Summary

The SPIVA Latin America Scorecard measures the performance of actively managed funds across Brazil, Chile and Mexico against their respective benchmarks over various time horizons, providing statistics on underperformance rates, survivorship rates and fund performance dispersion.

Mid-Year Highlights

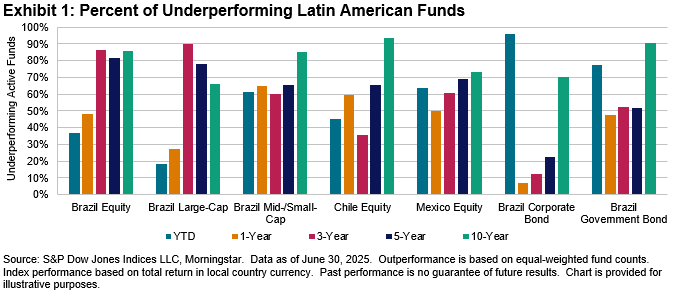

While most local Latin American benchmarks increased in H1 2025, active fund underperformance rates varied widely by country and asset class. Equity funds in Chile and Brazil fared better than most, with fewer than one-half of funds in each category underperforming. In contrast, most Mexico Equity and Brazilian bond funds trailed their benchmarks. Over the 10-year period, most funds underperformed in every category (see Exhibit 1).

Mexico

- The S&P/BMV IRT climbed 18.6% during the first half of 2025. Nearly two-thirds of active Mexico Equity fund managers (63.6%) underperformed for the six-month horizon. Over longer periods, outperformance remained challenging, with 50.0%, 60.5%, 69.0% and 73.2% of managers underperforming the benchmark over 1-, 3-, 5- and 10-year periods, respectively (see Report 1a).

- The median active fund return trailed the benchmark by 1.5% in H1 2025, outperformed by 0.3% over the 1-year period and underperformed by 1.0%, 2.7% and 2.8% for the 3-, 5- and 10-year periods, respectively (see Reports 3 and 5). Over the 10-year period, the threshold for top-quartile managers exceeded the benchmark by 0.5%.

- The survival rates of active Mexico Equity funds remained the highest in Latin America, at 100.0%, 100.0%, 100.0%, 97.6% and 82.9% over the six-month and 1-, 3-, 5- and 10-year periods, respectively (see Report 2).

- Funds with greater assets, on average, performed significantly worse than smaller funds in H1 2025. Average returns for Mexico Equity funds were 9.8% and 14.1% on asset- and equal-weighted bases, respectively (see Reports 3 and 4).

Brazil

- Brazil’s equity market finished the first half of 2025 in positive territory, with the S&P Brazil BMI rising 16.3% (see Report 3). Large caps, as measured by the S&P Brazil LargeCap, increased 13.3%, yet still trailed mid- and small-cap companies, as measured by the S&P Brazil MidSmallCap, which finished H1 2025 up 24.0%.

- Year-to-date through June 2025, 61.4% of active Brazil Mid-/Small-Cap funds underperformed their benchmark, while significantly fewer active equity funds underperformed their benchmarks in other categories, with underperformance rates of 18.5% among Brazil Large-Cap funds and 36.5% for Brazil Equity funds. Active managers within all categories produced even worse outcomes relative to their respective benchmarks over the longer 10-year period ending in June 2025, with underperformance rates of 86.0%, 66.3% and 85.3% in the Brazil Equity, Brazil Large-Cap and Brazil Mid-/Small-Cap fund categories, respectively (see Report 1a).

Chile

- Chile’s equity market proved to be one of the best performing in Latin America, with the S&P Chile BMI rising 23.0% for the first half of 2025 (see Report 3).

- Less than one-half of active Chile Equity fund managers (45.0%) underperformed the S&P Chile BMI over the first six months of 2025, but the underperformance rate varied over longer time periods, with 59.5%, 35.7%, 65.3% and 93.3% of active funds underperforming the benchmark over the 1-, 3-, 5- and 10-year periods, respectively (see Report 1a). The median Chile Equity fund outperformed the benchmark by 0.2% in H1 2025 and trailed by 1.5% over the longer 10-year period (see Report 5).

- Over the six-month period, the relationship between fund size and returns was inverse, with active Chile Equity funds rising 31.8% and 21.7% on equal- and asset-weighted bases, respectively. Over the 10-year period ending in June 2025, however, equal-weighted returns for Chile Equity funds averaged 8.4%, while asset-weighted returns averaged 8.3%, indicating that performance converged across funds with different asset levels (see Reports 3 and 4).

- Over the 10-year period, the threshold for top-quartile active fund managers trailed the benchmark by 0.5% (see Reports 3 and 5).