EXECUTIVE SUMMARY

- Net-zero commitments are starting to receive signatories, with USD 5.7 trillion and USD 37 trillion assets signed up to the Net Zero Asset Owners Alliance and Net Zero Asset Managers initiative, respectively.

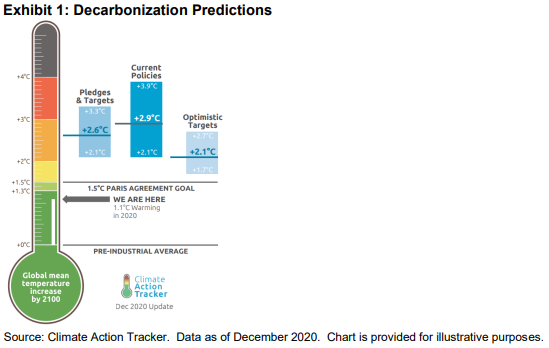

- Even optimistic targets show the world falling short of a 1.5°C scenario (see Exhibit 1). Scientific consensus suggests a 1.5°C pathway would require net-zero emissions by 2050, while 2°C pathways are closer to 2070-2080.

- Absolute greenhouse gas (GHG) reduction (tracking a specified scenario) is aligned with meeting these goals, while relative GHG reduction (reduction to an underlying index) is better but not necessarily aligned.

- The S&P PACT™ Indices (S&P Paris-Aligned & Climate Transition Indices) are designed to give investors confidence in following absolute decarbonization pathways.

WHERE ARE WE NOW?

Both the Net Zero Asset Owners Alliance and Net Zero Asset Managers initiative have signed up to target net-zero GHG emissions by 2050 or sooner, binding trillions of dollars to be decarbonized. This raises the question, how can we grasp these climate targets and practically implement them?

Understanding scenario alignment as reductions in GHG emissions (or GHG intensity adjusted for inflation) at the portfolio level, aligned with that required of the global economy, allows the application of conclusions from climate scenario trajectories to broad-market indices. The EU Technical Expert Group on Sustainable Finance (TEG) promotes this philosophy as not simply limited to indices, but applicable to asset owners, asset managers, private investors, etc. as a method to decarbonize a portfolio.

We use data from the Integrated Assessment Modeling Consortium's (IAMC's) 1.5°C Scenario Explorer, used in the Intergovernmental Panel on Climate Change's (IPCC's) Special Report on Global Warming of 1.5°C, which is a collection of quantitative climate scenario pathways. These enable us to approximate scientific consensus on future climate scenarios. The next sections will discuss relationships among these climate scenario predictions.

Modeling future climate scenarios is tough, even for the world's brightest minds, due to the climatic system being complex in nature. This brings significant potential for error and uncertainty. Therefore, aiming below predicted trajectories may be prudent to increase confidence in a stable climate.

WHERE ARE WE HEADING?

While there is uncertainty around the climate scenario we are heading for, Carbon Action Tracker calculates scenario predictions based on current policies, current pledges and targets being met, and more optimistic targets, where any targets agreed on or under discussion are assumed to be achieved.

Even optimistic targets only predict a median temperature increase of 2.1°C above pre-industrial levels by the year 2100 (see Exhibit 1). Even the lower bound of optimistic targets see us fall short of the 1.5°C target the IPCC steers us toward.

The median expected 2100 warming is around 2.6°C when accounting only for those that have made pledges, while current policies would leave us around 2.9°C, but potentially as high as 3.9°C—a high degree of error built in, given we are currently at 1.1°C above pre-industrial levels.