04 Dec 2018 | 16:13 UTC — Insight Blog

Insight: Extreme volatility returns to NYMEX natural gas futures

By Jason Lord

With volatility making a return to the previously calm US natural gas futures market, it’s important to remember that price swings happen in both directions, as individual fundamentals wax and wane in terms of their influence.

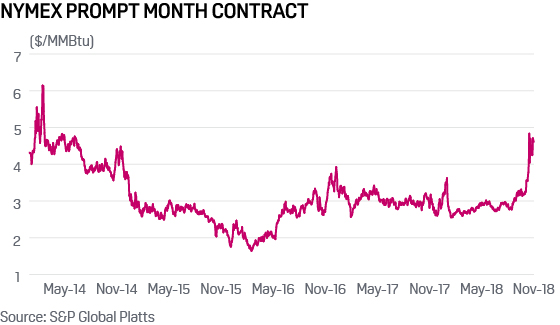

November saw notable price volatility in the December Henry Hub prompt-month contract. The December contract settled and expired at $4.715/MMBtu, up $1.53/MMBtu from the November NYMEX settle.

The onset of a cold November with the looming potential for a cold winter, combined with natural gas storage concerns, created a volatile whipsaw of price movements and resulted in the highest settlement for the NYMEX prompt-month contract since 2014.

November’s bullish market developed in spite of rising domestic production, with the Energy Information Agency estimating dry gas output will average 83.2 Bcf/d in 2018, up 8.5 Bcf/d from the previous year. It is precisely this abundance of supply that appears to have encouraged gas utilities to rely more heavily on volumes sourced directly from pipelines, rather than injecting into and then later pulling from gas storage.

US temperatures in November were the coldest for the month going back to 2014, averaging 46.2 degrees Fahrenheit. This in itself was enough to spook gas markets.

Additionally, the US went into winter with gas stocks around 17% lower year on year. Storage concerns raised during the summer injection season continued as the EIA announced the first withdrawal of the season. This amounted to a whopping 134 Bcf drop in the weekly change of US inventories – the largest initial withdrawal in the past eight years and more than double the previous record pull of 53 Bcf in November 2015.

For prompt-month NYMEX, the November 14 settlement at $4.837/MMBtu was the highest price since February 26, 2014.

The arrival of volatility and higher prices now means the market is looking towards new developing fundamentals and weather trends. As the December prompt month rolls off into January, the market will test higher resistance and lower support levels at these $5/MMBtu and $4/MMBtu thresholds.

With recent price gains in November as large as 73.6 cents in a single day, or single-day losses as big as 79.9 cents, participants must not forget how fast the prompt-month contract blew through the $4/MMBtu threshold on the way up. Prices can fall just as quickly.

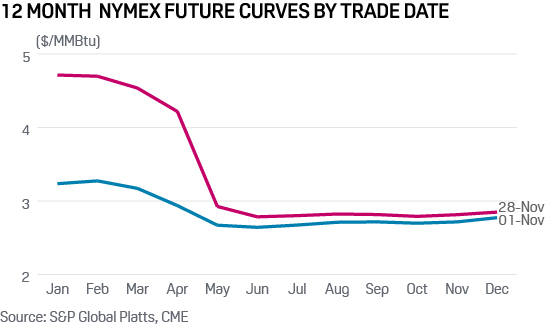

The 12-month strip shows how much changed from the start of November. Despite the dramatic price increase in winter contracts, further down the curve, as markets enter summer injection season, the balance of the 12-month strip did not change much with all April – October contracts settling in a range of $2.746/MMBtu to $2.894/MMBtu, at the November 29 close.

It is during this summer period that production will dominate from a fundamentals perspective as the burgeoning supply looks for new outlets of demand, such as power burn and exports.

Ultimately, winter weather will drive it from here. A mild winter will test the $4/MMBtu support level, and cold weather could push it above $5/MMBtu.

With gas production records expected to continue, weekly reports of natural gas storage levels will have less influence in the market. Other fundamentals – such as weather, pipeline and LNG exports, and power generation demand – will be more in play.