14 Sep 2017 | 08:34 UTC — Insight Blog

To deal with global supply glut, US LNG export developers thinking outside the box

A global market overflowing with LNG supplies is squeezing US developers vying for customers and financing in 2017. But that has not deterred a slew of ventures from seeking to move ahead and sway long-term buyers to their view that the market will shift in the first part of the next decade.

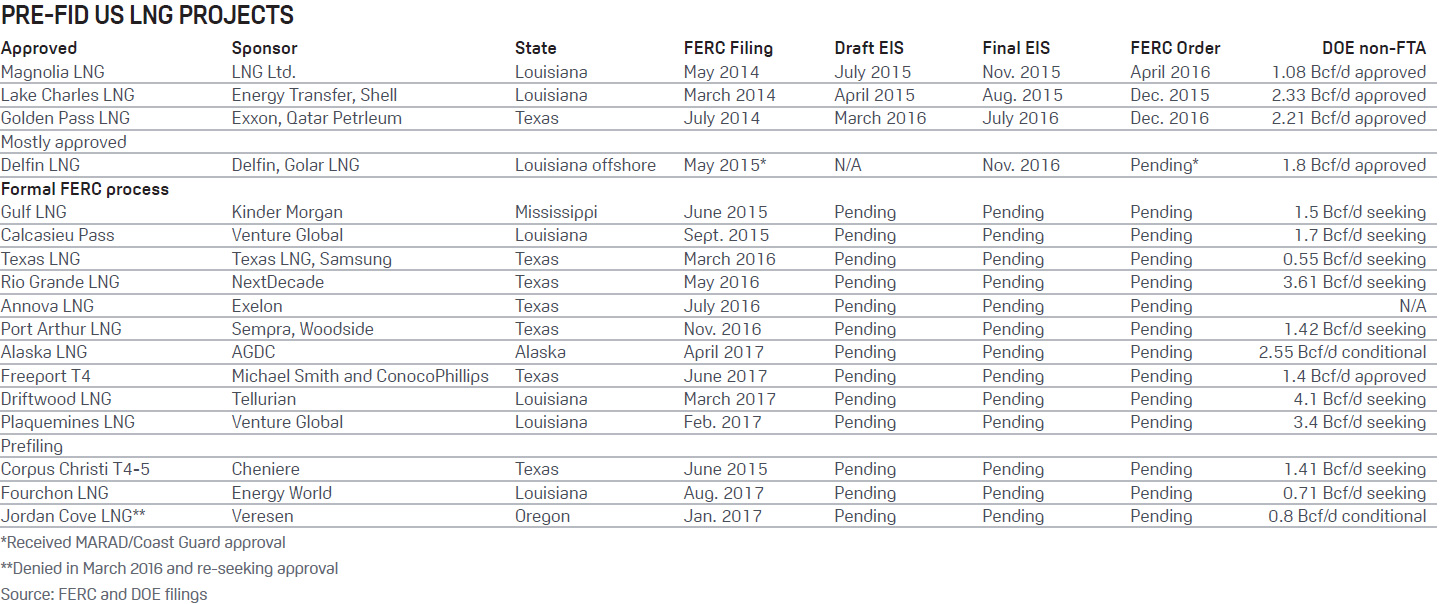

The competition is fierce among pending projects seeking to outlast the current glut, with six projects under construction in the US, another three fully permitted but lacking a final investment decision, and more than a dozen representing 25 Bcf/d of capacity in the queue at the US Federal Energy Regulatory Commission.

For the time being, it's a tough market for LNG export hopefuls who need long-term contracts to sanction their projects.

"The fundamental issue for US LNG is, do the economics still make sense," said Edward Chow, senior fellow for the Center for Strategic and International Studies. US LNG made a lot of sense when international LNG prices were above $8 MMBtu and domestic gas was at $3 MMBtu or less. "At global spot LNG prices of $5 or even below, I don't see how US LNG is in the money," he said.

For some new project developers, it still makes sense because by 2022 there will be sufficient demand and the spot LNG prices won't stay at the relatively low level they are at today, he continued.

"But that's a bet, and the question is can you line up enough creditworthy buyers to commit to buying and paying the tolling charges and the capacity reservation charges in order for your project to be financeable," Chow observed.

The global LNG markets have swung over the last five years from a supply-constrained environment, which drove spot LNG prices to near $20/MMBtu, to the well-supplied environment today, with the Japan Korea Marker (JKM) now trending down to levels equal to European gas prices plus transportation costs.

Analysts are not in agreement on when the market may rebalance, and LNG export hopefuls are taking a similar message of urgency to buyers overseas: If a shortage materializes in 2023, where will you get your supply without any new export projects?

Platts Analytics' Bentek Energy expects the global LNG markets to be moving back toward equilibrium by 2024 and possibly flip short if no incremental capacity is added beyond 2025 or global demand grows faster than expected. As such, the timing of that transition is based heavily on Asian demand growth assumptions, which could prove conservative amid policy shifts favoring LNG for electricity generation.

With global LNG prices now trading at levels that just barely cover variable LNG costs from the US, many of the non-utility buyers have left the market. Much, if not all, of the profit margin in the US spot LNG trade has disappeared.

Many early buyers of US LNG export projects are having buyer’s remorse. In January, Toshiba was reportedly seeking buyers for its roughly 0.3 Bcf/d of capacity at Freeport, rather than face the possible spot market losses.

In July, India’s Gail, which owns 0.85 Bcf/d of capacity spread across Sabine Pass and Cove Point, was seeking to renegotiate pricing with Cheniere Energy.

"It's a very, very tough market," said Ernie Megginson, a consultant with Megginson & Associates.

As some offtakers seek to resell commitments related to brownfield projects already under construction, for instance offering shorter-term contracts, that competes with the projects that haven't reached FID and still must secure long-term contracts, he said.

Magnolia LNG, which has a contract model much like Cheniere's, has had regulatory clearance since April 2016 but is still trying to line up financing and long term contracts.

But demand estimates are feeding the optimists.

LNG demand rose to 37.7 Bcf/d in the first half of 2017, a 4.1 Bcf/d (12%) increase over last year, buoyed by a rapid buildout of liquefaction capacity and led by growth in Asia.

Demand growth is expected to remain robust for the foreseeable future, rising another 17.7 Bcf/d by 2025, according to Platts Analytics, but for now it remains unclear how much more liquefaction can be added before global markets become over-supplied and producers are forced to economically shut in capacity.

Platts Analytics expects that the six LNG export terminals under construction will be completed over the next five years, raising total US LNG export capacity to 9.9 Bcf/d, and that US LNG export terminals will reach full utilization by 2024.

That could make the US the third-largest LNG exporter by 2019, with total exports potentially nearing that of rival Australia by the mid-2020’s.

Click to view image in full size

"I tend toward an optimistic view that delays in new financial investment decisions combined with steady demand growth for natural gas are going to work toward a stronger market and one that remains fairly stable," said Bud Coote, senior fellow of the Global Energy Center at the Atlantic Council.

The current reality is that US sellers have to sell LNG at below their full cycle of costs. "How long they can do it is an open question," he said. By 2020, those sellers will be close to covering their costs, even as those ventures that have not gone forward may be discouraged, he added.

Some key developers of new projects are bullish nonetheless.

Tellurian CEO Meg Gentle earlier this summer cited estimates that by 2025 there will be demand for another 100 million t/year of LNG around the world, and the call on added capacity from the US will be roughly 70% of that.

"I think there is a consensus that more LNG is needed by 2022," she told an Atlantic Council forum. "The big question mark is, will that happen earlier... My prediction is that demand will grow faster than we're expecting."

The winners, she said, are those that can meet the new demand at the lowest cost. The US can be one of the lowest cost sources, she said, describing ways that Tellurian is driving toward lowering costs all along the gas value chain, including owning production. The company announced September 6 that it had entered into an agreement to buy acreage in Louisiana's Haynesville Shale for $85.1 million.

Gentle said that price increases last winter for buyers in Asia and Southern Europe started to change the discussion.

Some buyers realized they may not have the luxury to sit in the spot market, she said. Other market observers have also suggested a recent uptick in interest from buyers.

Cheniere CEO Anatol Feygin said in November 2016 that a drop in the number of FIDs over the past few years indicates that the LNG market will "tighten dramatically by the end of the decade."

As they compete in a market now awash in LNG, US players are trying to be creative in their offerings, for instance by trying to uncover cheaper business models and new types of contracts.

Tellurian is offering Japanese buyers five-year deals through the proposed Driftwood LNG export facility at a fixed $8/MMBtu, a split from traditional 20-year contracts with Henry Hub-linked pricing, as off-takers push for shorter agreements.

Megginson said some yet-unannounced projects are working to offer prices tied to an offtaker's preferred index or a blend of indexes, potentially including TTF in Continental Europe, NBP in the UK, and Brent.

Buyers such as state utilities are keen to link to an index acceptable to regulators, or to mitigate the potential for price swings of a single index. The capability to provide non-Henry Hub pricing is attractive to European buyers, he said.

Other projects are going modular, employing much smaller liquefaction trains that can be pre-fabricated off-site to cut down on costs and increase flexibility.

Magnolia LNG is offering its own liquefaction technology, which the Australian developer hopes to then sell to other LNG export projects.

G2 LNG project, which was recently removed from FERC's prefiling process but said it will re-apply, plans for an expansion that would allow for the export of petrochemicals in addition to LNG.

Cheniere has repeatedly said a third train at its Corpus Christi terminal under construction in Texas would be the cheapest liquefaction train to sanction in the US.

Others have looked to Golden Pass, a fully permitted export project backed by Qatar Petroleum and Exxon Mobil. The Lake Charles LNG project also has the help of a major, though Shell has delayed a final investment decision even while project sponsor Energy Transfer has said it is ready to move forward.

Height Securities analyst Katie Bays says she sees Cheniere being the next developer to see a project advance.

"They’ve said that they have the ability to offer a more flexible contract structure, since they’re less dependent upon the capital markets to finance Corpus Train 3," she said. Cheniere has also signed contracts with EDP Energias de Portugal and Électricité de France for volumes from the third train, leaving as little as 1 million t/year before the unit could be viable for a final investment decision, she said.

Estimates for demand growth after 2020, and the pull on US LNG, are at the mercy of a variety major swing factors that could dramatically alter the picture.

Among those are policies that could influence the turn toward natural gas consumption in key growth areas of China, India and Southeast Asia, the degree to which Russia will protect market share for pipeline gas in Europe, and whether European buyers decide to take the plunge toward long-term contracts to ensure supply diversity.

Other key factors to watch include a possible moratorium on exports from Australia driven by domestic price concerns, and whether Qatar, a key competitor to the US in Asia, follows through on recent promises to increase LNG output by 30% after 2020. Global oil and coal prices also play a critical role.

And Shell has argued that floating storage and regasification units, as well as new demand sources, made predicting demand more difficult than predicting supply.

Gautam Sudhakar, director of IHS Markit's LNG research practice, said his company's base case outlook anticipates the global LNG market will balance around 2023, when a price response is likely.

"But we acknowledge there are numerous sensitivities to demand in many major markets," including new markets and established markets with a large volumetric potential such as China and India.

In South Korea, the newly elected President Moon Jae-in has instituted a policy that backs renewables and LNG for power generation amid air quality concerns about coal and public worries over nuclear safety. Coal is currently the largest power supplier in the country, which Yale University ranked 166 out of 178 nations for air quality.

Sudhakar cautioned that the new policies in South Korea could also swing back. "In just a couple of years you've seen the growth trajectories of the fuels change dramatically," he said. "What's to say that's not going to change again with the next flip-over of administrations in South Korea," he said. China's strong LNG demand growth potential, hinges in part on the drive to improve air quality in big coastal economic centers.

In December 2016, Chinese LNG imports soared to 6.1 Bcf/d, 1.6 Bcf/d (35%) stronger than any previous month on record, due to a combination of a cold winter and heavy pollution emanating from the country's coal fleet. By 2019, China will have increased its LNG import capacity to nearly 9.4 Bcf/d, giving it the potential to eat into large portions of the global balance, according to Platts Analytics.

There’s a chance for that growth to be offset if China seeks to outsource power generation to the coal-rich Western side of the country and wire it to the east, according to Sudhakar.

In India, where the government is pushing to increase gas use, even a small percentage of growth could translate into large volumetric supplies, he said.

For now, US market observers see securing financing — rather than regulatory delays — as the key holdup for US projects.

Nonetheless, industry advocates have welcomed the Trump administration's high-level cheerleading for LNG exports. In meetings with foreign leaders from Asia and Eastern Europe, Trump has touted LNG exports as a way to lower the US trade deficit while bolstering energy security abroad.

US Energy Secretary Rick Perry has signaled that he would move quickly to sign export orders.

"Here are the rules — if you meet the rules, here's your permit," Perry said, summing up the current approach, at a July press conference. Any perceived foot-dragging is a thing of the past, he said.

Among industry backers in Washington, that boost is fueling optimism, despite the erratic messaging that has at times beset Trump's trade policy.

There is still pressure to further grease the skids for LNG exports. For instance, a bill introduced by Senator Bill Cassidy, Republican-Louisiana, and Representative Clay Higgins, Republican-Louisiana, would lift the requirement that DOE make a public interest determination for exports to countries without free trade agreements.

But it's unclear for now how much attention revamping LNG export reviews will get in the crowded political arena in Washington, as larger battles loom over taxes, health care and the budget. In lieu of actual reform, LNG has gained increased visibility from the White House, DOE, the departments of State and Commerce, as well as the US Trade Representative, said Charles Riedl, executive director of the Center for Liquefied Natural Gas.

"It is more optics at this point, but it is a noticeable effort and the value isn't lost upon the industry," he observed.

That signals that LNG exports are aligned with a broader energy policy friendly to added production, and may show buyers that US LNG is a reliable bet, he and other industry advocates suggest.