Daily Index Insights offers a concise two-minute read on the latest news and trends in index markets. This resource includes performance data from S&P Dow Jones Indices across equities, fixed income, multi-asset, commodities, and factors. Our daily insights are designed to provide you with a comprehensive understanding of market movements, empowering you to make informed decisions based on the most current indices data and analysis.

“The secret of staying young is to live honestly, eat slowly, and lie about your age.”

Lucille Ball (August 6, 1911 – April 26, 1989)

A hundred years ago today, American swimmer Gertrude Ederle became the first woman to swim the English Channel. She didn't just finish the grueling route from France to England; she beat the existing men's record by nearly two hours, clocking in at 14 hours and 31 minutes. Setting new benchmarks usually requires navigating some choppy waters, something markets know well right now. Here is your Daily Dashboard.

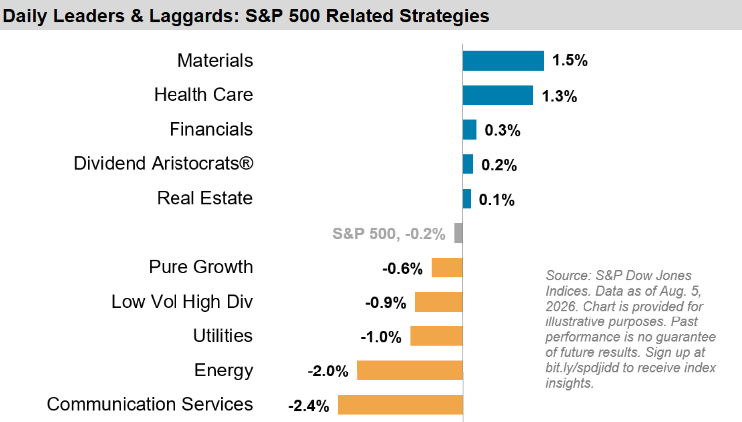

- The S&P 500® declined 0.2% yesterday. The broader market was weighed down by losses in Communication Services (-2.4%), Energy (-2.0%), and Utilities (-1.0%), which offset gains in Materials (+1.5%), Health Care (+1.3%), and Financials (+0.3%).

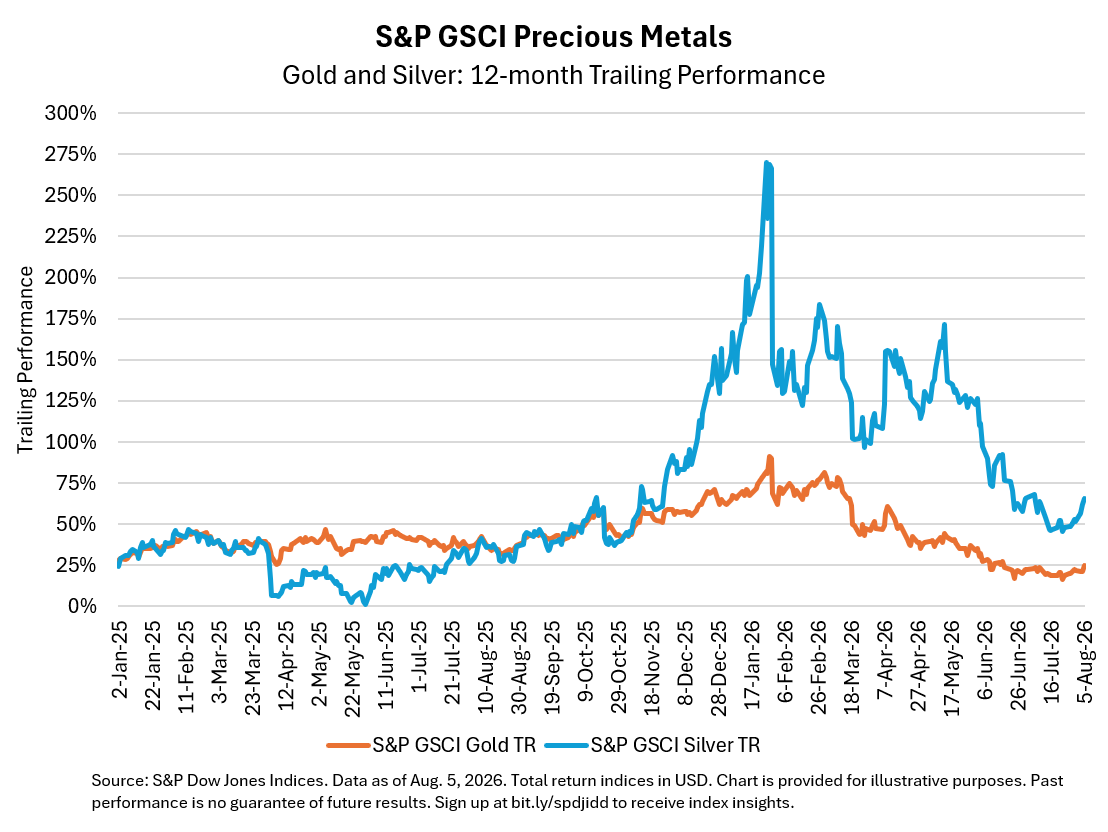

- Precious metals have rallied month-to-date, led by Silver (+7.9%) and followed by Gold (+4.9%). Following recent monthly declines, Gold appears to be regaining its safe-haven appeal amid lingering concerns over U.S. inflation.

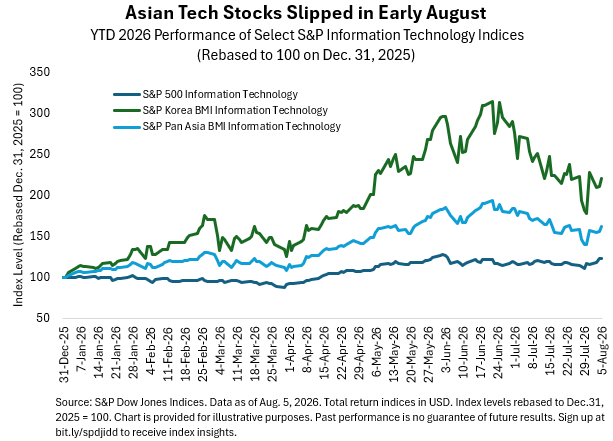

- Asian Information Technology stocks, measured by the S&P Pan Asia BMI Information Technology, retreated in August following a steep decline on the first trading day of the month. This contrasts with U.S. Tech, which experienced a mild increase. The drawdown in Asia happened at the same time as notable weakness in the Korean Tech sector, as major constituents like SK Hynix Inc. reported earnings that fell short of consensus estimates.

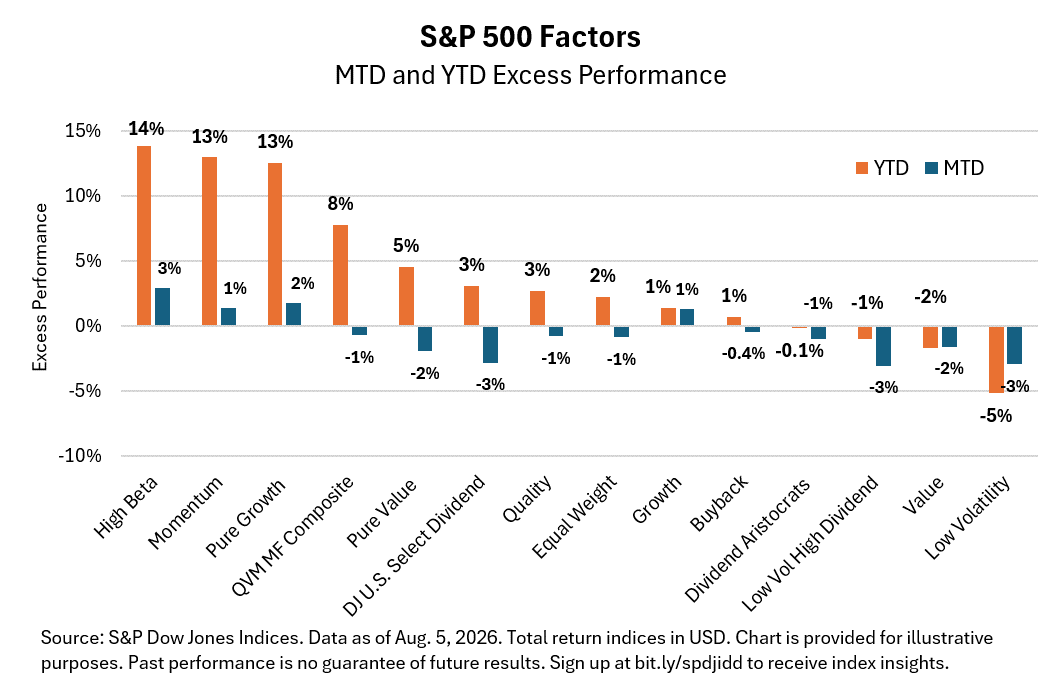

- As seen on page 4 of the Dashboard, August has been a good month for U.S. factors, with all of them in positive territory. But how many of them provided excess performance over the benchmark in the last year? Note that every factor, with the exception of the S&P 500® Dividend Aristocrats®, recorded negative daily performance yesterday.