27 Jan 2017 | 10:31 UTC — Insight Blog

Permian returns are producing all of the oil drilling drama

Featuring Matt Andre

In the last year, commodity prices have improved considerably. While oil prices were sub-$40/b in early 2016, producers were cutting back on new drilling and focusing on efficiencies — by cutting costs and concentrating drilling in the highest initial production (IP) rate counties — to get the most bang for their buck.

So when prices finally rallied in the second half of the year (bouncing off $50/b), producers were able to ramp up new drilling activity rather quickly. New drilling grew 71% across the US to 774 rigs in early January 2017 from an average of 452 rigs in June 2016.

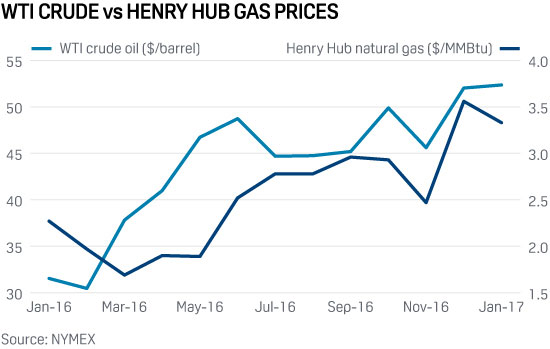

To give more color on the price rally, WTI cash prices have risen 68% to $53/b in January this year from an average of $32/b in January 2016. Over the same time frame, Henry Hub cash prices rose 52% to $3.45/MMBtu from $2.27/MMBtu.

Meanwhile, average returns for a typical new well drilled in the US increased about 14 percentage points over the year according to Platts Analytics’ Well Economics Analyzer (WEA). In West Texas, the oil-rich Permian basin has benefited from a combination of the price rally and drilling efficiencies causing internal rates of return (IRRs) to grow an impressive 30 percentage points to almost 40% in January 2017, up from 10% in January 2016.

Oil prices flirted with $50/b midway through the year, but only in the past two months have they shown that they can sustain above that threshold, causing average returns in the top five oil-rich basins to soar above 30%. For January 2017, the average 12-month forward curve for WTI is up to $56/b, incentivizing new drilling, and producers have responded adding another 55 rigs in the past month. The basin with the largest month-over-month rig increase is the Permian, which is up 29 rigs from the month prior, bringing the total for the basin to 278 rigs.

The Eagle Ford is up 11 rigs from last month with January returns (for a typical well) in the basin averaging 26%, marking a high that hasn’t been achieved since August 2015 when the IRR reached 27%. Rigs in the Eagle Ford have been on the rise since early October, increasing by 24 rigs from early-October’s 35 rigs to early-January’s 59 rigs.

On the gas side, the average 12-month forward curve for Henry Hub fell to $3.30/MMBtu, a decrease of $0.18/MMBtu from the prior month. As a result, returns in the gas-rich plays across North America are down close to three percentage points on average.

Returns in the Marcellus Dry decreased six percentage points, dropping the IRR for a typical well to 15.7%. The decrease is a combination of the Henry Hub price slipping along with Dominion South basis widening, causing the total price to drop to $2.20/MMBtu for January, down about $0.25/MMBtu from $2.45/MMBtu. Even with the minor setback to Northeast gas prices, we still saw an increase in new drilling as the region climbed back to 60 active rigs — levels that haven’t been observed since November 2015. As a point of reference, back in October 2010 drilling activity within the Northeast region reached an all-time high with 184 rigs. During that time, Northeast Pennsylvania was operating 71 rigs, a stark contrast compared to the 10 rigs currently being operated.

Over the past two years producers have struggled with debt concerns and suppressed prices. Our thought is, if oil prices can remain above the $50/b threshold, it will provide some relief and allow rig counts to continue increasing across the US in 2017. One of the risks involved is that as prices rise we anticipate service costs (drilling and completing labor costs) to rise as well, which could put downward pressure on returns for plays across the US.