2025: Year In Review

The year 2025 ended with a positive quarter for financial markets. Following a hesitant start to Q4, with AI-related stocks coming under pressure due to valuation concerns, equity markets rallied strongly into year-end with the S&P World Index finishing 2025 just shy of all-time highs.

For 2025 as a whole, markets performed significantly well, supported by favorable monetary conditions combined with strong corporate earnings announcements. Returns for most private client investors are expected to have been well ahead of the long-term averages for the third year in a row.

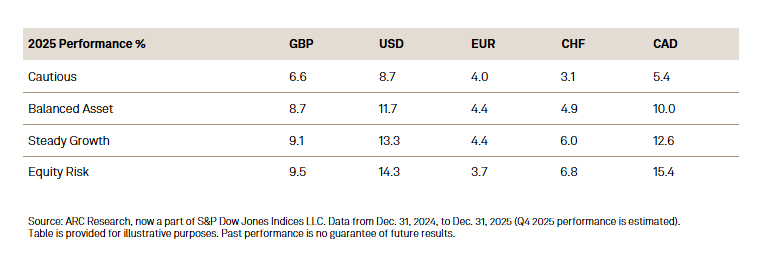

The table below sets out the estimated returns for private client portfolios across the five ARC Private Client Indices (PCIs) and four PCI risk categories.

There were significant currency moves over the course of the year, and these moves explain much of the difference in performance between the various indices. The U.S. dollar was weak, especially in the first half of the year as markets digested the implications of President Trump’s trade policies. The U.S. Dollar Index (DXY) ended the year 9.4% lower. The Canadian dollar also came under pressure, while the Swiss franc and the euro were the main beneficiaries of the U.S. dollar’s weakness, rising 14.4% and 13.4%, respectively.

Within fixed income markets, U.S. and U.K. government bond yields fell and the curves steepened as further rate cuts were priced in. Turning to Europe, German yields edged higher while the best performance was found in the peripheral markets of Spain, Italy and Greece, all of which saw their spreads over German Bunds narrow significantly. Credit risk was rewarded, with investment grade, high yield and emerging market spreads tightening.

Gold had another exceptional year, up 62% in U.S. dollar terms, taking the rally from the 2022 lows to over 150%. Bitcoin once again grabbed much of the headlines but ended the year 6% lower at around USD 88,000—well below the highs of USD 125,000 seen just three months prior.

For the third successive year, equity investors enjoyed strong performance, with the S&P World Index increasing 13.6% in GBP terms (total return). This follows a 21.6% rise in 2024 and 17.5% gain in 2023.

In contrast to 2023 and 2024, gains were reasonably widespread. In the previous two years, the bulk of the global stock market performance was driven by a small number of U.S. mega-cap growth stocks. During this period, global growth materially outperformed global value (as measured by the S&P World Growth Index and S&P World Value Index, respectively) and U.S. equities outperformed the rest of the world (as measured by the S&P United States BMI and S&P Global Ex-U.S. BMI, respectively). In 2025, these trends reversed, and while the Magnificent 7 as a group once again delivered strong absolute returns, there were opportunities for discretionary fund managers to add value at the country and sector level without the need to have material exposure to these seven names.