13 Jun 2018 | 05:31 UTC — Insight Blog

3 key impacts of Trump's gas policies in Asia

By Eric Yep

The geopolitics of gas, and especially LNG, in the Asia Pacific reached a crescendo early this month when US negotiators got Beijing to agree to buy more American LNG in exchange for easing trade tariffs.

The natural gas industry has come a long way since the days of Unocal and Nexen.

When state-run China National Offshore Oil Corp or CNOOC’s $18.5 billion takeover bid for California-based energy company Unocal was shot down in 2005 and its $15.1 billion takeover of Calgary-based Nexen in 2012-13 faced political backlash, Chinese state corporations were left traumatized.

As recently as 2016, American companies were wary of selling stakes in LNG projects to Chinese buyers amid political sensitivities, even though Washington steered clear of making any ban official.

Then in mid-2017, US President Donald Trump signed a 10-point plan to boost trade between US and China, openly inviting Beijing to import US LNG, saying “the United States treats China no less favorably than other non-FTA trade partners with regard to LNG export authorizations.”

With US Commerce Secretary Wilbur Ross’ latest push in Beijing over the weekend, Trump has firmly anchored US LNG in China’s import mix.

Trump’s gas politics have three major consequences for Asian markets:

1. Trump has forced US LNG to become more competitive in Asia

Let’s face it; Asia is not exactly the natural home for US LNG exports.

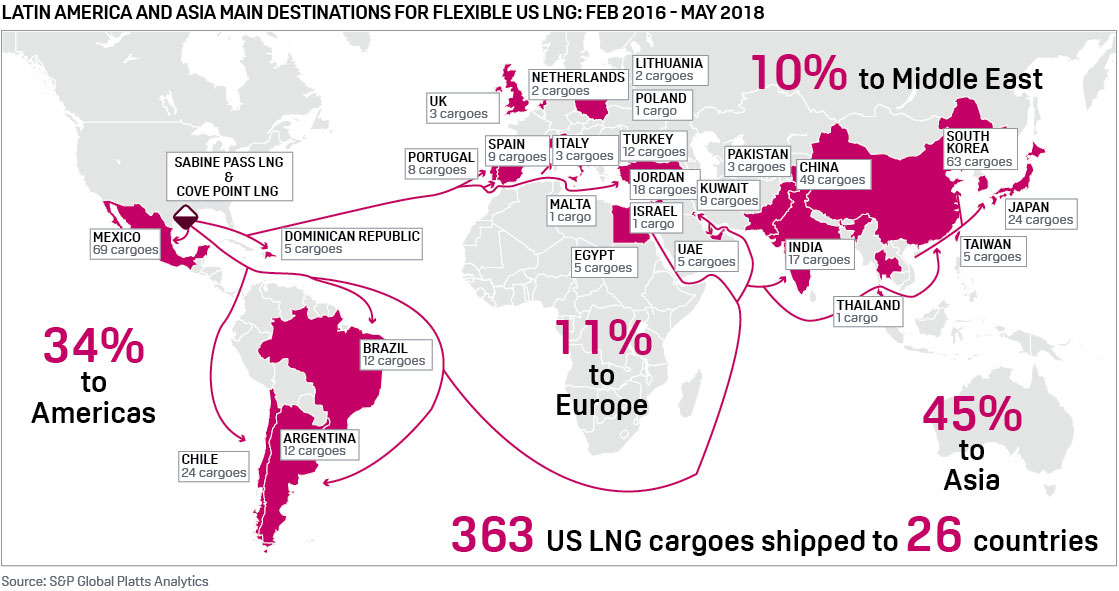

US LNG is inherently freight disadvantaged and takes up more shipping capacity than nearly every other LNG exporter, resulting in higher transportation costs. LNG carriers carrying US cargoes are typically on the water for an average of 125 days, compared with just 50 days for LNG produced in Malaysia and Brunei, according to Platts Analytics.

Moreover, US LNG is largely destination-free and opportunistic.

Around 66% of US LNG is currently contracted to Asian utilities and national oil companies, while 28% is held by portfolio buyers like Shell and 6% is still uncontracted, according to Jeff Moore, Asia manager for LNG at Platts Analytics.

That's nearly a third of US volumes that are floating, not counting the contracted volumes that are being resold by Asian utilities which have easier access to Qatari and Australian volumes.

Most importantly, Trump has helped US LNG break into markets dominated by Qatar and Australia, in a battle for market share.

In the first quarter of 2018, Australia accounted for a whopping 37% of China’s LNG imports, followed by Qatar at 23%.

Queensland state was China’s largest LNG supplier in the first quarter, bigger than Qatar at 2.9 million mt, with nearly 26% of China’s LNG imports supplied by Gladstone projects alone, according to Perth-based consultancy EnergyQuest.

Trump has now helped US LNG dislodge its competitors.

2. US LNG now faces off with Russian gas on a new front - Asia

So far, Chinese demand has been strong enough to soak up LNG from all regions.

But that could change when Russian gas starts flowing. Chinese buyers have been holding out on signing long-term offtake agreements on expectations that Russia’s "Power of Siberia" pipeline will start up by the end of this decade.

Then, it could be a fight for market share again - and Trump has put US LNG in the heart of a market that the Russians have tried to crack for decades using both pipelines and ships.

Power of Siberia will carry 38 Bcm of gas on its eastern route and 30 Bcm on its western route to China at full capacity.

Together with Yamal LNG in the Russian Arctic, Russia's gas exports to Asia could cross 100 Bcm within a few years, nearly half of Russia's record 194 Bcm of gas exports to Europe in 2017.

Trump threatens Moscow’s long-term strategy to diversify energy exports to Asian markets, and cut reliance on Europe where geopolitics has already seen some of its supplies compete with US LNG in some countries.

After Europe, Trump has taken the fight to Russia’s gas markets in Asia, and his Beijing maneuver will be the thin end of the wedge for US LNG to penetrate Asian demand.

3. Iranian gas is forced to stay under the ground

The US trade delegation to Beijing was preceded by Trump’s withdrawal from the Iran nuclear deal.

Iran holds the world’s largest gas reserves, at 18% of total global gas reserves estimated at 6,589 Tcf, followed by Russia at 17.3% and Qatar at around 13%; the US has just 4.7%, according to the BP Statistical Review of World Energy 2017.

“We are all talking about the competition to get in line for projects, and the Iranians were aware of this the first time around [when US sanctions were lifted] - the longer they are under the sanctions, the more years they get back to the end of the line on LNG,” Amy Myers Jaffe, director of the program on Energy Security and Climate Change at the Council on Foreign Relations, said in a recent interview.

She said if Iran loses another two to three years in the LNG supply race, then it will miss the 2025 demand window, and then the next tranche of demand as well.

“And at some point when you start losing each tranche of demand you have to ask yourself, does renewable energy and nuclear in China create so little market opportunity that there never is a market opportunity for Iran?” Jaffe said.

She said after a certain point, Iranian LNG “loses the market forever and they never export, ever.”

Perhaps that’s exactly what Trump wants.