01 Jul 2016 | 18:01 UTC — Insight Blog

Liquidity flows faster for aluminum swaps

By Henry Van

Aluminum swaps have come a long way since August 9th 2013, when the first lots on the CME’s MW US Transaction futures contract were reported to have traded. By the end of May 2016, open interest for exchange traded CME premium contracts stood at 27,890 lots [735,250 mt], up 194% on year. Swap contract trade rose further in June, with large volumes traded for H2 2016 and H1 2017.

Midwest swap liquidity up 90% from May

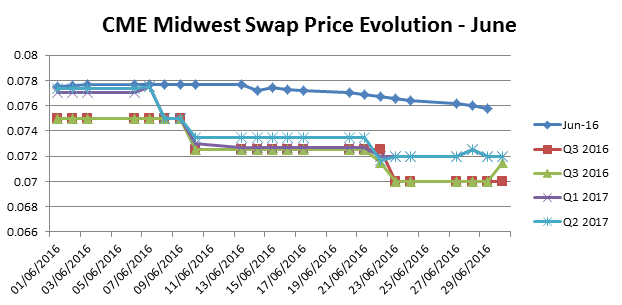

By the beginning of July, cleared open interest on the Midwest contract rose to 29,410 lots, excluding settled June contracts, with open interest for the Japanese contract rising above 2,000 lots for the first time. Throughout June, 7,905 lots were sold through the CME clearing mechanism across all Midwest swap contracts, a 91.31% rise from May volumes. The majority of interest was on the buy side of the contract, with some aggressive bidding on 2016 prompt contracts at under 7 cents/lb.

The market has pointed towards a growing tendency towards incorporating swaps in hedging strategy. According to a trader, “liquidity has picked up across the board [and] premium levels have dropped so inevitably customers are locking in as part of their rolling hedge program,” adding that some large traders had gone short on large volumes with the expectation that premiums would go lower.

While aggressive bidding has characterized recent trade movements, a second swaps trader said that Q3 and Q4 contracts would have to go significantly lower than the physical Midwest premium for larger volumes to be sold.

"The swaps have to be consistently cheaper than the physical price as this will provide incentive for more consumers to lock in good premiums," the second trader said.

At the beginning of June, contracts settling in the second half of 2016 traded in the 7.40-7.60 cents/lb range, but had moved to 7 cents/lb by month end. While the most recent bid [June 30] for the July contract was at 6.90 cents/lb, lower bids further out in 2016 led the second trader to predict that the premium forward curve would move into backwardation.

Compared with 2015, premiums were slightly higher with the July 2016 premium trading at around 6.50 cents/lb 12 months ago versus 7 cents/lb in late June.

While liquidity has risen in recent months, this has been clumped into specific trade days. Three days [June 10, 22 and 28] accounted for 70% of the volume traded over the month, with no cleared trades being done for nine working days in June.

The prompts over the H1 2017 period were the most heavily traded, with 3,742 lots, accounting for 51.20% of all June trades. Liquidity dropped over H2 2017, with only 1,050 lots traded on aggregate over the Calendar 2018 period.

![CME Midwest Swap Volume Traded - June [lots]](/content/dam/spglobal/ci/en/images/platts/general/2016/070116-cme-midwest-swap-volume-traded-june-lots.jpg)

Japanese contract buoyed by 2017 trade

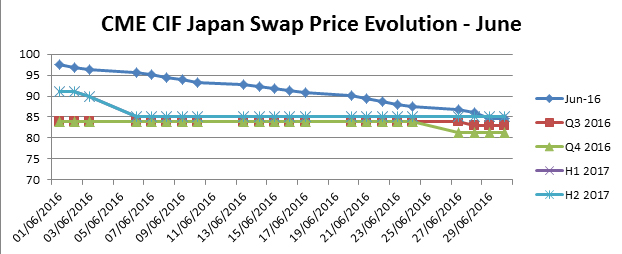

Open interest on the Japanese swap contract rose to 2,494 lots, with 970 lots [26,750 mt] traded, up 22.71% from May, with the market pointing towards the growing discrepancy between producer and trader prices as one reason for the rise in liquidity.

"Most interest in Japan is on the offer side as some consumers still have issue with quoting the contract, there is more traction but not much yet on spot contracts," a premium swaps trader told S&P Global Platts.

Two Calendar 2017 strips for Japan made up the majority of the volume traded on the contract. On June 2, 20 lots per month were traded through the CME clearing system at $90/mt and on June 7, 40 lots per month was traded at $85/mt.

The only 2016 prompts which traded in June were the November and December contracts, with 50 lots per month traded on June 27 at $80/mt and a further 50 lots per month on June 29 at the same price.

Despite offers from producers for Q3 2016 physical contract being above $100/mt throughout most of June, the quarterly physical Japanese contract had yet to settle by July 1, with recent bids at or below $90/mt rejected by sellers.

Nevertheless, traders commented that the downwards trend for the quarterly premium, having settled at $116/mt in Q2, was in line with the price evolution on the swaps curve, with contracts up to Calendar 2017 trading below $90/mt for most of the month.

Since the contract was launched in December, the July 2016 contract price has fallen from $120/mt at launch to $83/mt by the end of June 2016, with the price falling over Q2 despite a higher quarterly physical contract compared with Q1 2016.

Overall, recent market consensus points towards swap liquidity rising over the rest of the year, as consumers in the US begin to adopt more robust hedging strategies and tighter margins worldwide increase the need to lock in a greater proportion of purchase costs and sales prices.

![CME CIF Japan Volume Traded - June [lots]](/content/dam/spglobal/ci/en/images/platts/general/2016/070116-cme-cif-japan-volume-traded-june-lots.jpg)