KEY HIGHLIGHTS

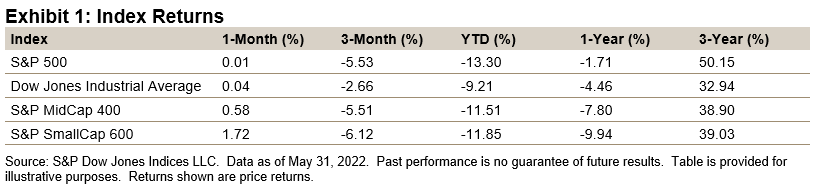

- The S&P 500® was up 0.01% in May, bringing its YTD return to -13.30%.

- The Dow Jones Industrial Average® gained 0.04% for the month and was down 9.21% YTD.

- The S&P MidCap 400® increased 0.58% for the month, bringing its YTD return to -11.51%.

- The S&P SmallCap 600® was up 1.72% in May and had a YTD return of -11.85%.

MARKET SNAPSHOT

The bear was—and still is—knocking at the door, although the 6.58% one-week rebound near the end of May (its best week since November 2020) put the trade back, permitting the S&P 500 to (technically) post a gain for May (0.01%). The index played cat and mouse with the bear; it traded at an intraday bear, but never closed there. The chase for weeks down also continued, but failed, though the S&P 500 did post seven consecutive weeks of declines (-14.18% cumulatively), an event that has only occurred four times since 1928, with the last one in March 2001 (-15.53%); the only nine-week decline was in 1923 (note the exchange was open on Saturdays back then). Thanks to the one-week rebound, the index posted a gain of 0.01%, after being down 7.78% (intraday, May 20), while it remained deeply in the red YTD (-13.30%), with strategists reducing target prices faster than oil prices went up at the pump. Economic data quantified significant price increases (CPI 8.3%, PPI 12.0%, Import Prices 12.9%), as housing slowed down (-5.9%, but prices were up 14.8% to a new record), with retail profits falling as consumers pulled back. Worse was the guidance, as companies forecast higher costs and admitted their “limitation” to pass them along (although operating margins remained high for Q1 2022, at 11.97%; the historical average is 8.21%), and the Fed notes said they may need to go beyond neutral (suggesting it could be more than “transitory”). But—and there is always a but—inflation is showing more signs that it has peaked, be it partially due to resistance, which in this case is not futile, but is recessionary. There does seem to be support levels across the market (which may be tested again), companies do appear to be starting up capital expenditures (be them from COVID-19 delays), employment remains high (according to the ADP and Monthly Employment reports), and consumers are still willing to spend—be it on leisure items and travel, which may eventually be reclassified as a one-time relief spending rally from COVID-19 hibernation.

As for the S&P 500, it posted a 0.01% gain after April's -8.80% decline and was down 13.30% YTD, as inflation fears struck individuals and profit concerns struck investors. While “we” all knew the economy would slow, the reality of the event caused selling (with buyers happy to exit as prices declined). The ability of the index to stay above 3,800, which still would keep it at a 2022 17.0 P/E (the current 2022 is P/E is 18.5), with 2022 earnings estimates having a 7.5% increase, spoke to those willing to buy for longer holding periods (with faith in the U.S. dollar averaging down). At this point, more bad news is likely ahead (inflation, interest rates, supply shortages, then supply backups once China opens up), which will test the pockets of those buying and the ability of the bulls to sell the story that inflation and supply issues are at or near their bottom, with the sun (and new highs) coming in 2023. Perhaps for now, anyone wanting to “buy in” needs to have liquidity and the ability to live past more volatility (and potential losses). As for the new risk/reward trade off, dividend stocks appear to have attracted more than the normal income seekers, which has helped those stocks (relatively), but those new investors may not be long term, so when the winds shift to growth, they may add to that selling.

At the root of the S&P 500 drop, up until May 20, was data from retailers that consumers were slowing on spending due to higher prices, and a growing belief that the Fed's interest rate increases would be quicker than expected, with the old 0.50% hikes and a potential 0.75% increase being replaced with 0.75% and a mention of 1.00%. Post-May 20, the index rebounded on more evidence that inflation may have peaked, and the underlying economy was still strong (and rich) enough to support spending (and profitability).