Overview

In 2025, Asia-Pacific economies remained resilient, delivering stronger-than-expected growth despite persistent geopolitical tensions and tariff headwinds. Throughout the year, central banks in the region remained highly vigilant, closely monitoring a broad spectrum of economic indicators to ensure their policy decisions were both timely and effective.

Many responded to signs of economic weakness with stimulative rate cuts, while others paused as inflationary pressures resurfaced. Most Asia-Pacific markets experienced at least two rate cuts, whereas the Bank of Japan took a divergent path, implementing two rate hikes and pushing interest rates to levels not seen in 30 years to curb inflation.

Over the past five years, Asia-Pacific bond markets have broadened and deepened, shaped by evolving currency dynamics, shifting interest rates and changing economic conditions. Both issuers and investors have become increasingly strategic, carefully balancing currency, duration, credit quality and carry considerations to navigate the region’s dynamic and complex environment.

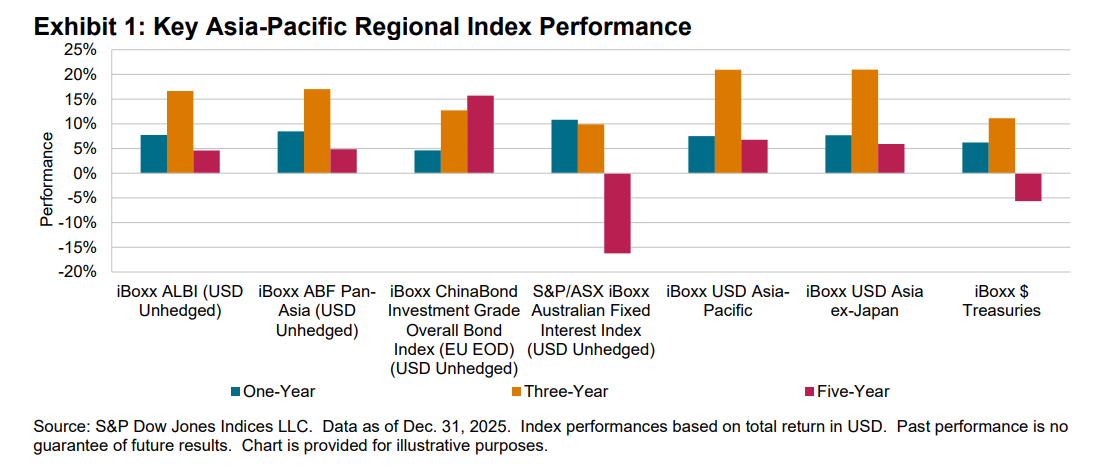

Among local currency multi-market indices, the iBoxx ABF Pan-Asia (which consists of government and quasi-sovereign bonds) outperformed iBoxx ALBI (which consists of additional government bonds such as India and offshore RMB, as well as corporate bonds from select markets from one-, three- and five-year timeframes). Over a five-year period, in USD unhedged terms, the iBoxx ChinaBond Investment Grade Overall Index and S&P/ASX iBoxx Australian Fixed Interest Index exhibited contrasting performance patterns: CNY bonds gained 15.71%, while AUD bonds lost 16.22%. However, as the Australian dollar rebounded against the U.S. dollar in 2025, AUD bonds (in USD unhedged terms) posted double-digit gains (10.82%) compared to CNY’s 4.63%.

For USD-denominated bond indices, the iBoxx USD Asia-Pacific Index outperformed the iBoxx USD Asia ex-Japan Index across one-, three- and five-year periods. This outperformance was driven by the eligibility of USD-denominated bonds from Japan, Australia and New Zealand, which diluted the weight of China and thereby mitigated the impact of the China real estate crisis. Notably, the past five years also saw a contraction in the iBoxx USD Asia ex-Japan universe—from more than USD 1.4 trillion at its peak in 2021 before the property crisis to USD 0.99 trillion as of year-end 2025—as more Asian issuers diversified their funding sources by issuing in other currencies (such as offshore RMB). The iBoxx USD Asia-Pacific Index, on the other hand, ended the year at USD 1.6 trillion in notional value.