In the first quarter of 2022, there was uncertainty in fixed income markets due to rising inflation and interest rates, the ongoing Russia-Ukraine conflict and slower economic growth prospects following the unwinding of the central bank actions in 2020 to combat the COVID-19 pandemic. In such market conditions, tradable credit indices have yet again shown that they are an effective instrument for navigating credit exposure. We outline the Q1 2022 volumes linked to key iBoxx, iTraxx and CDX indices.

ETFs Tracking Key Credit Indices

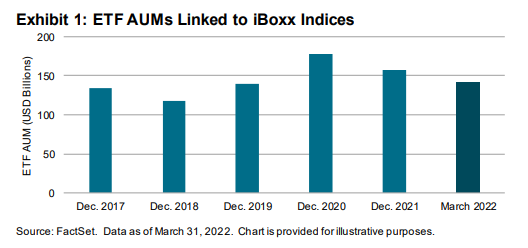

In 2021 and the first quarter of 2022, adverse fixed income market conditions affected investor appetite for long exposure to credit. Flows in ETFs tracking key iBoxx credit indices tend to act as bellwethers for market sentiment and have reflected investor paring of fixed income exposure.

In the following sections, we will examine ETF AUMs linked to key iBoxx credit indices across North America and Europe.

North America

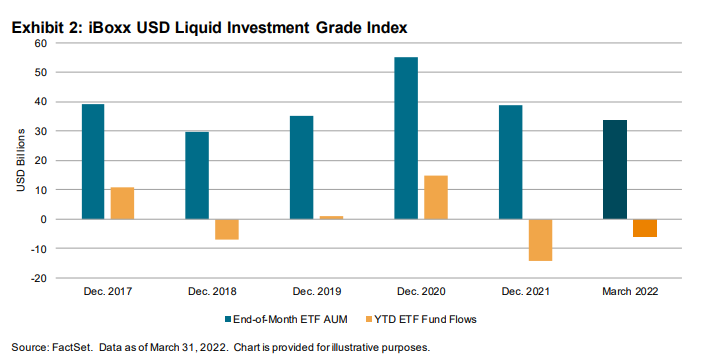

There was USD 38.9 billion in ETF AUMs tracking the iBoxx USD Liquid Investment Grade Index at the end of 2021, which was 29.3% less than at the end of 2020. ETF AUMs tracking the index ended Q1 2022 down 13.6% from year-end 2021. ETFs tracking the index had net outflows of USD 14.2 billion in 2021 and USD 5.8 billion in Q1 2022, which reversed course from the USD 15 billion and USD 1.2 billion of net inflows in 2020 and 2019, respectively. However, ETF AUMs tracking the index to close 2021 was still 10.9% higher than the close of 2019.