EXECUTIVE SUMMARY

With increasing interest in smart beta strategies in the Australian equity market, we examined the effectiveness of six well-known risk factors, size, value, low volatility, momentum, quality, and dividends, in the Australian equity market from Dec. 31, 2004, to May 29, 2020.

- Quintile analysis showed that low volatility, high momentum, and high quality delivered the most persistent absolute and risk-adjusted return spreads, but small cap and value did not generate incremental return in the Australian market.

- Among the Australian factor indices offered by S&P Dow Jones Indices (S&P DJI), the quality and momentum indices delivered the highest excess returns, while the low volatility and dividend indices had lower volatility than the S&P/ASX 200.

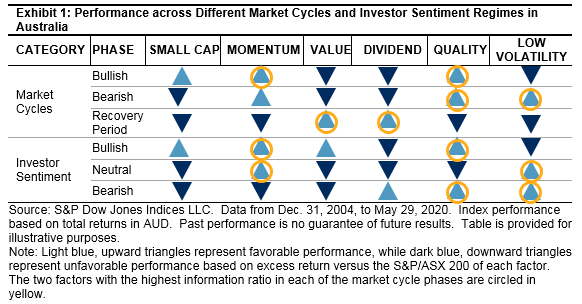

- Our macro regime analysis showed that most factor portfolios in Australia were sensitive to local market cycles and investor sentiment regimes.

- The distinct cyclicality of factor performance in Australia indicated its potential for implementation of active views on the local equity market.

FACTOR-BASED INVESTING IN THE AUSTRALIAN EQUITY MARKET

Smart beta strategies have gained significant attention in the asset management industry, and the exchange-traded products (ETPs) tracking factor indices have experienced significant asset growth since the end of 2008. Factor-based strategies are a category of smart beta strategies that target specific risk factors. They share some common characteristics with passive investing, such as rules-based construction, transparency, and cost-efficiency, and they also share features of active investing in that they aim to enhance return and reduce risk compared to market-cap-weighted indices.

Single-factor indices are constructed explicitly to capture a specific risk factor and exhibit distinct cyclicality in response to a changing market environment, which also makes them ideal tools for implementation of active views.

In Australia, although the adoption of factor-based investing by local market participants is behind the U.S. and some Asian markets (like Japan), the growth of factor-based ETPs has accelerated in recent years, achieving 46% growth in net assets in the past 18 months in local currency terms as of Dec. 31, 2018, and accounting for 10.5% of the Australian ETF market. Dividend products still dominate the Australian factor-based ETP market, but we observed the proliferation in categories and the increasing demand for factor-based index-linked products within the Australian equity market.

Based on the performance contribution analysis for the S&P/ASX 200 portfolio, the Financials and Materials sectors contributed about 63.6% of the total performance of the portfolio for more than 15 years. At a stock level, the top five large-cap contributors (BHP Group Ltd, Commonwealth Bank of Australia, Westpac Banking Corporation, CSL Limited, and Australia and New Zealand Banking Group Limited) together contributed approximately 49% of the total portfolio performance over the same period. This suggests that sector or size bias might have a significant impact on the excess return of factor portfolios in the Australian market.

In this paper, we examined the effectiveness of six well-known risk factors (size, value, low volatility, momentum, quality, and dividend) in the Australian equity market and the behavior of these factors under different market regimes.