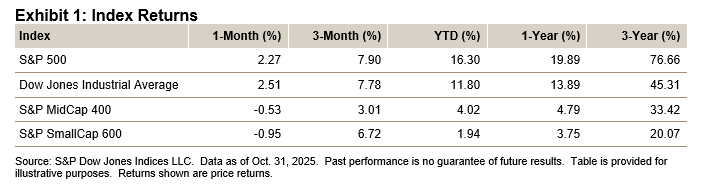

Key Highlights

- The S&P 500® was up 2.27% in October, bringing its YTD performance to 16.30%.

- The Dow Jones Industrial Average® gained 2.51% for the month and was up 11.80% YTD.

- The S&P MidCap 400® decreased 0.53% for the month, bringing its YTD level to 4.02%.

- The S&P SmallCap 600® lost 0.95% in October and was up 1.94% YTD.

Market Snapshot

The S&P 500 continued its upward trend, posting eight new closing highs for the month (a 6,920.34 intraday high and a 6,890.89 closing high) after eight new closing highs last month, breaking through the 6,700, 6,800 and 6,900 point levels (but not closing at or above 6,900), and posting 36 closing highs YTD and 46 closing highs since the Nov. 5, 2024, U.S. presidential election. The Dow Jones Industrial Average also continued up, posting seven new closing highs after posting six last month, as it broke through 47,000 and 48,000 (but did not close at or above 48,000). The October market momentum shifted to corporate profits, as operating earnings came in significantly stronger than anticipated and are expected to post a quarterly record of USD 599 billion, as sales, which were initially expected to decline, increased, and are now expected to set a new quarterly record of USD 4.49 trillion.

Tariff news continued to be volatile, with significant announcements, though the overall tone appeared to continue to be positive, with the U.S. and individual countries reaching agreements. U.S. consumers, both individual and corporate, have been able to absorb the tariff costs to date (with more expected to come through in November, as holiday pricing starts to be posted). The gains from the last two weeks of October (and new closing highs) left The 500™ up 2.27% for the month, as the gain from the post-tariff-announcement low (on April 8, 2025, of 4,982.77, when the S&P 500 was down 15.28% YTD) was a staggering 37.82%, with all 11 sectors up (Information Technology was the best, up 70.57% and Consumer Staples was the worst, up 1.37%), with 387 issues up (28 doubling and 90 up at least 50%) and 115 down (57 down at least 10%, 24 down at least 20% and 2 down at least 50%). Year-to-date, the S&P 500 was up 16.30% (17.52% with dividends), as 10 of the 11 sectors were positive (Information Technology was up 39.30% and Consumer Staples was down 0.58%), while 278 issues were up (average 27.84%) and 200 were down (average -15.15%), adding USD 8.532 trillion in market value (USD 0.882 trillion for October).

Momentum has now become a major investment theme, as corporate earnings set records and are expected to continue to do so at least through Q1 2026 (supported by lower taxes via USD 190 billion in corporate tax incentives from Trump’s budget bill), as individuals are expected to get an additional USD 150 billion in tax refunds in early 2026, which would likely lead to increased (or at least supported) spending. Adding to the optimism are employment levels; though expected to slightly decline, they are expected to remain strong overall, with AI productivity gains expected to make up for any loss in the employment base. Interest rates continued to be range bound (the 10-year rate defending the 4% level and short-term rate stable at the 3.8% level), as the FOMC reduced interest rates for the second consecutive month by 0.25% (to 3.75%-4.00%) by a 10-2 vote, with 1 vote for no change (Schmidt) and 1 vote for a 0.50% rate cut (Miran), as Fed Chair Jerome Powell said a December cut was “not a foregone conclusion,” with the Street still expecting another 0.25% cut at the December meeting and beginning to speculate on the start of asset purchases.

For October 2025, the S&P 500 was up 2.27% (3.53% in September, 1.91% in August and 2.17% in July), with 6 of the 11 sectors up (7 in September, 9 in August and 6 in July). Breadth declined, as 204 issues gained and 298 declined (248 and 255 in September, and 337 and 166 in August). Information Technology did the best for the month, adding 6.20%, as it was up 29.30% YTD and up 75.44% from the 2023 close. Materials did the worst, falling 5.10% for the month, up 2.23% YTD and up 0.37% from the 2023 close. Year-to-date, the S&P 500 was up 16.30% (17.52% with dividends), with 10 of the 11 sectors up, as 278 issues gained and 224 were down; Information Technology led the sectors, up 29.30% YTD, and Consumer Staples did the worst, down 0.58%.

For November 2025, the initial attention will be on reopening the U.S. government, along with back pay for employees, as the key funding issue at the root of the shutdown (which is at 31 days, and counting) remains an extension and/or adjustments to subsidies for the Affordable Care Act, which is expected to be the main headline but not the main trading driver for November. The Street expects an extension of the subsidies along with a partial scheduled phase-out of benefits for some individuals based on income, which may be done via a continuing resolution bill, after the Tuesday, Nov. 4, 2025, election.