1. What are some of the macro trends occurring in 2025, particularly in relation to the fixed income landscape? Additionally, what were some of the other key trends observed in 2024 and thus far in 2025?

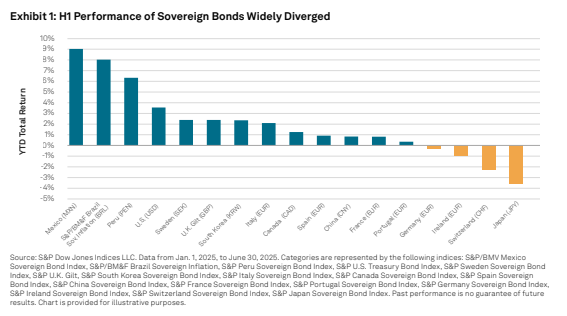

In analyzing the fixed income markets during the first half of 2025, three significant trends emerge. First, within the sovereign bond sector, various global forces have led to notable performance disparities among sovereign fixed income benchmarks. As shown in Exhibit 1, Latin American indices have notably excelled, with Mexican bonds achieving a remarkable 9% growth—an impressive figure in the fixed income arena. Additionally, Brazilian inflation-linked bonds and Peruvian government bonds also delivered high-single-digit returns during this period. Conversely, the S&P Japan Sovereign Bond Index experienced a decline of 3.6%, attributed to the Bank of Japan’s ongoing monetary tightening policy.

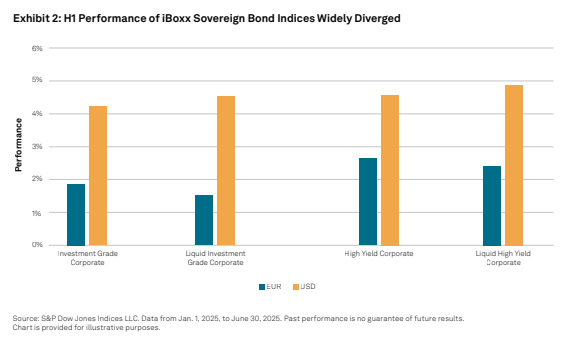

Second, U.S. corporate credit indices have shown strong performance, outperforming their counterparts in Europe in both the investment grade and the high yield space. As shown in Exhibit 2, this outperformance is particularly noteworthy given that credit spreads in Europe outperformed those in the U.S. However, taking duration risk in Europe resulted in significant loss, while it was rewarded in U.S. markets.

2. Could you explain some of the concepts around duration, liquidity and corporate credit? These tend to be sources of outperformance, or alpha, for active fixed income managers.

The traditional sources of excess returns in the fixed income markets have historically related to three key factors, known as the three Ts: time, trust and trading.

The first factor, time, involves taking on term or interest rate risk, which is reflected in the relative performance of longer-dated bonds compared to shorter-dated bonds. The second factor, trust, relates to assuming more credit risk by moving down the credit spectrum from sovereign bonds to investment grade and high yield bonds. The third factor, trading, pertains to exposure to illiquid bonds, measured by the performance of investment grade and high yield indices against their more liquid counterparts.

In examining the performance of these three Ts in Europe during the first half of the year, we find that trust and trading have contributed positively to returns. In contrast, time, which involves taking on duration risk, has significantly underperformed. This decline is largely due to the eurozone's fiscal loosening, particularly in Germany, which has led to increased bond issuance and a rise in high-duration yields.