Overview

In 2025, the iBoxx USD Emerging Markets Broad Overall Index rose 10.31%, the strongest annual performance in the past six years, with a primary driver being the structural weakness of the U.S. dollar. In 2025, the S&P U.S. Dollar Futures Index was down 5%, following three 25 bps rate cuts by the U.S. Federal Reserve, which lowered the federal funds target range from 4.25%-4.50% at the end of 2024 to 3.50%-3.75% by December 2025. U.S. core inflation also eased, finally settling below 3%, though it remained above the Fed’s 2% target. Despite episodic rebounds during risk-off periods, the sustained U.S. dollar weakness was broadly supportive for emerging market (EM) fixed income, easing external financing conditions and improving investor appetite for higher-yielding EM debt.

Outside the U.S., macro conditions evolved unevenly. In Europe, after an initial 25 bps rate cut in June 2025, the European Central Bank held policy rates unchanged through the remainder of the year as inflation remained near target and policymakers emphasized a data-dependent approach. Across emerging markets, monetary policy paths have diverged. In Brazil, the central bank maintained a restrictive stance by holding the Selic benchmark rate at 15.00%, its highest level in nearly 20 years. In Mexico, the central bank continued its easing cycle, bringing the policy rate to 7.00% by December 2025. In South Africa, the central bank also resumed cautious easing with a 25 bps cut to 6.75% in November following a pause in September.

In China, subdued domestic demand and the continued adjustment away from property-led growth kept inflation pressures low and policy accommodative. In the Middle East, countries such as Saudi Arabia and the UAE largely adjusted policy rates in line with U.S. monetary policy, reflecting currency pegs to the U.S. dollar.

Broadly speaking, EM Eurobond issuance reached a record high in 2025, with EM sovereign bond issuance reaching USD 255.7 billion by early December. The strong issuance backdrop was underpinned by a weaker U.S. dollar and continued policy easing by some major central banks. In public markets, risk sentiment was further supported by strong U.S. equity performance, with the S&P 500® gaining 16.4% in 2025.

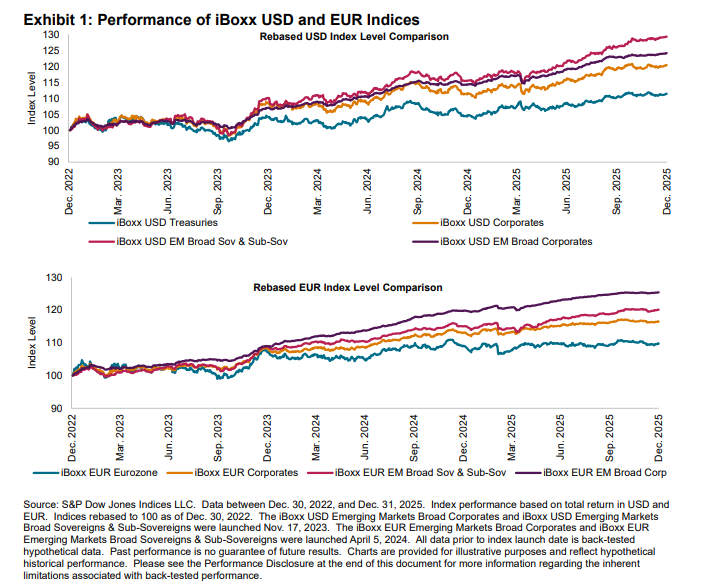

Overall Index Performance