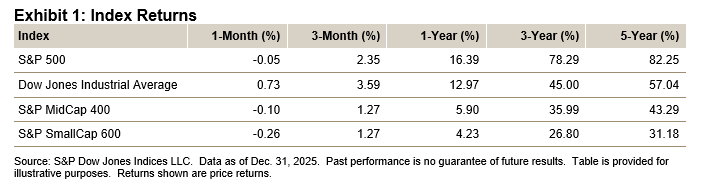

Key Highlights

- The S&P 500® was down 0.05% in December, bringing its 2025 performance to 16.39%.

- The Dow Jones Industrial Average® gained 0.73% for the month and was up 12.97% for 2025.

- The S&P MidCap 400® decreased 0.10% for the month, bringing its 2025 level to 5.90%.

- The S&P SmallCap 600® fell 0.26% in December and was up 4.23% for 2025.

Market Snapshot

In December, the S&P 500 continued November’s reallocation, as most of the money stayed in the equity markets (some also went into gold and silver, but not oil), with domestic and international inflows continuing to be strong (though U.S. interest rates remained on the high side, with the dollar on the low side—not unassociated). The month ended in a minor 0.05% decline (up 0.06% with dividends), after November’s 0.13% gain and the prior 10 months’ 16.30% (7 months up and 3 down), leaving 2025 with a pleasing 16.39% gain (but it was the second year of declines, as 2024 was up 23.31% and 2023 was up 24.23%). The three-year total return was 88.11% (23.01% annualized), but the more pressing question is about 2026: the S&P 500 one-year bottom-up consensus target price for the S&P 500 is 8,001, a 16.9% expected gain, marking a potential fourth year of double-digit gains (last seen in a five-year run from 1995 to 1999 of 220%). Breaking down the gains shows the often-quoted Magnificent 7 contributing a sizable amount. For the three-year period, the Magnificent 7 contributed 55% of the total return, meaning the 86% (23.0% annualized) total return would become 39% (11.6% annualized) without the group, while 2025’s 17.9% would become 10.4%, with the expected 2026 return of 16.9% (a potential third year of decreasing gains) becoming 9.3%. Of note, however, is that the top-heavy stocks are projected to become even more so, as NVIDIA (NVDA) and Microsoft (MSFT), which together comprise 14% of the index’s market value, are expected to contribute 30% of the return, so 16.9% would be 11.8% absent those two. In retrospect, while no one created an aggravation-reward index, 2025 was not an easy year (but it was profitable for most); the people who think 2026 will be easier are those who have taken their profits and parked their money in more secure instruments.

As for 2025, the S&P 500 posted a 16.39% gain (17.88% with dividends), compared to 2024’s 23.31% (25.02%), 2023’s 24.23% (26.29%) and 2022’s decline of 19.44% (-18.11%). Breadth slightly declined for the year, as 304 issues gained (332 in 2024, 332 in 2023) and 196 declined (169, 179). Ten of the 11 sectors gained for the year (Communication Services had the best performance, up 32.41%, and Real Estate the worst, down 0.35%); 2024 also saw 10 of 11 sectors gain (Communication Services at 38.89%, and Materials at -1.83%), while 2023 had 8 of 11 (Communication Services at 54.36%, and Utilities at -10.20%). Of note, 2022 was not a good year, as the index fell 19.44%, with only one sector up (Energy, 59.05%) and 10 down (Communication Services, -40.42%), as 139 issues were up and 363 were down. Risk, as measured by VIX, closed down at 15.01 from 17.35 at year-end 2024, but in between it spiked on April 7 at 60.13 over tariffs, and it reached its yearly lows in December. Intraday daily volatility (high/low) increased for 2025 to 1.18% from 2024’s 0.91% and 2023’s 1.04% (historically 1.40%). Trading volatility for the year increased 31% over 2024; it declined 2% in 2024 and fell 1% in 2023. On an aggregate basis, the S&P 500 closed with a market value of USD 58.438 trillion, adding USD 8.633 trillion for the year into shareholders’ pockets (excluding USD 671 billion in dividends) and adding USD 26.305 trillion (plus USD 1.888 trillion in dividends) over the three-year period.

From a higher market view, the recent reallocation was seen as a successful market operation, as money not only stayed in the market, but inflows helped to support levels. On an issue level, breadth declined and turned negative (242 up and 260 down), reflecting the continued top-heavy contributions, as the Magnificent 7 continued to outperform (the 0.06% S&P 500 total return gain for December would have been a decline of 0.18% without the Magnificent 7). Leadership shifted, as views of the economy (the expectation of Fed interest rate changes, employment, consumer spending and earnings) and politics (tariff negotiations and alternatives to an expected Supreme Court ruling) changed, while trading remained calm. December trading volume was down 13% from November (but up 12% year-over-year), though 2025 was up 31% over 2024 (after 2024 was down 2% over 2023).