SUMMARY

When an active manager beats a benchmark, how can we judge whether the result is a product of genuine skill or merely of good luck? Genuine skill is likely to persist, while luck is random and soon dissipates. Therefore one key measure of active management skill is the consistency of a fund’s outperformance.

The Persistence Scorecard attempts to distinguish luck from skill by measuring the consistency of active managers’ success. This report shows that, regardless of asset class or style focus, few fund managers have consistently outperformed their peers.

For example, only 3.84% of domestic equity funds in the top half of the distribution in 2015 maintained that status annually through 2019, significantly below what random chance would predict. Similarly, just 0.18% of the 2015’s top-quartile domestic equity funds maintained that performance over the next four years, again below random chance.

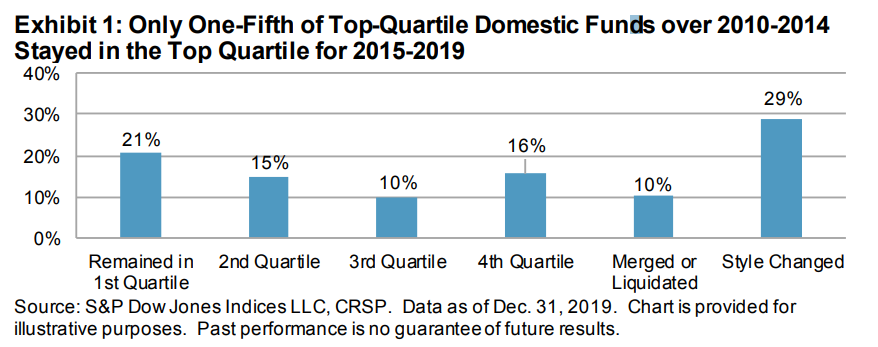

Lengthening the horizon to consider performance over two consecutive five-year periods, Exhibit 1 shows that the top-quartile domestic equity funds of 2010-2014 had little luck maintaining their top-quartile status for the 2015-2019 period. In fact, the most likely outcome for a top-quartile fund was liquidation or style change (39% together).

Compared with our previous reports, persistence appeared to improve over shorter investment horizons. Of the top-quartile domestic equity funds in 2017, 37.17% managed to stay in the top quartile annually through 2019. However, this persistence was inconsistent and decayed over time. For example, 61.34% of 2017’s top-quartile domestic equity funds were ranked in the top quartile for 2018. Rewinding the clock two years, just 3.38% of 2015’s top-quartile funds maintained that status in 2016.

There were few patterns to be found among equity funds’ performance, as the random distribution of fund performance over various time frames covered large-, mid-, small-, and multi-cap focused funds. One notable observation came from small-cap funds in the three-year period, as just 1.67% of 2014-2016 top-quartile funds remained in the top quartile for 2017-2019.

Unsurprisingly, the one pattern that did hold across equity funds was the tendency of the poorest funds to close. Fourth-quartile funds were generally the most likely to merge or liquidate over the subsequent three- and five-year windows, with nearly 38% of the bottom-quartile multi-cap funds of 2010-2014 disappearing by 2019.

Perhaps more surprisingly, style changes did not appear to be correlated with fund performance. Top, middle, and bottom performers within a category all generally had similar chances of style drift over three- or five-year periods. Multi-cap funds had the highest percentage of style change, with 31% making a change over three years and 40% over five years.

Fixed income funds showed similar results to equities, with rare pockets of one-year persistence and little evidence for consistent annual outperformance over longer periods. In 10 of the 13 categories considered, no top-quartile funds from 2015 maintained that status annually through 2019.

Transition matrices showed slightly more evidence of fixed income fund persistence. Over the three-year horizon, the most likely outcome for top-quartile funds in 11 of the 13 categories was to remain in the top quartile. In 10 of the 13 categories, this outcome occurred for 50% or more of top-quartile funds. Similar results existed over the five-year window. However, in many fixed income fund categories, fewer than 20 funds qualified within each quartile, perhaps leading to small sample size effects.