In the world of ESG investing, there has long existed a David versus Goliath scenario in which smalland mid-cap companies have often been considered the sustainable underdog. With the strength, size, and resources of larger-cap companies, it may seem a formidable challenge for smaller companies to compete within the sustainable ranks. However, the rules around corporate sustainability are evolving, and nimbleness, flexibility, and adaptability are all attributes that will ultimately help promote positive change in mid- and small-cap companies. The 2021 rebalance—the first for the S&P MidCap 400® ESG Index and the S&P SmallCap 600® ESG Index since their launch—has provided an opportunity for these small(er), yet mighty, companies to showcase their contributions to the growing sustainability universe.

ESG Score Improvement: A Leading Indicator

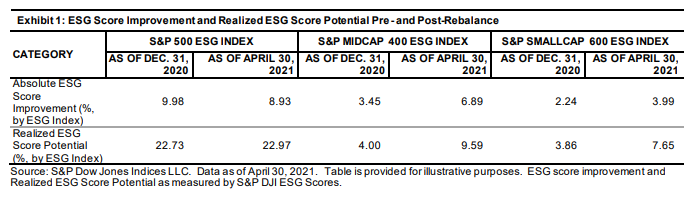

While there were many positive results coming out of the April 30, 2021, rebalance, one of the most encouraging signals was that small and mid caps are well on their way to improving their sustainability standing. This was evidenced by the fact that the S&P SmallCap 600 ESG Index and S&P MidCap 400 ESG Index achieved a significant boost in S&P DJI ESG Score improvement both in absolute terms—at the index level—and in their realized ESG score potential. While the numbers may seem modest in comparison to their large-cap counterpart, the substantial year-over-year increase in ESG performance for both the small- and mid-cap indices dwarfed the improvements exhibited by the S&P 500® ESG Index (see Exhibit 1). This could be considered an indicator that smaller companies are moving quickly to close the sustainability gap between themselves and their larger-cap competitors.