Executive Summary

A healthy trading ecosystem promotes price transparency, market efficiency and confidence for market participants operating at all frequencies, from highly active tactical traders to buy-and-hold passive investors. Updating our analysis from 2023, this paper surveys the volumes for listed products tied to the indices produced by S&P Dow Jones Indices (S&P DJI). Spanning asset classes and product types, the results offer insight into the increased presence of index-linked products within global capital markets.

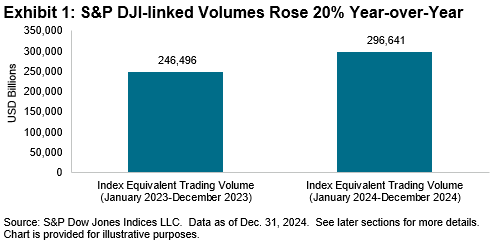

- The economic value of volumes across products tied to S&P DJI’s indices increased by USD 50 trillion in 2024.

- The usage of index-linked products is increasingly active, with the median holding period across S&P DJI products falling from 222 to 198 days.

- We spotlight the importance of sector and industry products to express market views and note the growing use of exchange-traded futures tied to these indices.

Why Track Trading?

Index funds, which hardly existed 50 years ago, now play a prominent role in global financial markets. The growth in passive investing has coincided with increased availability and usage of tradeable (that is, listed) index-based products, and their combined growth may create benefits for both active and passive users.

One of these benefits is expanded mechanisms facilitating price discovery. For example, there are now listed products tracking the S&P 500®—including futures and exchange-traded funds (ETFs) listed across the world—that in combination trade almost 24 hours a day. Consequently, investors no longer have to wait until the underlying equity exchanges are open to assess the impact of overnight events, a fact confirmed by the observation that U.S. equity markets typically open at prices that are in line with where their futures were just recently trading.

Another benefit is improved market efficiency. For example, the quoted prices of an ETF tracking The 500™ may be supported by the large and liquid trading ecosystem tied to the same index, which allows arbitrageurs and market makers to minimize mispricing by combining trades in one product with trades in another, often including derivatives such as futures and options tied to the same index.

Meanwhile, motivated by the ability to exploit any discrepancies, highly active users of index-based products add transparency by scrutinizing every index change in price, composition or methodology.

All of this may help market participants maintain confidence that indices such as the S&P 500 will faithfully replicate their target market and that licensed products will track the index closely.

Thus, as well as indicating the presence of higher-frequency market participants, volume data gives us an indication of the potential network effects arising from greater liquidity: a market that is better “policed” by arbitrageurs is potentially one with stronger links reinforced between an index and its objective, and between index-linked products and the indices they seek to track.