05 Apr 2016 | 15:47 UTC — Insight Blog

European steel producers on the offensive, but will price increases stick?

Mounting losses, depressed demand and capacity closures have all been causes of misery for European steel producers, reflected in perennially low finished prices. But recently, surging flat-rolled steel prices hint at a bright spot in an otherwise bleak industrial picture.

So what is exactly causing this upward momentum in spot prices when markets are supposedly at their nadir?

After heavy falls in steel prices in the second half of 2015, European producers started this year determined to avoid a repeat situation. Several mills announced €30/tonne increases to their coil prices in Q1. Despite this, the spot market remained lacklustre and the increases barely registered.

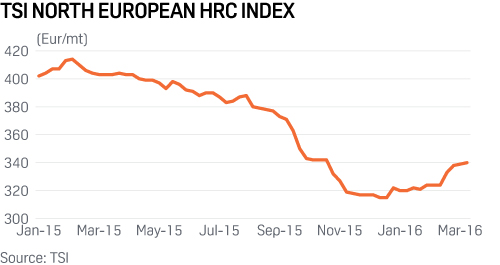

TSI’s North European hot rolled coil (HRC) index averaged €321/t over January-February, marginally lower than its Q4 2015 average, a period which saw two steelmaking behemoths - ArcelorMittal and Tata Steel - record losses of €465 million and €89 million for their European operations respectively.

Luckily for mills strengthening prices in international markets helped European producers push through the increases they deemed necessary.

The rally in iron ore and Chinese domestic steel prices triggered a domino effect around the world as producers raised export offers. Turkish mills quickly increased their coil prices by a whopping US$100/t, which in turn encouraged CIS producers to hike their export offers.

Iranian mills, large exporters into Southern Europe, temporarily withdrew from the market, restricting supply. A recent anti-dumping investigation by the European Commission into Chinese HRC exports created further uncertainty for importers, making them wary of possible retroactive duties.

European mills were also well aware of low inventory levels in the supply chain. According to the German Association of Steel Distribution (BDS), at the end of last year flat steel inventories dropped to the lowest level since December 2003. The latest data showed some improvement, but with flat steel stocks at 1.4 million tonnes in February, they remained 7% lower year-on-year.

With imports priced out, buyers had few options other than booking material from domestic suppliers. With both raw material and steel prices rising globally, sentiment in Europe also turned bullish – TSI’s market survey showed that by the end of February close to 70% of European market participants expected prices to increase over the next three months.

And that upward spiral effect has very much kicked into gear, with European steelmakers once again raising list prices for flat-rolled products in early March. However, the pace of this uptrend stalled and failed to replicate the scale of increases seen, for example, in Asia. Despite the tighter supply, growth in European end-user demand has been less than spectacular.

European steel service centers started to voice concerns that they would not be able to pass mills’ increases to their customers. The European Steel Association (Eurofer) estimated that activity in steel using sectors is going to rise this year by a modest 2% y-o-y.

Markit, publisher of Purchasing Managers’ Indices (PMI), noted in one of its latest releases ‘a slight slowing in the pace of economic growth’ in the Eurozone, and commented that ‘stronger growth in coming months is by no means assured’.

Persistent overcapacity in the European distribution sector, according to some estimates at around 30%, is also dampening steel producers’ expectations. Steel service centres and stockholders competing for business in a fractured market have been known to partially absorb mills’ hikes.

As international steel prices continue to boom, the pendulum has swung in favor of European sellers. For how long this remains the case is anybody’s guess. If Asian steel markets get jittery, the dampening effects on Europe as a steelmaking region could be significant.

After a punishing 2015 and with the outlook uncertain, both European HRC sellers and buyers may see value in re-evaluating sales programs to introduce more flexibility, using indexing as some traders have done, derivatives as the iron ore market has done, or perhaps a combination of the two.