Since the first publication of the S&P Indices Versus Active (SPIVA) U.S. Scorecard in 2002, S&P Dow Jones Indices has been the de facto scorekeeper of the ongoing active versus passive debate. The SPIVA Japan Scorecard measures the performance of actively managed funds offered in Japan against assigned benchmarks over various time horizons, covering large-, mid- and small-cap segments, as well as international and global equity funds.

Year-End 2025 Highlights

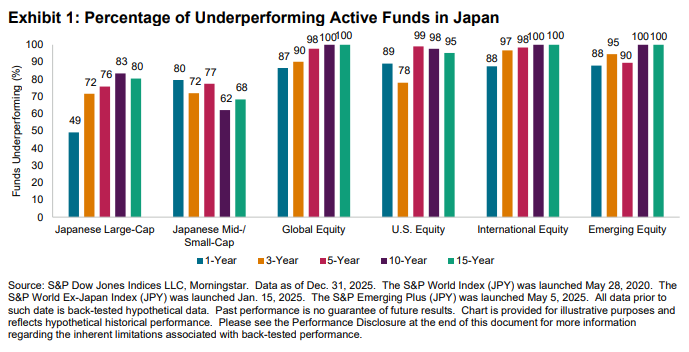

2025 proved to be challenging for active managers in Japan, with over 80% of funds underperforming their relevant benchmarks across five fund categories. The Japanese Large-Cap category was the notable exception, with a slim majority of funds outperforming—marking its best relative performance since 2017. However, long-term results remained unfavorable: across all categories, a significant majority of funds underperformed over the 15-year period ending in December 2025.

- Japanese Large-Cap Funds: The S&P/TOPIX 150 posted an impressive 25.0% gain in 2025, while actively managed Japanese Large-Cap funds achieved average returns of 25.4% and 9% on equal- and asset-weighted bases, respectively. In this category, 49% of funds underperformed the benchmark, representing the lowest underperformance rate since 2017 (see Exhibit 5). However, underperformance rates rose for longer time frames, exceeding 80% over the 10- and 15-year periods.

- Japanese Mid-/Small-Cap Funds: Actively managed Japanese Mid-/Small-Cap funds struggled to beat the benchmark amid its strong rally, recording an underperformance rate of 80%—the worst result since 2014. Nonetheless, they demonstrated better relative performance over longer horizons, with underperformance rates of 62% and 68% over the 10- and 15-year periods, respectively.

- Global Equity Funds: The S&P World Index posted a 7% gain (in JPY terms), while Global Equity funds delivered average returns of 15.0% and 13.9% on equal- and asset-weighted bases, respectively. During this period, 87% of Global Equity funds underperformed the benchmark, while 100% of funds lagged over 10- and 15-year periods.

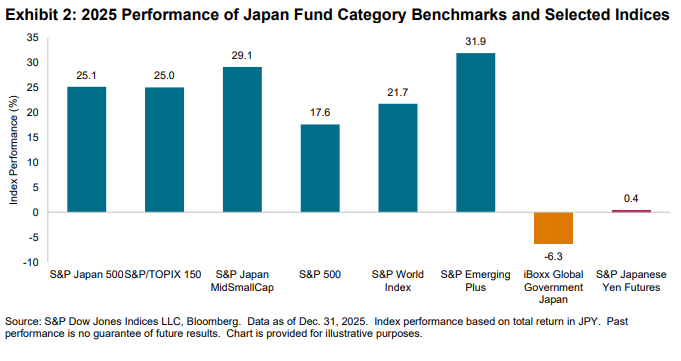

- S. Equity Funds: U.S. Equity funds domiciled in Japan faced significant challenges, with 89% of funds failing to beat the benchmark in 2025—the highest among all categories. They achieved an asset-weighted average return of 9.1%, compared to the S&P 500®’s 17.6% gain in JPY terms.

- International Equity Funds: International Equity funds recorded a majority underperformance rate of 88%, delivering an asset-weighted average return of 9% compared to a 21.5% gain in the S&P World Ex-Japan Index (in JPY terms). Underperformance rates generally rose over the longer term, reaching 100% over the 10- and 15-year periods.

- Emerging Equity Funds: Emerging Equity funds recorded a majority underperformance rate of 88% against the category’s new benchmark, the S&P Emerging Plus. These funds achieved an asset-weighted average return of 23.8%, compared to a 9% gain in the S&P Emerging Plus (in JPY terms). Underperformance rates increased to 100% for the 10- and 15-year periods.

- Fund Survivorship: Fund liquidation remained moderate overall, with 8% of active funds across all reported categories being merged or liquidated in 2025. Emerging Equity and Global Equity funds experienced the largest attrition rates, exceeding 5.0%. Over a 15-year period, more than half of all funds failed to survive (see Report 2).

Market Context

Global equities had another strong year in 2025. Developed market equities, as measured by the S&P World, advanced 21.7% in JPY terms, marking the third consecutive year of gains exceeding 20%. Emerging market equities outperformed—a trend not seen for some time—with the S&P Emerging BMI posting an impressive 31.9% gain.

Japanese equities also surged, with the S&P Japan 500 hitting a record high and posting a 25.1% gain. The rally was driven by the prospect of wage growth and increased consumption as inflation remained firmly above 2%, coupled with the resilience of Japanese corporate profits despite higher U.S. tariffs. The pro-growth policies of Prime Minister Sanae Takaichi bolstered optimism about the equity market, resulting in the strongest annual foreign inflow since 2013. However, this was not welcomed in the bond market; concerns about increased fiscal spending combined with the Bank of Japan’s policy normalization weighed heavily on Japanese bonds, with the iBoxx Global Government Japan finishing 6.3% lower.

Smaller Japanese companies outperformed their large-cap peers. The S&P Japan MidSmallCap climbed 29.1% compared to a 25.0% increase in the large-cap S&P/TOPIX 150, marking a notable departure from the trend of large-cap dominance observed in previous years.