Introduction

When considering investing in commodities, synthetic access is a popular choice. Commodity futures offer exposure to commodities performance attributes without the need for delivery and storage, and commodity indices offer broad measures of multiple commodity sectors without the need for detailed knowledge of individual commodity markets. Popular broad commodity indices hold the nearest expiring futures contract with a mechanism to roll out of the futures contract before expiring into the next nearest expiring futures contract.

This roll mechanism introduces a second type of return to commodity investors known as roll yield. Therefore, investing in commodities synthetically exposes the investor to both (1) the return of the underlying commodity, and (2) the roll yield from the rolling mechanism.

A popular and simple carry strategy involves holding commodity futures further along the curve, for example, three months forward. To be clear, being three months forward is a constant maturity strategy, whereby the commodity index always aims to hold futures contracts that expire roughly three months in the future. Practically speaking, this means the contract calendar for a given (prompt month) index is shifted by three units.

This paper will explore the characteristics of indexing at the three-month tenor, using the broad-based commodity index the Dow Jones Commodity Index (DJCI) and its variant the Dow Jones Commodity Index 3 Month Forward (DJCI 3M) as an example.

A Comparison of DJCI and DJCI 3M on a Spot and Excess Return Basis

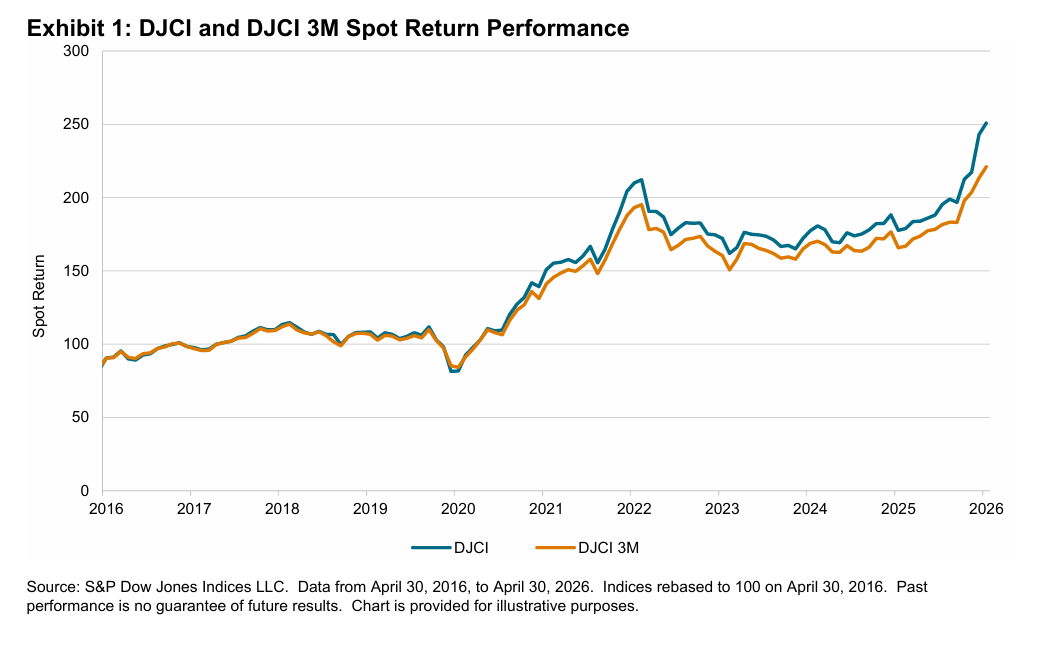

To begin, we will compare the performance of the DJCI and the DJCI 3M on a spot and on an excess return basis. As a reminder, the spot version of the indices is simply the weighted average price of the constituent contracts, whereas the excess return version of the indices accounts for (1) the daily price return of those contracts, and (2) the roll yield received from rolling those contracts.

It is important to note that the contracts must be rolled for a long only strategy to prevent physical delivery, and therefore the excess return index is the only strategy that is replicable.

Exhibits 1 and 2 show the DJCI versus the DJCI 3M on a spot and on an excess return basis, respectively. While the DJCI outperformed the DJCI 3M on a spot return basis, the DJCI 3M outperformed the DJCI on an excess return basis.