May 2022 Commentary

Inflation continued to be a prominent topic, as protectionism on domestic food supplies rose with a growing list of countries that imposed (or were planning to impose) bans on food exports, including India (wheat), Indonesia (palm oil) and Malaysia (chicken). On the other hand, there was good news from China, as Beijing and Shanghai began to take measures toward COVID-19 reopening, which should be a welcome boost to the economy (and global supply chain).

Global stock markets bounced back in the last few days of trading in May after a turbulent start to the month but still ended the month in the red, losing 0.10% (as per the EMIX All World Index). U.S. Treasuries (as per iBoxx $ Treasuries) ended the month relatively flat, returning 0.03%.

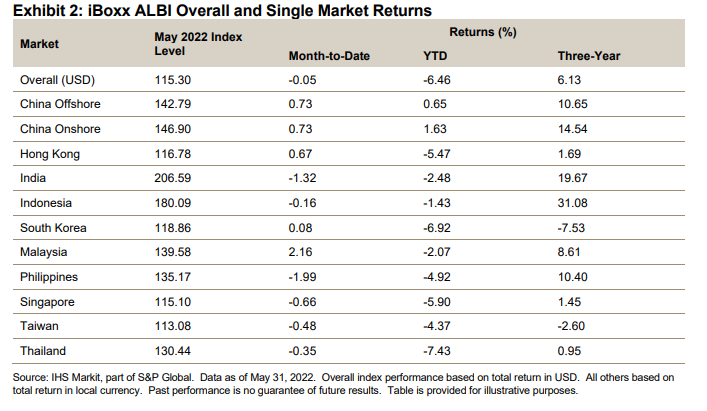

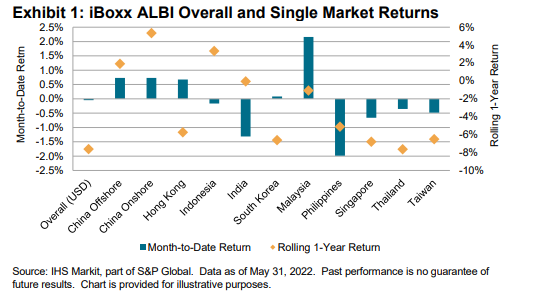

In Asian fixed income, the iBoxx Asian Local Bond Index (ALBI) (unhedged in USD) remained flat as well, returning -0.05%, with mixed performances in the sub-markets. Among the top gainers were Malaysia (2.16%), China Onshore (0.73%) and China Offshore (0.73%), while the Philippines (-1.99%), India (-1.32%) and Singapore (-0.66%) lost ground.China Onshore, China Offshore, Hong Kong and Malaysia saw gains across the yield curve, while India, the Philippines and Singapore declined across maturity buckets. The largest gains and losses were concentrated in the long end, with the Malaysia 10+ Year registering the highest gain of 3.30%. Meanwhile, the Philippines 10+ Year (-3.35%) saw the largest decline.

In May, the overall index yield increased by 2 bps to 4.01%. The yield of Malaysia tightened the most, declining 25 bps to 4.39%, while the Philippines climbed 48 bps to 4.88%. India remained the highest-yielding bond market in the index, offering 7.49%, while Singapore (2.90%) was the lowest-yielding market.