Launched in 1994, the S&P 600 is designed to track the performance of small-cap U.S. equities and has outperformed the Russell 2000 by an average of 1.6% per year over the past 25 years. This outperformance highlights the importance of index construction; unlike the Russell 2000, the S&P 600 uses an earnings screen—companies must have a track record of positive earnings before they are eligible to be added to the index. The resulting quality factor exposure has played a significant role in explaining the S&P 600’s relative returns, and why it has been a harder benchmark for active managers to beat.

RELATIVE RETURNS COMPARISON: S&P 600 VERSUS RUSSELL 2000

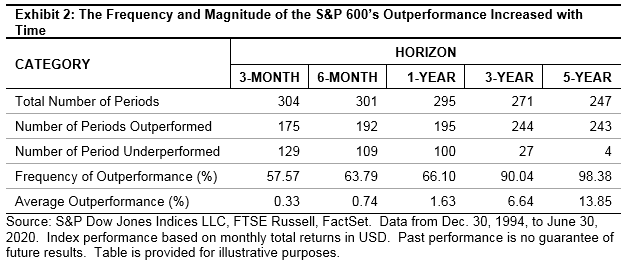

Exhibit 1 shows the cumulative total returns for the S&P 600 and the Russell 2000 since Dec. 31, 1994. The S&P 600 posted higher annualized returns and lower volatility than the Russell 2000 over the entire period, and it outperformed the Russell 2000 in 17 of the past 25 full calendar year periods.

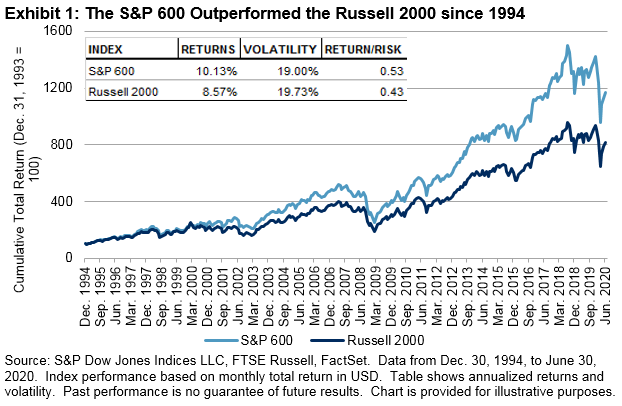

Exhibit 2 shows that the S&P 600 also typically outperformed the Russell 2000 over other horizons. Indeed, the S&P 600 outperformed over most rolling three-month, six-month, one-year, three-year, and five-year periods, with both the frequency and magnitude of outperformance increasing over longer time horizons.