EXECUTIVE SUMMARY

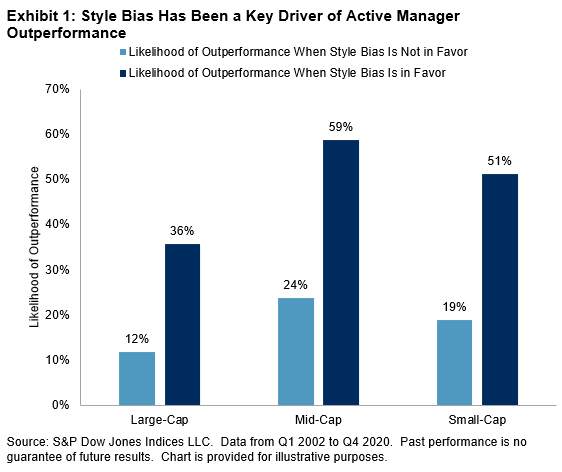

- Style bias plays a major role in explaining active manager outperformance across the capitalization spectrum.

- Active managers of large-capitalization portfolios tend to tilt down the cap scale, while mid- and small-cap managers tend to tilt up. Consequently, large-cap managers are most challenged when large-cap stocks beat mid- and small-caps. Mid- and small-cap managers have the opposite tendency.

- As Exhibit 1 illustrates, the likelihood that a majority of managers in a given capitalization tranche will outperform is importantly dependent on style favorability.

- Similar results apply for fixed income managers.

A SIMPLE QUESTION

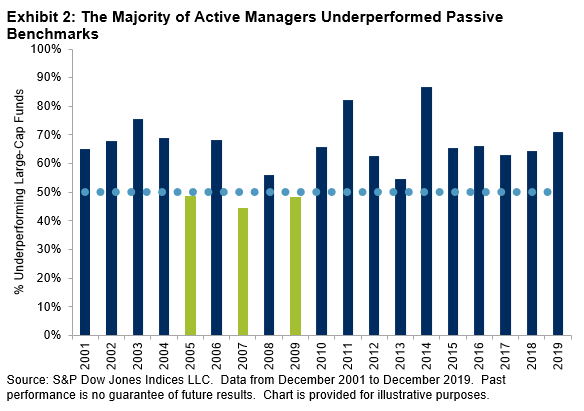

The evidence that most active portfolio managers typically underperform passive benchmarks appropriate to their investment style is extensive—both historically and geographically. Exhibit 2, for example, summarizes data from our firm’s SPIVA® Scorecards, which have documented the performance of U.S. managers since 2001 (with shorter histories for other markets). Of the 19 full calendar years for which we have U.S. SPIVA results, the majority of large-cap active managers outperformed the S&P 500® in only three.

This paper asks a simple question: what (if anything) distinguishes the three years when most active managers outperformed from the 16 years when the majority failed?