August 2022 Commentary

The recent rally in U.S. equities hit a reset after hawkish comments by the Federal Reserve Chairman Jerome Powell at the Jackson Hole Economic Symposium.

In his speech to investors, Powell indicated that the Fed is committed to raising rates to quell inflation and to bring demand and supply dynamics in better balance. His remarks sparked a sell-off in U.S. stocks and pushed bond yields and the U.S. dollar higher.

For the month of August, the 2-year U.S. Treasury yields rose from 2.90% to 3.45%, while the 10-year U.S. Treasury yields were up 48 bps to 3.15%. Meanwhile, the U.S. dollar came close to a 20-year high against other major currencies.

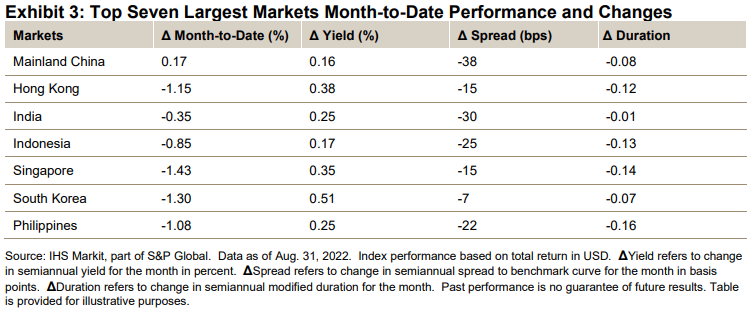

With U.S. yields rising across the curve in August, the rally of Asian USD bonds in July was short-lived. This month, the iBoxx USD Asia ex-Japan Index fell 0.40%, largely driven by the negative performance of its investment-grade bonds. The overall index yield rose 24 bps to 5.82%, and the overall index spread narrowed 26 bps to 244 bps.

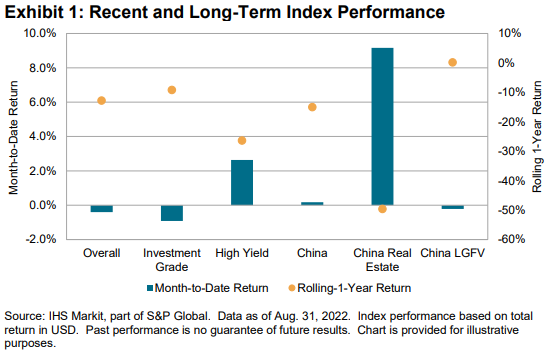

Making up about 85% of the overall index by market value, the investment grade (IG) subindex considerably underperformed the high yield (HY) subindex this month. In the IG segment, losses were seen in the mid-to long-end of the curve. In contrast, the HY subindex generally logged gains across the maturity buckets. Moreover, the HY subindex yield and spread dropped by 75 bps and 137 bps, respectively.