26 Aug 2019 | 12:05 UTC — Insight Blog

Commodity Tracker: 4 charts to watch this week

An upcoming decision on Dutch gas output will be significant for European wholesale markets, while in bunker markets the impact of IMO 2020 is being felt in differentials between high and low sulfur marine fuels. S&P Global Platts editors delve into key energy trends for the week ahead.

1. EU gas markets await decision on Groningen production quota

What's happening? The Dutch economy ministry is expected to shed light on future production limits on the giant Groningen gas field onshore the Netherlands. In the coming weeks, the ministry should publish the results of work by Dutch gas grid operator Gasunie into the feasibility of lowering the production quota from the field for the next gas year. The quota was provisionally set at 15.9 Bcm, but is expected to be lowered to 12.8 Bcm, or even 12 Bcm.

What’s next? A much lower quota for Groningen will make the Netherlands and other parts of northwest Europe more dependent on gas imports as soon as October this year. The quota for the current gas year is 19.4 Bcm, so a drop to 12 Bcm would leave a big hole in the region’s gas supply. But the economy ministry does not just have to take into account the feasibility of a lower Groningen quota – it also has to weigh the economic and social impact of less domestically produced gas against the risk of earthquakes caused by drilling at the field.

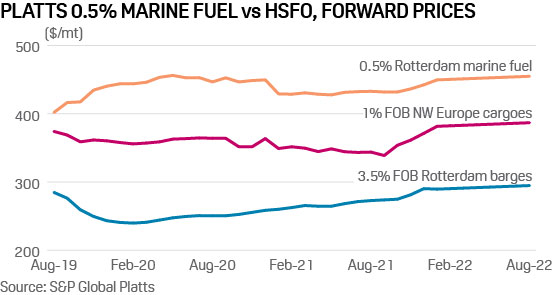

2. High and low sulfur marine fuel spread wide ahead of IMO 2020

What’s happening: In recent weeks the front-month fuel oil crack – the discount to Brent for 3.5% sulfur FOB Rotterdam barges– has reached the widest level in over five years with just months until the International Maritime Organization's lower sulfur cap on marine fuel comes into effect. The forward curve now shows barge prices dropping below $250/mt going into 2020 – a level not seen since late 2016. Running down inventories of high sulfur material in Singapore has been the primary focus of the Asian bunker hub ahead of IMO 2020, while European markets are also purposely running down stocks. The Northwest European fuel oil market has tightened this year, reflected in the highly backwardated 3.5% FOB Rotterdam barge structure. Market players have been preparing for the lower sulfur cap by undergoing refinery upgrades which removed RMG high sulfur bunker fuel from the European market, acquiring storage tanks for blending purposes to produce 0.5% compliant marine fuel, and by taking on scrubbers.

What’s next: With shipowners planning to switch to compliant bunker fuels in the coming months and with a voyage from Europe to Singapore taking 40 days, it will only get more challenging selling high sulfur fuel oil.

3. Power demand boost to US gas prices could be short lived

What’s happening? Record power demand this month is helping to lift US gas prices out of the doldrums, but cooler autumn temperatures ahead could see prices soon revisiting multiyear lows. In August, gas demand for electric generation has averaged 41.5 Bcf/d, or its highest monthly average on record by a margin of 1 Bcf/d, data compiled by S&P Global Platts Analytics shows. On August 21, cash prices at the Henry Hub settled at $2.245/MMBtu and last week climbed to their highest level since late July, S&P Global Platts data shows.

What’s next? Moving into September, the seasonal shift should see power burn demand fall sharply. According to Platts Analytics, weather-normal demand in September would average only 33.7 Bcf/d or about 7.7 Bcf/d lower compared to the August-to-date average. Flagging shoulder-season demand next month, though, is likely to meet with continued gains in US gas production, putting additional pressure on prices. On August 19, output climbed to a fresh record high at 91.3 Bcf/d, marking the eighth record high already this month.

4. German gas-fired generation profitability could persist beyond summer

What's happening? Generation spreads indicate German gas-fired power station profitability is stretching deeper into winter, maintaining a summer-long ascendancy over the country’s coal plant fleet. Negative spreads, the preserve of gas plants for so many years, have driven German coal-fired output to record lows in August with little improvement expected this autumn.

What's next? While forward margins for the most efficient coal plant surpass those for gas into Q4 2019 and Q1 2020, gas plant forward margins remain near nine-year highs. With healthy gas stores expected to end-December, and 3 GW of nuclear, coal and lignite closures this winter tightening the market, the prospect for gas spreads remain positive. This is a reversal of last autumn's scenario when a tight gas market pushed gas plant to the bottom of the merit order.

Reporting by Stuart Elliott, Paul Hickin, Jack Jordan, Tamara Sleiman, J Robinson, Andreas Franke, Henry Edwardes-Evans