Since the first publication of the S&P Indices Versus Active (SPIVA) U.S. Scorecard in 2002, S&P Dow Jones Indices has been the de facto scorekeeper of the ongoing active versus passive debate.

The SPIVA Canada Scorecard measures the performance of Canadian actively managed funds against their respective benchmarks over various time horizons, covering large-, mid- and small-cap segments, as well as international and global equity funds.

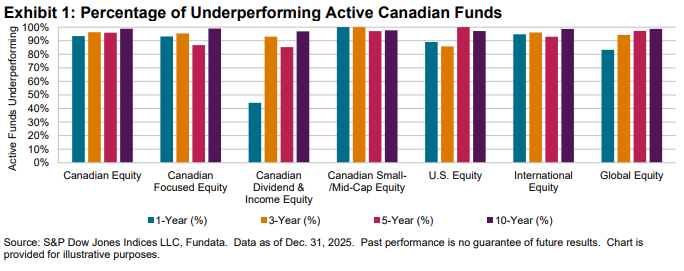

Year-End 2025 Highlights

In 2025, most of Canada’s active funds failed to surpass their respective indices. Across categories, an average of over 85.4% of active funds underperformed their benchmarks, including Canadian Equity funds at 93.4%, Canadian Focused Equity funds at 93.1% and Canadian Small-/Mid-Cap funds at 100.0%. Dividend & Income Equity funds fared better than most, with 44.2% trailing the benchmark (see Exhibit 1 and Report 1). Underperformance rates increased over longer time horizons.

- Canadian Equity Funds: The S&P/TSX Composite Index climbed 31.7% in 2025, while Canadian Equity funds gained 22.1% and 22.7% on equal- and asset-weighted bases, respectively. Underperformance rates hit 93.4% over the 1-year period, climbing to 96.3%, 95.9% and 98.8% over the 3-, 5- and 10-year horizons, respectively.

- Canadian Focused Equity Funds: The blended benchmark of 50% S&P/TSX Composite Index + 25% S&P 500® + 25% S&P EPAC LargeMidCap increased 26.0% in 2025, outperforming 93.1% of Canadian Focused Equity funds. Underperformance rates were 95.4%, 86.8% and 99.0% over the 3-, 5- and 10-year horizons, respectively.

- Canadian Dividend & Income Equity Funds: The S&P/TSX Canadian Dividend Aristocrats® Index rose 19.1% during 2025, while Canadian Dividend & Income Equity funds gained 19.5% and 19.2% on equal- and asset-weighted bases, respectively. Underperformance rates hit 44.2% over the 1-year period and reached 93.0%, 85.2% and 96.9% over the 3-, 5- and 10-year horizons, respectively.

- Canadian Small-/Mid-Cap Equity Funds: The S&P/TSX Completion Index gained 42.5% in 2025, and 100.0% of Canadian Small-/Mid-Cap Equity funds underperformed the index. Funds in this category gained 23.6% and 23.3% on equal- and asset-weighted bases, respectively, over the one-year period.

- U.S. Equity Funds: The S&P 500 increased 12.4% in 2025, and 89.1% of U.S. Equity funds underperformed the index. Few funds in the U.S. Equity category outperformed over the long term, with 85.8%, 100.0% and 97.1% underperforming over 3-, 5- and 10-year horizons, respectively.

- International Equity Funds: 94.7% of International Equity funds lagged the S&P EPAC LargeMidCap in 2025, and 96.1%, 93.0% and 98.7% underperformed over the 3-, 5- and 10-year periods, respectively.

- Global Equity Funds: The S&P World Index rose 16.3% in 2025 and Global Equity funds gained 11.0% and 11.2% on equal- and asset-weighted bases, respectively. Over the one-year period, 83.3% of funds in the category trailed the benchmark. Over the 3-, 5- and 10-year periods, 94.3%, 97.3% and 98.7% of funds underperformed, respectively.

- Fund Survivorship: Liquidation rates for all categories were in the single digits for the one-year period ending Dec. 31, 2025. Over the 10-year period, 47.1% of Canadian Equity funds merged or liquidated and 39.3% of funds disappeared across all categories (see Report 2).