14 May 2019 | 14:54 UTC — Insight Blog

Iron ore markets digest impact of Vale tailings dam disaster

By Jun Kai Heng

Ahead of the S&P Global Platts Global Metals Awards in London, on May 16, The Barrel presents a special series of articles looking at the global metals trade. Here, Jun Kai Heng looks at how iron ore buyers and sellers are adapting to tightened supply of specific products, following the accident at one of Vale’s Brazilian operations in January.

On January 25, a Vale tailings dam in Brumadinho, part of its Southern Systems mining operations, collapsed, resulting in massive loss of life and a significant impact on its iron ore supply chain over the longer term.

The company declared force majeure in the first week of February on a range of iron ore qualities after Minas Gerais state authorities ordered a production halt at Vale’s 30 million metric ton/year Brucutu mine, alleging safety concerns. Vale later noted that maintaining supplies to the domestic market was its priority, and that it was giving preference to contractual commitments over spot market sales.

Initial concern from market participants was related to Vale’s production of its medium grade fines, including the flagship Brazilian Blend fines (BRBF) as well as Standard Sinter Feed Guaiba (SSFG), given their reliance on Southern System fines for blending with high grade fines mined from the Northern Systems.

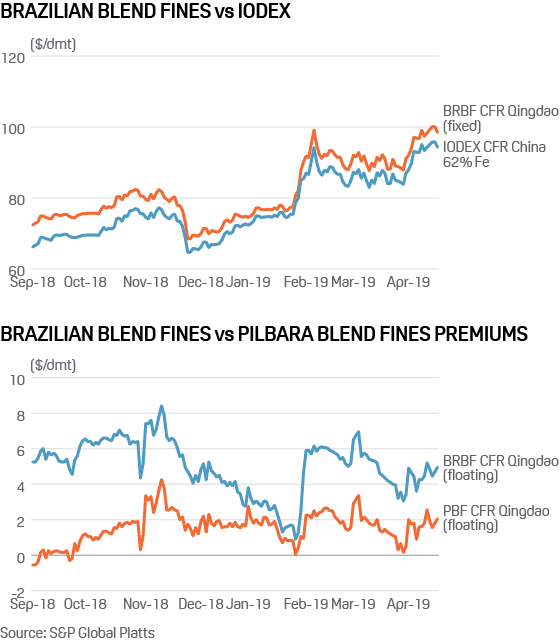

Marketed as a premium medium grade fines product, Vale’s Teluk Rubiah-blended BRBF was traded at high premiums of around $5-6/dry metric ton against the S&P Global Platts 62% Fe IODEX in the third quarter 2018 and tradeable at a premium of over $8/dmt in November 2018. End-users were seeking to capitalize on its low alumina and high Fe content to increase production efficiency, while staying within stringent environmental limits.

However towards the end of the last quarter of 2018, premiums for BRBF had been declining in the face of thin steel margins, sinking to a tradeable low of $1.85/dmt on January 18. Market sources said that a more relaxed approach to environmental pollution had also resulted in steel mills being unwilling to pay higher prices for low-alumina fines.

Vale currently produces several variants of its BRBF, with market sources valuing those blended at Teluk Rubiah in Malaysia with the highest premiums, due to better sintering consistency and blending compared to those blended at the northern Chinese ports for domestic use.

At the northern Chinese ports During the same period, spreads between port-blended BRBF and Pilbara Blend fines (PBF) narrowed to levels around Yuan 5-10 per wet metric ton as compared to levels of around Yuan 5-10/wet metric ton in the previous two quarters.

In the week following the accident, industry participants saw with greater clarity the longer-term impact of the Vale incident with Chinese market participants returning from the Lunar New Year holidays.

Expectations were of a significant reduction in production of Vale's Southern System fines, including those used for the blending of BRBF with Carajas fines. Platts observed increasingly high premiums for BRBF in the spot market, with premiums for BRBF strengthening to over $6/dmt against the front month IODEX on February 8.

Market sources also reported rising demand for other similar Brazilian low-alumina fines, like Sudeste and IOC6 from Trafigura and CSN, with bid levels rising to over $3/dmt from around flat to $1/dmt in the following weeks after the accident.

Sellers of Mauritanian TZFC fines also saw strong buying interest as buyers looked to secure alternative cargoes with low alumina and medium-to-high silica content. The typical specifications for Teluk Rubiah-blended BRBF are 1.5% alumina and 5% silica, with the silica content regarded as ideal for the raw feedstock blend for Chinese blast furnaces.

Amid an increase in market activity for Brazilian low-alumina cargoes, many market participants were adopting a cautious attitude due to existing high surplus volumes, and uncertainty over the operational status of Vale’s other mines. Market sources said that a visible tightening in supply would only be present after March, when end-user demand was expected to pick up.

Export data seen by Platts for the week of February 4 demonstrated a 54% dip on the previous week for volumes exported out of Tubarao, a main export port for Vale’s Southern System products, to just over 940,000 mt. However, sources said that the declaration of port maintenances by Vale over the same period meant that further monitoring was required.

Vale's production and exports

More clarity on Vale's export volumes was only attained in the week of March 11, with export data seen by S&P Global Platts demonstrating that export volumes out of Vale's Guaiba port in the south fell by 60% on the week, to 176,000 mt. Then, from March 18 to the week of April 15, Vale’s export volumes out of Guaiba were at a weekly average of 264,000 mt, in contrast with a weekly average of 809,000 mt for the calendar year of 2018. In the week of March 25, export volumes out of Tubarao decreased by 36% on the week to 786,000 mt, before further declining to 351,000 mt in the week of April 8.

Vale’s CFO Luciano Siani said in a conference callwith analysts late March that the miner’s average iron ore product mix was set to decline in terms of quality following the January 25 dam burst. “With lower levels of wet (ore) processing, production of higher value added products falls and so we need more high-quality Carajas ore for blending to correct the quality of some products,” Siani said. “We are committed to maintaining stable our offer of Brazilian blend fines (BRBF), our principal product.” However, the offer of Carajas and niche products would decline, he said.

"Although it is unclear how long low loading volumes will continue, end-users are definitely looking to reduce their reliance on Brazilian low-alumina fines and alter their feedstock blends," a northern Chinese mill source said.

Alternative products

Several market sources said that, while higher premiums for alternative Brazilian fines were reflective of the current situation for iron ore supply, large-scale end-users were unlikely to use these options as a full direct replacement for impacted volumes of BRBF supply.

“A mill’s main priority when it comes to iron ore procurement is stability, especially for those with massive blast furnaces where a significant alteration of the raw feedstock blend will have a detrimental impact on performance, as the accompanying coke blend cannot be adjusted so easily. There are not too many products in the market which have the same supply volumes and spot availability as mainstream Australian fines and BRBF,” an end-user procurement source said.

"The supply of these alternative low alumina fines is definitely not sufficient to replace the estimated loss in BRBF supply and this is not taking into account many other technical differences like sizing, which require other changes in the blast furnace operations,” the source added. “The use of these alternative options as an immediate direct replacement is more suited for smaller mills with high levels of flexibility for their feedstock options. For large-scale mills, a longer-term and gradual shift in feedstock to stable alternatives is needed.”

Although the authorization of the resumption of operations at Vale’s Brucutu mine by a Brazilian court on April 16 was expected to add 30 million mt of iron ore supply back into Vale’s production volumes, market sources warned against being too optimistic.

“Vale has not changed their volume guidance due to reduced shipments in April from Ponta da Madeira as a result of bad weather. It remains to be seen which products iron ore from Brucutu feeds into, and when this supply becomes available in the spot market,” an Asian trader said. “Vale has stated its priority to be its domestic Brazilian steel end-user demand, so it is unclear how much of a supply boost this announcement will have,” the source added.

Market sources displayed mixed expectations of demand for higher-silica fines, as a replacement for the higher silica content of Vale’s Southern Systems-based products, in the longer run. "There are not too many sustainable high silica alternatives in the market, so this could present an issue to end-users. South African Kumba fines are one of the closest in specifications to BRBF for non-Brazilian options, but the alkali content is a major issue for many blast furnaces," an eastern Chinese mill source said.

"The silica issue is not as serious as a shortage of low alumina, but it will have an impact on the coke rate and other production factors. However, there are some alternatives to work around it without a change in feedstock blends," an Asian mill source said.

Pellet market

Another significant impact of Vale's dam accident is the reduced supply for the pellet and pellet feed market. With Vale's declared priority the domestic market, shipments of around 11 million mt of pellet – a concentrated, direct-feed, high-iron product – are expected to be affected.

Market sources say that the reduced supply will have a smaller impact on Chinese end-users compared to other Asian and European mills, due to the availability of domestic concentrate that can be used for pelletization.

"Indian pellets are likely to see increasingly higher prices into the second half of the year. Although there are Chinese domestic options, they are still dependent on the extent of environmental controls. European mills have been heard inquiring about Indian pellet offers, which is only likely to push spot prices up higher," an international trader said.

The resumption of Anglo American's Minas Rio pellet feed concentrate production has eased some supply concerns, with expected production levels of 16-19 million mt in 2019. Several market sources pointed to new opportunities for Vale due to the creation of spare capacity from Oman.

Vale’s current distribution and pelletizing complex in Oman is targeted at regional Middle Eastern end-users, with its port in Sohar able to receive its Valemax iron ore cargoes from Brazil. "Middle Eastern steel mills had switched over to supply from Vale after the Minas Rio pipeline was shut. With the resumption of production, these mills will be reverting back to prior contracts, leaving a surplus of iron ore from Sohar," an international trader said. "Vale has already begun selling its Carajas fines from the port of Sohar, a clear indicator of spare inventories," the source added.

The spread between high-grade and medium-grade fines saw little impact in the immediate aftermath of the Vale accident, as direct production cuts and halting of mine operations were limited to the Southern Systems, with no visible restrictions on Carajas fines production. In addition, the thin levels of steel margins in the first quarter of 2019 meant that demand for high grade fines remained tepid, and the 65-62% Fe spread narrowed from $14.10/dmt on January 28, to a year low of $11.65/dmt on March 4.

Trade flows shift

Initial market expectations from sources were towards a possible increase in spot supply of Carajas fines, due to lower volumes of Southern System fines being available for blending at Teluk Rubiah and Chinese ports. On April 12, Vale sold a 170,000 mt cargo of Carajas fines from Teluk Rubiah terminal, loading May 10-19 at $110/dmt.

“While Vale’s sale from Teluk Rubiah will ease supply constraints for Carajas fines due to delayed loadings at Ponta da Madeira as a result of poor weather, it is too early to say what Vale’s new strategy will be with regards to its current problems,” another international trader said.

"Loading rates at Ponta da Madeira have been at very low levels, and the impact of delayed shipments is likely to be felt as spring demand for iron ore is picking up," a trader said. "In addition to delayed loading, there is concern over the spot availability of Carajas fines given Vale's public commitment to channel more Carajas volumes into its BRBF blending. Over the long run, this reduction in supply should support a widening of the high and medium grade fines spread," another trader said.

However in late April, several market sources expected a longer-term trend of sales of Carajas fines from Asia rather than from Ponta da Madeira due to the current situation in Brazil.

“Vale does not have sufficient loading volumes from its southern ports to load all its contracted vessels beyond the near term, and is likely to use some of these empty vessels towards Ponta da Madeira to load Carajas fines,” a source said. “Given the current high prices for Carajas fines, shifting volumes to Asian ports to reduce the duration in anticipation of stronger demand would be a very logical choice, especially with so much spare tonnage available,” the source added.

“For May, the ratio of Valemaxes from Ponta da Madeira and Tubarao to Teluk Rubiah suggests that more sales of Carajas fines from Teluk Rubiah is very likely, given the much higher proportion of Carajas fines that is needed for blending BRBF,” an international trader said.

“Supply of Carajas fines has been tight recently due to delayed loadings from bad weather at Ponta da Madeira. There are discussions on future sales of Carajas fines from bonded warehouses in Dalian and Yantai like BRBF into the Northeast Asian market to get around this issue,” another international trader said.

Vale did not respond to inquiries from Platts at the time of publication about possible new marketing strategies from its existing distribution centers, and its subletting of contracted capesize tonnages from Brazil.