EXECUTIVE SUMMARY

- Any analysis of investment policy or strategy must be based on historical data. Even if an analyst wants to extrapolate into the future (which we do not), extrapolations must start with the past.

- But the historical data that we observe were not inevitable; history might have turned out differently than it actually did.

- In this paper, we construct a counterfactual history of the last 40 years of U.S. equity returns, and explore what those histories could imply for investment policy.

- Although the range of possible outcomes is quite wide, one consistent conclusion is that long-term investors in large-capitalization U.S. equities would have been advantaged by choosing passive rather than active management.

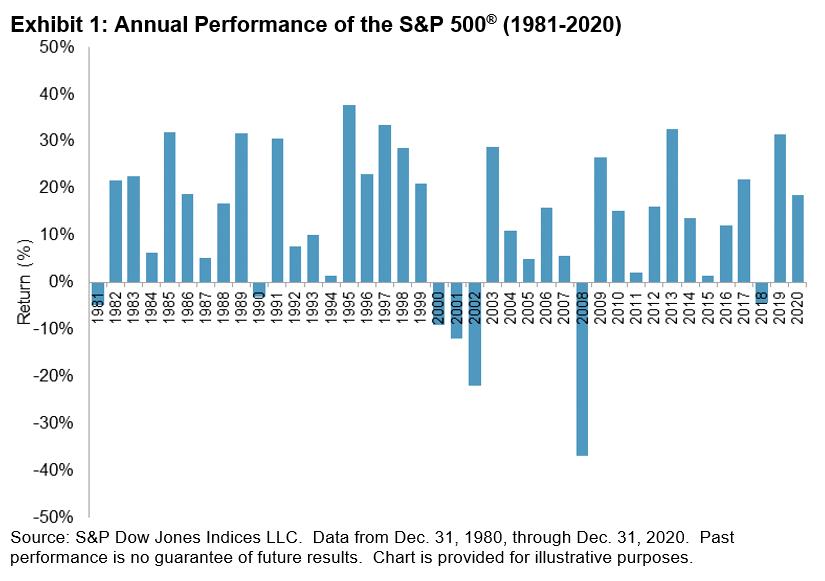

INTRODUCTION

We often write about equity markets and the potential implications of various investment strategy choices. What are the implications of the choice between active and passive management? How have factor or “smart beta” strategies performed in various economic environments? What do market dynamics tell us about the investment opportunity set?

All of these questions, and others like them, are important, but all are questions about returns. Investors, however, live not with a series of returns, but rather with portfolio values. In this paper, we model the connection between returns and portfolio values over a long-term historical horizon.