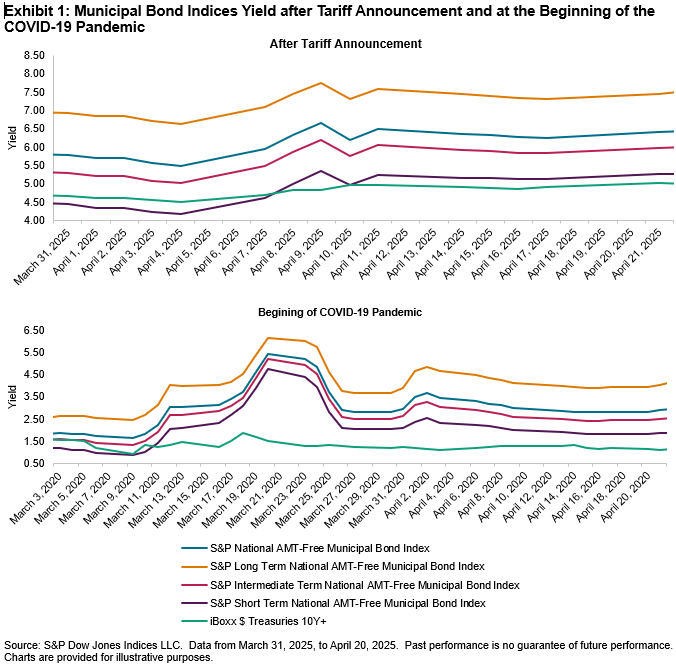

The beginning of the year has been challenging for municipal bonds, as a combination of factors rattled the U.S. markets. Market volatility, largely driven by the announcement of tariffs on April 2, 2025, created an uncertain environment that extended to the municipal bond sector. Adding to the uncertainty was the looming expiration of a Congressional bill (The Tax Cuts and Jobs Act [TCJA] of 2017) that upheld the tax-exempt status of municipal bonds, set to expire at the end of 2025. Fortunately, the new tax reform bill passed the House of Representatives in May 2025, and the tax-exempt status of municipal bonds remained intact for the time being, with another assessment remaining in the Senate. This potential shift in the regulatory framework has further compounded market anxiety, as the tax-exempt status is a significant draw for many municipal bond investors. Additionally, municipal bond issuance experienced a slowdown in Q1 2025, from USD 125.6 billion in Q4 2024 to USD 119.1 billion in Q1 2025, a 5.1% decrease. 1

Overall taxable equivalent yield (TEY) for the S&P National AMT-Free Municipal Bond Index surged from 5.69% on April 1 to 6.36% on April 14, 2025—a dramatic 66 bps increase not seen since the early days of the COVID-19 pandemic. By the end of April 2025, yields for the index had stabilized at 6.06%, but since then, the TEY has remained above 6%. The S&P Intermediate Term National AMT-Free Municipal Bond Index and the S&P Long Term National AMT-Free Municipal Bond Index also experienced significant yield jumps of 70 bps and 59 bps, respectively. In contrast, the S&P Short Term National AMT-Free Municipal Bond Index saw a yield drop of 3 bps, reflecting the market's preference for shorter durations during times of volatility.

A comparison of index returns for the first five months of 2025 versus 2024 reveals a notable underperformance of the S&P Long Term National AMT-Free Municipal Bond Index, signaling a risk-off market sentiment and the search for shorter-dated bonds. In March 2025, the index was down 2.60%, with a modest recovery to -1.39% in May 2025. When compared with May 2024, the index was 168 bps lower in May 2025, highlighting the cautious approach adopted by market participants.