Summary

Since the first publication of the S&P Indices Versus Active Funds (SPIVA) U.S. Scorecard in 2002, S&P Dow Jones Indices has been the de facto scorekeeper of the ongoing active versus passive debate.

The SPIVA MENA Scorecard extends this analysis to the Middle East/North Africa (MENA) region by measuring the performance of actively managed MENA equity funds against their respective benchmarks over various time horizons, providing data on outperformance rates, survivorship rates and fund performance dispersion.

Year-End 2025 Highlights

Performance across MENA markets was mixed in 2025. The S&P Saudi Arabia declined by 9%, while the S&P Pan Arab Composite and S&P GCC Composite were up 4% and 2%, respectively. It was a relatively challenging environment for active managers across the region.

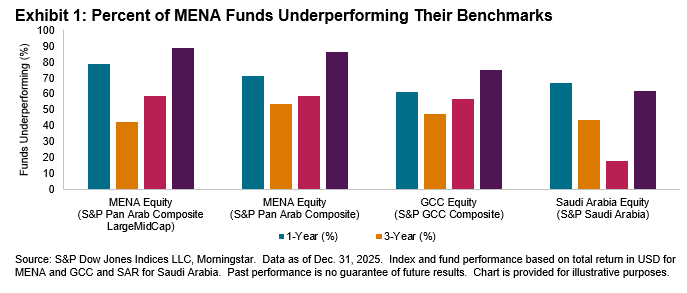

MENA

- 71% of MENA Equity funds underperformed the S&P Pan Arab Composite in 2025, while 79% underperformed the S&P Pan Arab Composite LargeMidCap Index. The latter index gained 5.7% versus 4.2% for the former. MENA Equity funds averaged returns of 4.1% (asset weighted) and 2.2% (equal weighted), indicating that larger funds outperformed smaller ones.

- Active underperformance increased over longer time horizons. Over a 10-year period, more than 80% of active MENA Equity funds underperformed both benchmarks.

- Survival rates for active MENA Equity funds were relatively low compared to other categories, with only 44% surviving over the 10-year period (see Report 2).