01 Mar 2016 | 10:31 UTC — Insight Blog

Ethylene projects in the ethane-heavy Northeast US

By Ben Gonzalez and Prachi Mehta

The US has experienced a renaissance in petrochemicals due to the abundance of ethane from shale gas. As a result of the increasing NGL production from various shale plays, there have been a total of 17 announced greenfield steam crackers in the US. Since much of the NGL production boom has come from the Northeast US, we wanted to take a look at ethane cracker projects in that area and assess their progress.

Ethane supply from the Marcellus and Utica Shale has grown strongly in the last few years but regional demand and pipeline takeaway capacity is still limited. US ethane supply from gas plants (before rejection) in the Marcellus and Utica has grown from 5,000 b/d in 2013 to about 276,000 b/d in 2015, according to Platts Bentek. Ethane production is estimated to grow to 387,000 b/d in 2017 and 443,000 b/d in 2018, according to Platts Bentek Market Call: North American NGLs, 1Q 2016.

Currently, the pipeline takeaway capacity for ethane out of the Northeast is limited to the Appalachia to Texas pipeline (ATEX). The 125,000 b/d ATEX pipeline carries ethane to the Gulf Coast, and is expandable to 265,000 b/d. Additionally, the 70,000 b/d Mariner East 1 pipeline is capable of transporting ethane and propane to the Marcus Hook facility in Pennsylvania to service export demand. The first cargo of US ethane is expected to leave Marcus Hook in March and Bentek estimates exports are expected to ramp up to 60,000 b/d in 2017. Blog post continues below...

|

|

|||

| Platts Global Polyolefins Outlook |  |

||

|

Platts Global Polyolefins Outlook report and accompanying dataset helps you to understand how today's wide cracking margins are incentivizing a rush for new capacity and how this might erode the US feedstock advantage after 2017.

|

||

|

|

|||

Due to limited transportation infrastructure and unfavorable economics, a large volume of ethane is rejected in the natural gas stream. Ethane rejection averaged about 176,000 b/d in 2015 in the Marcellus/Utica. However, Platts Bentek estimates ethane rejection to decrease to 120,000 b/d in 2017 and to about 75,000 b/d in 2018, due to increased demand from exports and new ethane-only crackers coming online on the US Gulf Coast.

With the declines in rejection and increase in production, ethane recovery in the Northeast will reach 443,000 b/d in 2018, up from 276,000 b/d in 2015. Subsequently, increased ethane volumes will need to flow on ATEX to the Gulf Coast, utilizing near full capacity on an expanded ATEX by 2018. Additional takeaway capacity and demand will be required to balance the oversupplied Northeast ethane market.

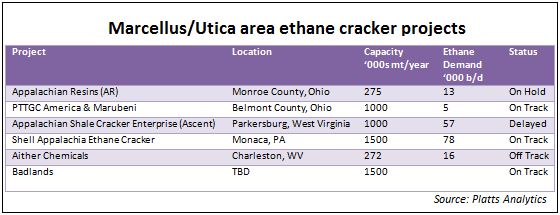

In the US there have been a total of 17 announced greenfield projects. During the next five years, we will see several of these crackers start up, mostly along the US Gulf Coast. In the Marcellus and Utica shale formations, there are four crackers that can possibly be built within the next five years. These include the 275,000 mt/year cracker in Monroe County, Ohio; the 1 million mt/year PTTGC America in Belmont County, Ohio; the 1 million mt/year Ascent cracker in Parkersburg, West Virginia; and the 1.5 million mt/year Shell Appalachia cracker in Monaca, Pennsylvania. Will these projects come to fruition by 2021?

Of all the projects outside the US Gulf Coast, the Shell cracker is the most likely to be built. Though the world-scale cracker has yet to be given the green light, Shell can afford to build considering certain risks, unlike proposed projects run by startups.

The Appalachian Resins cracker has been put on hold due to the difficulties in finding engineering services and workers in the area at the same time when the world scale PTTGC cracker in Belmont County is being constructed. In late October 2015, Technip signed an agreement to provide its ethylene technology and process design package to PTTGC. Many people in the industry have wondered how the Appalachian Resins cracker, with its relatively small capacity, was viable.

According to AR CEO James Cutler during the NGL Feedstocks and Derivatives conference in Houston last week, it is viable if the plant is integrated with a gas plant and polymer plant where the gas plant will send just enough feedstock to the cracker, and the cracker will send just enough feedstock to the polymer plant.

However, since oil prices have fallen significantly, and pulled down most prices of products in the supply chain, the project is no longer feasible, but has been put on hold as opposed to being shelved.

During the first half of 2015, Braskem and Obedrecht announced that the companies were reconsidering and reevaluating the Ascent project in Parkersburg, West Virginia. There were no announcements indicating that this project was cancelled, and there have been some reports that this project may still move forward. Regarding the Aither Chemical small cracker proposed in West Virginia, there haven’t been any announcements indicating that this has been delayed or shelved. However, with its relatively small capacity, it would be difficult to achieve economies of scale. Therefore, we believe that financing this project would be very difficult.

Of all the announced projects, the most aggressive plan has been the proposed Badlands cracker project in North Dakota. According to Badlands CEO William Gilliam during the NGL Feedstocks and Derivatives conference, “Badlands has been working since 2012 to build a plant close to the wellhead.”

Initially, plans were to build a large-scale ethane cracker in North Dakota and a polyethylene plant, with the idea that it is much easier to transport plastic resin than ethane gas or ethylene. Therefore, building a cracker in the Bakken where a lot of ethane is rejected would make sense. Right?

But North Dakota lacks the infrastructure to transport ethane to the East Coast or the Gulf Coast, and may be extremely difficult to accommodate a world-scale cracker and integrated polymer plant. At the conference, Gilliam announced that Badlands is planning two world-scale crackers, the first to be built “on the water” (location was not disclosed), and the second to be built in North Dakota afterwards.

Gilliam also points out that producers in the region are selling condensate at a premium to WTI. Therefore, producers aren’t that concerned with NGLs since they are getting paid well for condensate. Additionally, Badlands is in serious talks with an ethane supplier in Canada, according to Gilliam. As a result, the company will have easy access to ethane.