31, 2025. This was more than 33 times larger than Australia’s weight in the global equity opportunity set (see Exhibit 1). The scale of the large-cap U.S. equity segment also means that, among the 100 largest stocks in the S&P Global BMI, 74 were S&P 500 members.