Blog — 3 Nov, 2022

Climate Scenario Analysis: Embracing Uncertainty with Conviction

This article is written and published by S&P Global Market Intelligence, a division independent from S&P Global Ratings. Lowercase nomenclature is used to differentiate S&P Global Market Intelligence credit scores from the credit ratings issued by S&P Global Ratings.

Financial regulators across the globe are increasingly looking to identify, assess and understand how to mitigate climate risks in the financial system. As of October 2021, at least 31 central banks and supervisors are conducting or planning climate scenario analysis exercises, with the U.S. Federal Reserve recently announcing it will join this group early in 2023.[1][2] In addition, climate-related financial disclosures have been, or will be, mandatory in many countries (e.g., New Zealand, Switzerland, China and the G7 nations). [3]

Scenario analysis is employed as a well-established tool to address uncertainties over the future. There are challenges, however, including: the availability and standardization of data; the unconventionally long time-horizons involved with climate-related scenarios; the quantification of the financial and credit risk impact of risks and opportunities at an entity level; and, the interplay between physical risk events and energy-related transition plans.

In our view at S&P Global Market Intelligence (“Market Intelligence”), there is a subtler source of uncertainty that can have profound effects on the understanding and management of climate risks and opportunities — that is, model risk and how a chosen analytical approach influences the final modelled results for a given scenario. For energy transition scenarios, in particular, model risk stems from the inability to backtest these new financial and credit risk implications as corporations progressively invest in, and adopt, greener technology.

We have developed two analytical tools to quantify the financial and credit risk impact of climate change risks and opportunities: Climate Credit Analytics (CCA) and Climate RiskGauge (CRG). Both models employ a bottom-up approach, linking climate scenario variables to key drivers that impact firms’ financial performance and credit risk profiles. These two tools differ in the level of granularity needed for inputs, assumptions made and outputs generated.

- CCA is a suite of sector-specific quantitative models built in conjunction with Oliver Wyman.[4] The models combine company financials, industry-specific granular data (e.g., the production split of nickel, copper or lithium metals for metal and mining companies) and Oliver Wyman’s deep financial risk modelling expertise to project full financial statements. This approach is very flexible and provides users with the ability to alter and simulate multiple combinations of future company behaviors to 2050 (e.g., Will a company buy back its shares? Will it maintain the same capital structure as of today? Will it limit its leverage?).

- CRG is a transparent, flexible and scalable tool that focuses on the climate change implications of firms’ projected carbon emissions, costs, revenues, earnings and liabilities and translates them into a final credit risk impact over the chosen time horizon. CRG covers all industry sectors, including small-revenue companies that do not report full financial statements, and offers users the ability to simulate multiple company responses (e.g., Will companies carry on with business as usual despite a carbon tax increase? Will they reduce their emissions forcefully or adopt greener technology, incurring further abatement costs to reduce their emissions?). The model makes use of a small set of customizable assumptions, thus reducing the “butterfly effect” of too many options potentially amplifying the financial and credit risk impact over the next three decades.

Both models incorporate the Network for Greening the Financial System (NGFS) energy transition scenarios that can be used to benchmark results obtained on the same set of companies, when possible, and explore the uncertainty introduced by model risk.

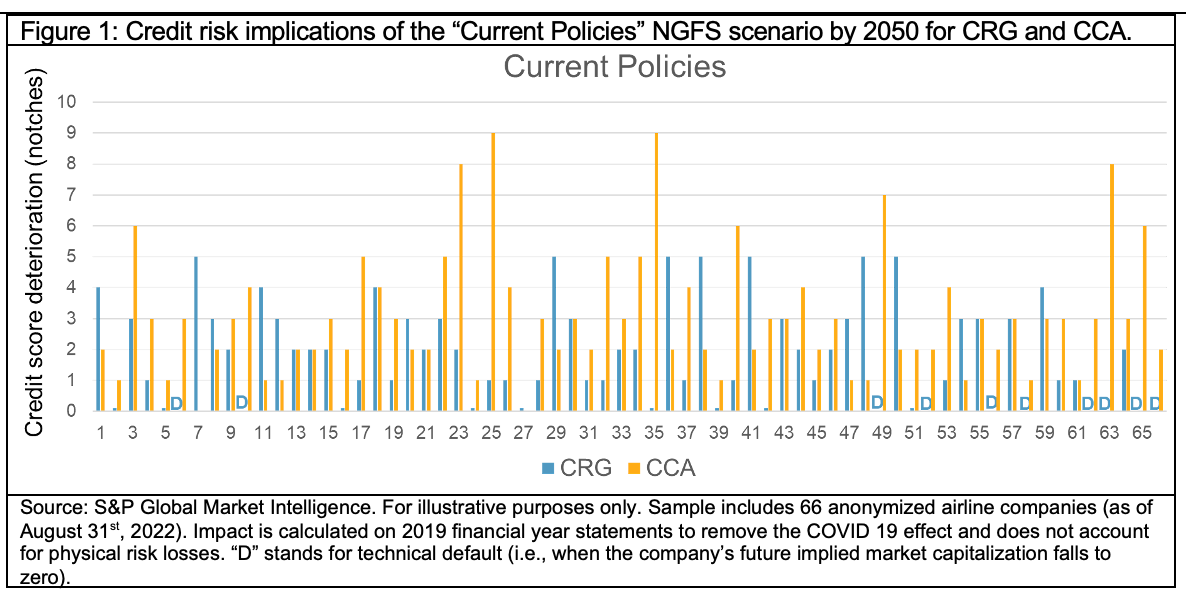

Figure 1: Credit risk implications of the “Current Policies NGFS scenario by 2050 for CRG and CCA.

Figure 1 shows the credit risk impact modelled via CCA and CRG to 2050 for an anonymized set of airline companies and a select NGFS scenario (“Current Policies”). While both models outputs align directionally across this portfolio, the credit score changes differ significantly for individual companies (e.g., company 35 or 63).

Model risk plays a critical role and is driven by: the underlying bottom-up approach selected to translate the energy transition scenarios into a full or essential financial impact; the number of assumptions made in simulating a company’s financial strategy to 2050; and, the robustness of the underlying data needed to run either model.

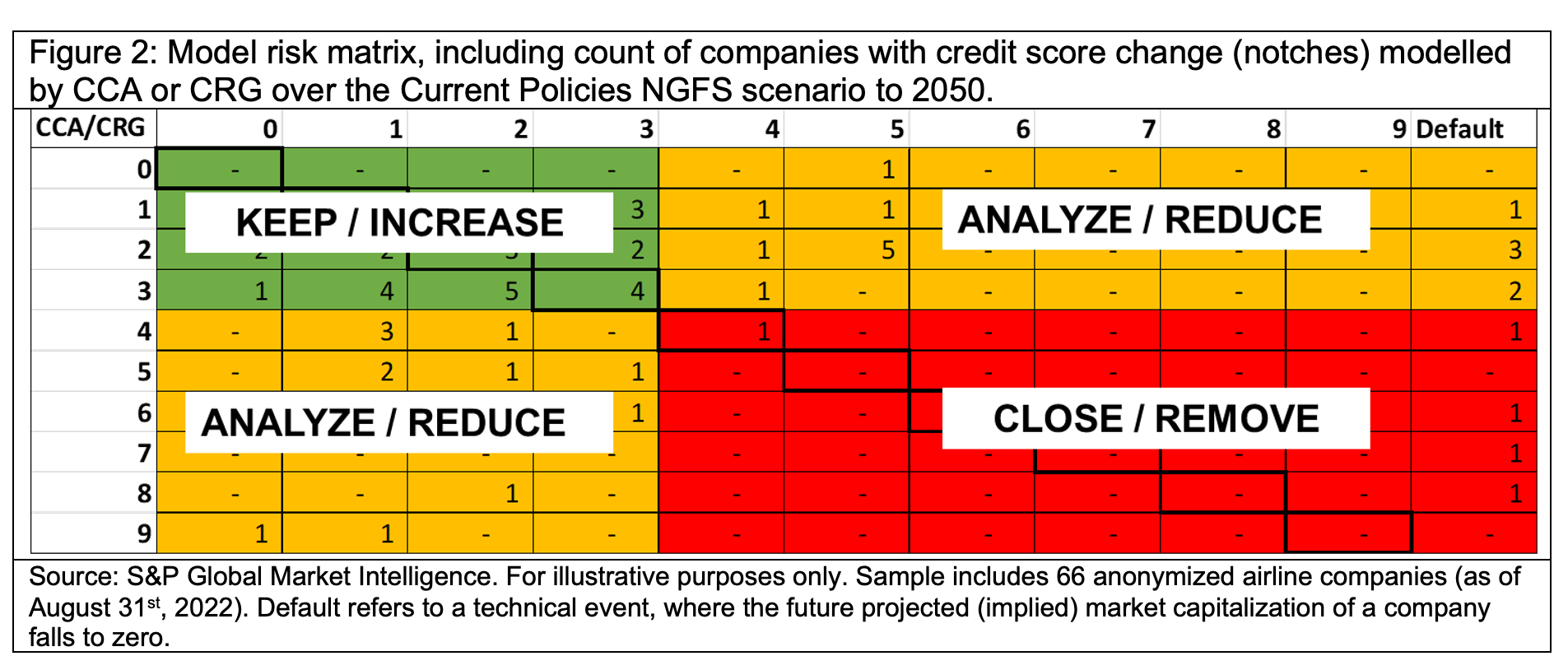

In this instance, it would be erroneous to take the average of the two outputs. A more solid analytical approach would consist in building a two-dimensional matrix, as shown in Figure 2, and partitioning it into four quadrants based on a user’s risk appetite.

Figure 2: Model risk matrix, including count of companies with credit score change (notches) modelled by CCA or CRG over the Current Policies NGFS scenario to 2050.

For the companies falling into the amber quadrants, an in-depth review could be warranted. Things worth considering could include:

- Data: Does the underlying data that is fed into each model represent good coverage? Are data gaps filled with peer-group averages that wash out important company-specific characteristics?

- Assumptions: Are a company's financial decisions that are put into the model going to hold, especially over very long-time horizons, or are a simpler set of assumptions needed? Are financial nuances missing by using a simpler set of assumptions, or should the original assumptions be fine-tuned?

- Financial and credit risk impact: Does the financial impact align to a users expert judgement, or does it show clear inconsistencies that suggest the presence of a butterfly effect?

An additional step to address these issues would help refine the structure of the matrix.

Please click here to learn more about these capabilities.

[1] Scenarios in Action: A progress report on global supervisory and central bank climate scenario exercises, Network for Greening the Financial System (October 19, 2021).

[2] Press Release, Federal Reserve (September 29, 2022).

[3] G7 Nations agree on mandatory climate-related disclosure”, Green Central Banking (June 8, 2021).

[4] Oliver Wyman is an independent third-party firm and is not affiliated with S&P Global or any of its divisions.