Since the first publication of the S&P Indices Versus Active (SPIVA) U.S. Scorecard in 2002, S&P Dow Jones Indices has been the de facto scorekeeper of the ongoing active versus passive debate. The SPIVA Asia Ex-Japan Scorecard measures the performance of actively managed funds relative to relevant benchmarks, covering domestic equity, international equity and bond funds available in Greater China, Korea and Southeast Asia.

Year-End Highlights

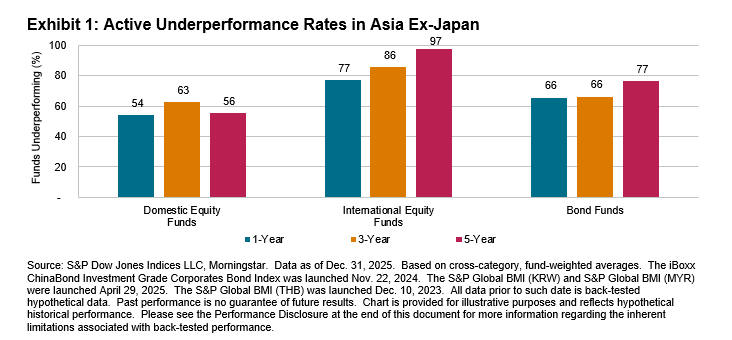

In 2025, a majority of actively managed funds in Asia ex-Japan underperformed their relevant benchmarks across domestic equity, international equity and bond fund categories. The rates of underperformance generally increased for longer time horizons. Exhibit 1 summarizes the results over one-, three- and five-year periods ending December 2025.

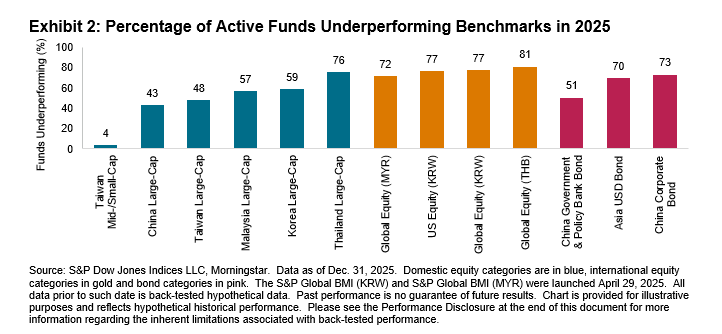

- As the global equity market experienced varied levels of performance and dispersion in 2025 (see Exhibits 3 and 4), actively managed funds in the region also exhibited a wide range of relative results across categories. Of the 13 reported fund categories, 10 witnessed a majority of funds underperforming their assigned benchmarks (see Exhibit 2).

- Domestic equity funds in Taiwan and China had higher beat rates. Only 3 out of 83 funds in the Taiwan Mid-/Small-Cap category lagged the S&P Taiwan MidSmallCap’s 17.2% gain, while 48% of Taiwan Large-Cap funds underperformed the S&P Taiwan BMI’s 31.2% increase. China Large-Cap funds also achieved majority outperformance—a notable improvement compared to recent years.

- In contrast, about three-quarters of Thailand Large-Cap funds struggled to surpass the S&P Thailand BMI’s weak -5.7% performance. Many Korea Large-Cap funds also failed to keep pace with the market amid a sharp rebound in which the S&P Korea BMI rose 87.2%.

- Outperformance was generally harder to find among international equity funds. Over 70% of global equity funds in Korea, Thailand and Malaysia underperformed the S&P Global BMI in their respective currencies. Korea-domiciled U.S. equity funds recorded a 77% underperformance rate against the S&P 500® (KRW).

- A majority of active funds underperformed in all three reported bond categories. More than two-thirds of Asia USD Bond funds trailed the iBoxx USD Asia ex-Japan’s solid 7.7% gain. Chinese onshore bond funds also struggled to differentiate themselves as yields remained suppressed.