EXECUTIVE SUMMARY

Chinese investors tend to have high exposure to domestic equities and low exposure to international equities. This home-country bias is common among investors globally. U.S. equities represented 45% of the global equity market, as of Dec. 31, 2020. Underallocation to international equities, including U.S. equities, means Chinese investors may be foregoing potential diversification benefits.

In this paper, we:

- Discuss the global investment opportunities for Chinese investors and the potential results of investing globally;

- Introduce the S&P 500 and explain how it is constructed;

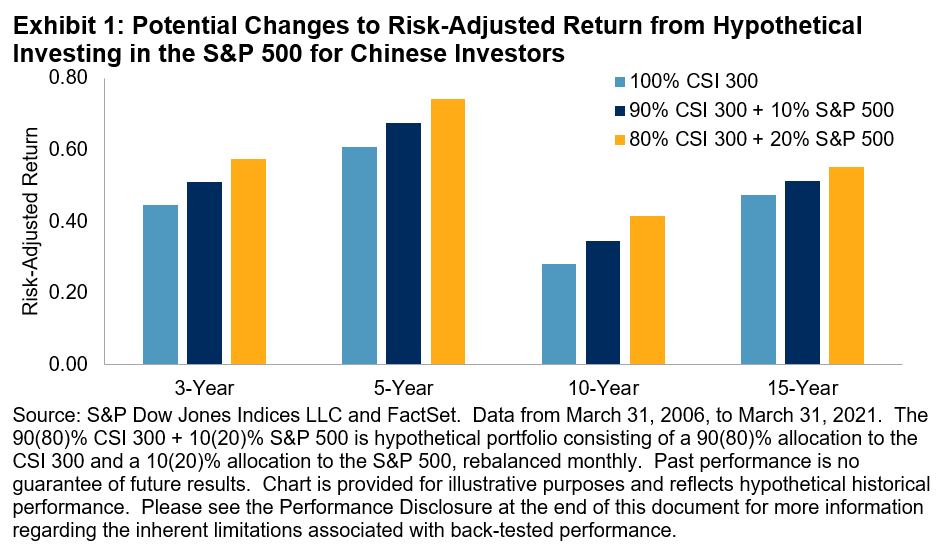

- Highlight how the S&P 500 could affect Chinese investors’ ability to diversify domestic sector biases, gain exposure to U.S. economic growth, and improve historical risk-adjusted returns; and

- List different channels where Chinese investors may access global markets and review the Qualified Domestic Institutional Investor (QDII) program.