September 2025 Commentary

Market Overview

The U.S. Federal Reserve cut rates on Sept. 17 by 25 bps, citing slowing job gains amid a mild inflationary environment. On Sept. 18, the Conference Board Leading Economic Index (LEI) was released, declining by 0.5% in August owing to weak new manufacturing orders and consumer expectations along with an increase in unemployment claims. Against the backdrop, the 10-year U.S. Treasury rate, as measured by the iBoxx U.S. Treasuries Current 10 Year Index, ended the month at 4.19%.

Growth was relatively flat in the EU, with Germany experiencing a decrease in GDP of -0.3% in Q2 2025.3 GDP growth in the EU area was led by Denmark, at 1.3%, followed by Croatia and Romania, both at 1.2%.

A softer picture was also painted in Asia. The HSBC India Manufacturing PMI declined to 57.7 in September from 59.3 in August due to higher costs, despite increasing international orders.

In Latin America, Argentina faced significant economic headwinds as investor sentiment soured following political developments in Buenos Aires. This led to a sharp downturn in the local stock market, with the S&P MERVAL Index declining 10.70% in September, while authorities took steps to manage the currency.

September 2025 Performance

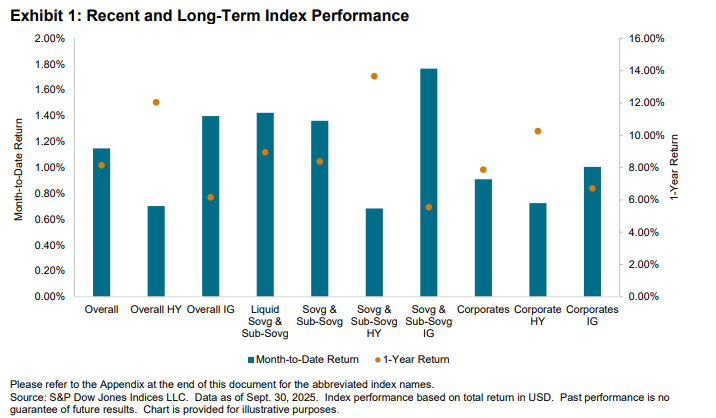

September witnessed a decline in monthly index performance, with the exception of Sovereign and Sub-Sovereign Investment Grade (IG) bonds, which rose by 50 bps to 1.77%. Overall IG also posted a modest increase of 18 bps, reaching 1.40%. In contrast, the Sovereign and

Sub-Sovereign High Yield (HY) bonds and Corporate HY bonds experienced the steepest declines in monthly performance compared to August, rising just 0.68% and 0.72%, respectively. Overall, Corporates HY underperformed its benchmark by 45 bps, closing the month at 0.70%. This trend underscores a market preference for higher-quality bonds and a risk-off sentiment amid volatility.

Among the top 10 emerging market economies, Mexico recorded the highest YTD performance at 13.21%, followed by Chile at 8.91% and Saudi Arabia at 7.97%. Mexico’s bond yields contracted by 32 bps when compared to August 2025, while Chile saw a yield contraction of 20 bps and Saudia Arabia of 15 bps. Yields contracted for all top 10 emerging market economies.