19 Nov 2019 | 13:58 UTC — Insight Blog

Around the tracks: Auto sales, coil prices unlikely to gain traction before 2020

By Paul Bartholomew and Clement Choo

This new monthly feature looks at key auto markets around the globe, including output and sales trends and the impact on relevant steel and metals prices.

The auto sector accounts for around 25% of steel consumption in the US and Germany, 7% in China and 12% in India. The sector will play a growing role in metals demand in emerging nations.

Global manufacturing has undergone a severe downturn this year, due in large part to US-China trade tensions undermining investor confidence. Consumers have not been immune to the negative sentiment and many have deferred decisions to buy cars and other consumer goods.

China’s auto sales and output improved in September but were still down on the year before. Demand in Germany and India slumped in September. Prices of steel coil used in auto manufacturing fell in all major markets in September, while lithium chemical prices show no sign of any recovery.

Forward gear: Auto sales in China, Philippines and Vietnam

Reverse gear: Auto sales in the US, EU and India. Coil prices in most major markets.

Outlook

Views are mixed on prospects for the auto market in Europe with an upturn likely to occur in Q2 next year. Strong seasonal buying may not occur in China in November and December due to bearish consumer sentiment, while over in the US, another interest rate rise may have a negative impact on auto. Coil prices will likely stay weak next month despite efforts from US and EU steelmakers to support prices. Steel export markets will stay extremely competitive with coil flowing into Asian markets and dampening prices.

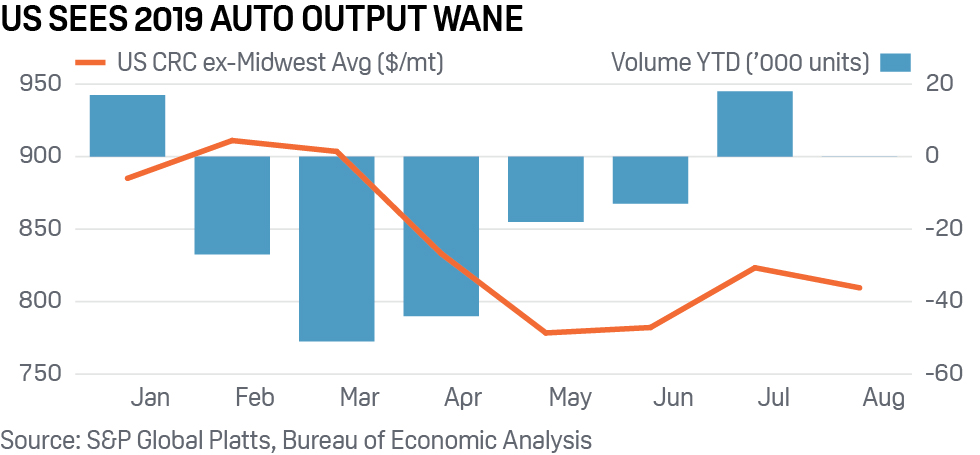

US

In the US, the outlook for the sector is mixed and the industry has been hampered by industrial unrest. US metals company Reliance Steel & Aluminum said it expected stronger demand from the automotive sector in Q4. Nissan has warned that higher interest rates in the US may further dampen consumer sentiment for buying cars.

- New passenger vehicle sales dropped 11% on year to 1,272,726 units in September, government data shows. Toyota’s sales of light vehicles slumped by 16.5% on year in September, while Nissan’s dropped by 17.6%.

- S&P Global Platts data shows that US cold-rolled coil prices averaged $693.4/short ton in October, compared with $734.35/st in September.

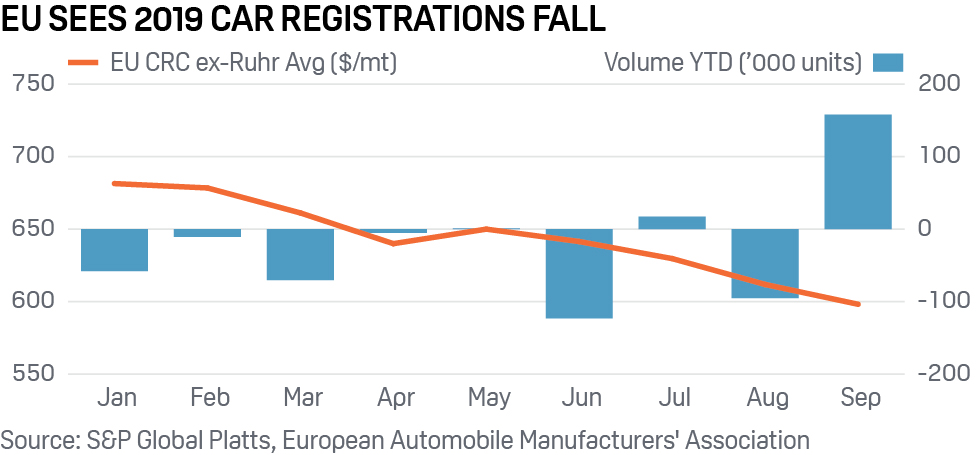

EU

EU manufacturing remains in the doldrums, with Germany, the region’s biggest car producer, now seemingly on the brink of recession. The European steel market has suffered from the downturn in automotive and construction demand, while in the UK uncertainty surrounding Brexit has resulted in a lack of confidence among consumers and investors.

- Car registrations in France dropped by 14% on year in August.

- Delegates at a trade fair in Stuttgart in late October said they expected a recovery in the auto sector by April 2020.

- Northern European cold-rolled coil prices averaged $535/mt in October, down from $555.4/mt in September, Platts data shows.

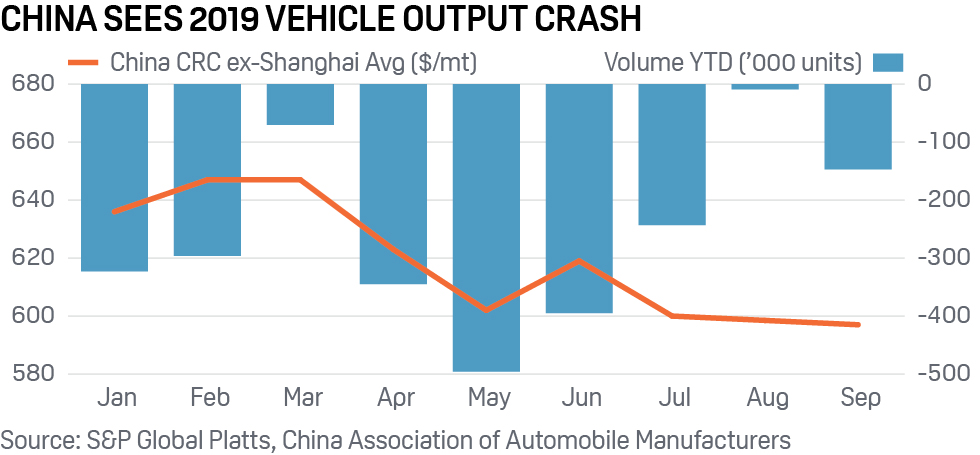

China

China's vehicle output and sales have started to recover – or at least, the decline has slowed. Last year saw the first reversal in car sales and production since the early 1990s. Chinese consumers remain highly leveraged to property and are buying fewer cars. The US-China trade conflict also continues to dampen sentiment and weigh on investment decisions.

- Chinese CRC output increased by just 2.8% on year over January-September to 24.55 million mt, compared with HRC growth of 11%. Domestic CRC prices averaged Yuan 4,242.33/mt in September, down from Yuan 4,259/mt in August.

- China's vehicle output and sales in October reached 2.30 million and 2.28 million units respectively, up 3.9% and 0.6% on the month, and 1.7% and 4% lower than a year earlier, data released by the China Association of Automobile showed.

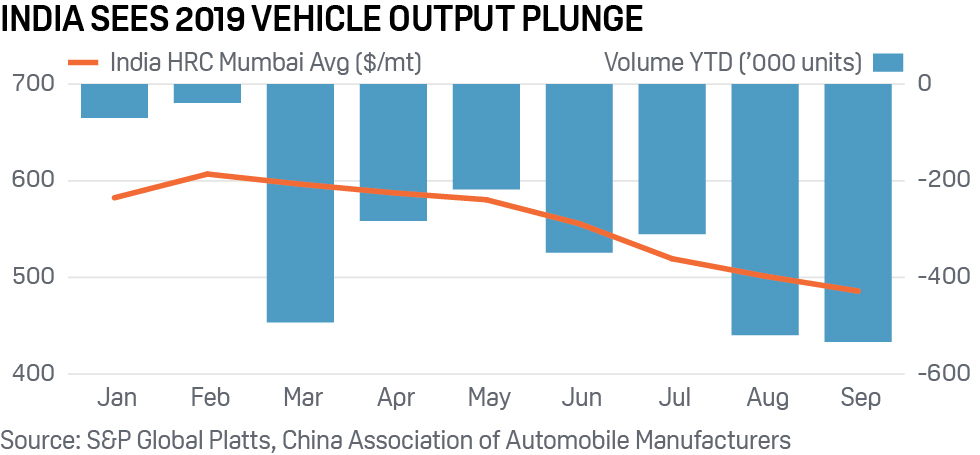

India

Auto demand was expected to be one of the big drivers of Indian steel demand but growth expectations of around 6-7% in the next few years may fall short. Car producers continue to cut production to bring down inventories, which in turn is pulling down steel coil prices. This was due to weak demand and output cuts resulting from the economic slowdown. India’s car ownership on a per capita basis stands at just 22 per 1,000 inhabitants, compared with 173 in China.

- India's vehicle production in October fell for an 11th month running, down 26% on year to 2.16 million units, data from the Society of Indian Automobile Manufacturers showed.

- Indian HRC prices have slumped by 18% this year, forcing Indian steelmakers to look overseas for sales in recent months.

What to look out for

In Europe the market will want more clarity on

ArcelorMittal’s announcementthat it plans to stop operating the Ilva Taranto steelworks in Italy. Less coil supply could support prices but it will probably require an improvement in auto demand. US steel prices will depend on whether the auto sector supports mills’ attempts to hike prices. Car makers in the US normally offer big discounts in December in a bid to meet yearly sales targets, which could see an uplift in sales.