EXECUTIVE SUMMARY

- Green bonds have historically exhibited a green premium—or "greenium"—meaning they have lower yields compared to non-green bonds with otherwise similar characteristics.

- Rapid growth and increasing differentiation within the green bond market has led to better ways to measure greenium across global bond markets.

- An index-based approach illustrates the level of greenium across bond markets; comparing current levels to historical ones suggests shrinking greenium in many major markets.

INTRODUCTION

Green bonds are tied to specific environmentally friendly projects of an issuer. The borrower agrees that the use of proceeds will be invested in environmentally friendly projects such as alternative clean energy, low carbon assets (e.g., green buildings, factories, or vehicles), or sustainable usage of water, pollution, or natural resources. In exchange for this commitment, the issuer seeks economic benefit in the form of a lower borrowing cost. First tapped by supranational borrowers such as the European Investment Bank and the World Bank, the index market value of green bonds surpassed USD 1 trillion in September 2021, expanding from sovereign and quasi-sovereign bonds to corporate and securitized debt.

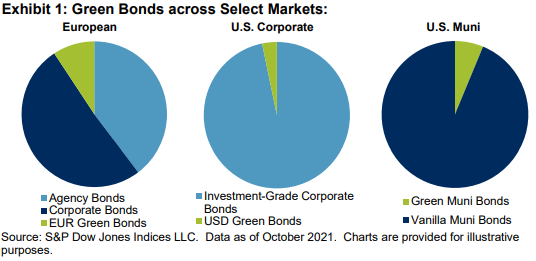

The green bond market, as measured by the S&P Green Bond Index, has grown since its 2007 debut: growth in the market value of green bonds averaged 70% annually over the past decade, compared with 3% for the global bond market (see Exhibit 1). Along with surging growth, investor demand for green bonds has remained strong.

S&P Global Ratings' research on the European credit market observed initial sustainable bond yields to be lower compared with conventional bonds, incentivizing issuers. Despite a lower yield, or greenium, investors absorbed the liquidity of green bonds, further stimulating supply. In cases of no greenium at issuance, the research highlighted economic incentives for the investor in the form of outperformance. Tracking historical performance of two nearly identical German government bunds demonstrated additional spread tightening of 5 bps of the bund that was classified as green in the year since issuance.

Historical pricing appeared to demonstrate a price premium for green over non-green, or vanilla, bonds, as green debt represents just 2% of the overall market. More recent evidence suggests mutual benefits for investors and issuers alike as green and vanilla bond yields converge over time. This paper analyzes factors contributing to the changing relative valuation between green and vanilla bonds. Markets covered include European government agency and corporate bonds, as well as U.S. corporate and municipal markets.

Many issuers have repeatedly tapped the green bond market, allowing for issuer-based credit curves. In select cases, they provide good comparisons, but this is rare. Often, new green bonds cannibalize matured vanilla bonds, creating new issue bias. Applying a comprehensive credit valuation approach, this paper analyzes green and vanilla bonds by issuer, sector, and credit rating.